Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

After two years of challenges for personal auto insurers, rating agency AM Best delivered a positive assessment: U.S. personal auto insurers are the furthest ahead when it comes to innovation.

Personal auto insurers’ innovative processes include automated claims management and the use of data to automate underwriting, according to a new AM Best report, titled “Highly Innovative Personal Auto Carriers Have Significant Competitive Edge,” in which analysts delve into how AM Best innovation scores line up with growth, profitability and overall rating agency actions.

Personal auto insurers have the highest average innovation scores among property/casualty lines of business, the report says.

AM Best has been scoring and assessing insurers’ innovation efforts since 2020. (Read sidebar articles for more information about the scoring process.)

Learn more about AM Best’s Innovation Assessments in these articles published by Carrier Management in 2020-2022

“Personal auto as a line of business is well suited to innovation,” said Helen Andersen, an AM Best industry research analyst, in a statement about the report. Personal auto carriers “deal with large homogenous risks, allowing initiatives to be scaled and replicated relatively easily,” she said.

But not all the personal lines insurers fare as well as those that AM Best assigned to the “Leader” category—the highest Innovation score assessment—when it comes to growth and market share.

In fact, insurers writing primarily personal auto that hold the “Leader” designation have seen average growth in net written premiums of 13.3 percent, while the growth percentage for the same period of the AM Best’s personal auto insurer’s composite was 5.5 percent.

AM Best translates innovation scores into five innovation capability assessment categories: Leader, Prominent, Significant, Moderate and Minimal.

According to the report, lower innovation scores of Minimal and Moderate “are overrepresented” among 18 personal auto carriers that AM Best downgraded in 2023. No insurers assessed as Leader were downgraded. While just over 35 percent of personal auto insurers have Moderate assessments, two-thirds of those whose ratings were downgraded have an innovation assessment of Moderate.

The report also presents information on relative growth rates and combined ratios by innovation category across the U.S. P/C industry, revealing the growth is significantly higher for innovators, and combined ratios are lower—driven by expense ratio differences. Innovative companies continue to slightly higher loss ratios, a finding that AM Best has published in prior years. (Related article, “Innovating to Control Costs: Carriers Seeking Top-Line Growth Amid Bottom-Line Pressures“)

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

TAMPA, Fla. (AP) — HCI Group Inc. (HCI) on Wednesday reported first-quarter profit of $47.6 million, which follows a $38 million profit for Q4 2023.

The Tampa-based company said it had profit of $3.81 per share. Earnings, adjusted for non-recurring gains, were $3.65 per share.

The results beat Wall Street expectations. The average estimate of three analysts surveyed by Zacks Investment Research was for earnings of $2.74 per share.

The property and casualty insurance holding company posted revenue of $206.6 million in the period, which also topped Street forecasts. Three analysts surveyed by Zacks expected $189.2 million.

Copyright 2024 Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

St. Pete Looking at Downtown Transformation with Housing and New Rays Stadium

ST. PETERSBURG, Fla. (AP) — The future of the Tampa Bay Rays is about to come into clearer focus as local officials begin public discussions over a planned $1.3 billion ballpark that would be the anchor of a much larger project to transform downtown St. Petersburg with affordable housing, a Black history museum, a hotel and office and retail space.

The St. Petersburg City Council will begin a detailed look Thursday at the plans by the Rays and the Hines development company for what the city calls the Historic Gas Plant Project. The name is a nod to the 86-acre (34-hectare) tract’s history as a once-thriving Black community demolished for the Rays’ current domed Tropicana Field and earlier for an interstate highway spur.

Mayor Ken Welch is St. Petersburg’s first Black mayor and his family has roots in the Gas Plant neighborhood when the city was racially segregated. He said it’s important to keep the Rays in the area and to restore promises of economic opportunity never met for minority residents after the businesses and families were forced out decades ago.

“I see it as a real opportunity to uplift the entire city,” Welch, a Democrat, said in an interview at City Hall. “This isn’t just a stadium. This is a stadium surrounded by the largest development in the state of Florida, if not the nation.”

The plan would cap years of uncertainty about the Rays’ future, including possible moves across the bay to Tampa; Nashville, Tennessee; and even an idea to split home games between St. Petersburg and Montreal. The Rays typically draw among the lowest attendance in MLB, even though the team has made the playoffs five years in a row.

The proposed 30,000-seat ballpark, which would open for the 2028 season, is a priority in the first phase of what ultimately is a $6.5 billion project. The City Council meeting Thursday will focus on other aspects of the plan, with a May 23 meeting set on the ballpark itself. Final votes are expected in either June or July; the Pinellas County Commission also must vote on the project.

According to the Rays, the first phase will break ground next spring with the ballpark and initially include 1,500 residential units, 500 hotel rooms, office and medical space, a new Woodson African American Museum of Florida, as well as entertainment, conference, ballroom and meeting spaces. The plan also calls for a tract of open space, particularly around a nearby creek, as well as work on an abandoned Black cemetery near the site.

The plan has drawn strong support from business and charity leaders across Tampa Bay, as well as organizations ranging from the NHL’s Lightning to St. Pete Pride, an LGBTQ+ group. Many local Black leaders also are in favor, according to support letters they have sent to the council.

Gwendolyn Reese, president of the African American Heritage Association, once lived in the Gas Plant neighborhood. She said people like her and descendants of the earlier residents feel “vindicated” by the inclusionary nature of the overall project. The local NAACP branch also endorsed it.

“People gave up their neighborhood for a better way of life, and none of that happened,” Reese said. “That has been like a stone in the hearts of many people in our community. This is a wonderful opportunity for the city to move ahead.”

The Rays’ ballpark is part of a wave of construction or renovation at sports venues across the country, including the Milwaukee Brewers, Buffalo Bills, Tennessee Titans and the Oakland Athletics, who are planning to relocate to Las Vegas. Like the Rays, all of the projects come with millions of dollars in public funding that usually draws opposition.

The Rays’ financing plan calls for the city to spend $417.5 million, including $287.5 million for the ballpark itself and $130 million in infrastructure for the larger redevelopment project that would include such things as sewage, traffic signals and roads. The city envisions no new or increased taxes.

Pinellas County, meanwhile, would spend about $312.5 million for its share of the ballpark costs. Officials say the county money will come from a bed tax largely funded by visitors that can be spent only on tourist-related and economic development expenses.

The Rays and Hines will be responsible for the remaining stadium costs — about $600 million — and any cost overruns during construction. The team would have naming rights to the ballpark, which could top $10 million a year.

Detractors in the Tampa Bay area, including a group called No Home Run, contend the Rays and Hines should pay rent to make up for potentially lost property tax dollars, split revenue with the city and county and be required to buy the prime downtown land at a fairer value.

“The only real goal in this project was for the Rays to get an incredible deal on a new stadium and to keep out all other lead developers so the Rays didn’t give up control,” wrote Alan Delisle, a former St. Petersburg city administrator, in a post on the No Home Run site. “They will always do what is in the best interest of the team and business. The City of St. Pete will always be secondary.”

Mayor Welch, however, said he and the project supporters are determined to see it through and that it has a real chance to transform the city, which has already changed dramatically from a sleepy retirement haven to a beacon for younger residents with a hip downtown not far from Gulf of Mexico beaches. After the ballpark opens, the rest is expected to be completed over about 20 years in several phases.

“I think we’re in a much stronger, competitive position than we have ever been,” Welch said. “There’s a tremendous amount of faith we’ll get it right this time.”

Photo: St. Petersburg Mayor Ken Welch compares an old aerial photo of downtown St. Petersburg with a newer one. The Rays stadium is the linchpin of a much larger project that would transform the downtown with affordable housing, a Black history museum, office and retail space. (AP Photo/Chris O’Meara)

Copyright 2024 Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Property insurance groups on Wednesday applauded a decision by Fannie Mae and Freddie Mac to hold off on an apparent plan to scrutinize mortgages on homes that don’t carry full replacement-value insurance coverage.

The decision by Fannie and Freddie to temporarily suspend enforcement of some guidelines now “creates an opportunity to speak with insurers and other stakeholders to gather more information about the problem of underinsurance, what they can do to help, and how they can best go about it,” the National Association of Mutual Insurance Companies’ Jimi Grande said in a statement Wednesday.

“Requiring full replacement coverage and an annual verification would come at a higher cost and may not always be the best choice for homeowners,” he added.

Fannie Mae and Freddie Mac, the quasi-governmental corporations that buy mortgages from lenders and help support a robust housing market, had posted bulletins in February that some in the insurance community took to mean that the mortgage backers were stepping up enforcement of replacement coverage compliance, starting June 1. That set off alarm bells in an industry that has been moving toward actual-cash-value policies and endorsements, especially for roofs, as a way to reduce losses and give homeowners an option to mitigate premium increases.

NAMIC and Big I, the Independent Insurance Agents and Brokers of America, in April sent a nine-page letter to Sandra Thompson, director of the Federal Housing Finance Agency, which has some oversight over Fannie and Freddie. The letter warned that the rule will disrupt insureds, insurers and agents already dealing with escalating premiums and capacity issues.

But Fannie and Freddie officials suggested earlier this week that the concerns were overwrought: The replacement-coverage guidelines have been in place for years, and the recent bulletins simply clarified things. Some insurance advocates, though, were worried. They have said that the mortgage-buying corporations have rarely enforced anti-ACV rules through the years, and the February updates seemed to signal a new crackdown.

“The FHFA may not believe it was a significant change, but many in the insurance industry have certainly seen it differently and believed these requirements, had they taken effect, would have caused significant damage to the industry and the marketplace,” said Grande, senior vice president for federal and political affairs at NAMIC.

Fannie Mae’s and Freddie Mac’s language in their Wednesday notices was similar, if bureaucratic: “…In coordination with Freddie Mac and FHFA and until further notice, we have decided not to cite findings for noncompliance related to obtaining property insurance replacement cost values for the purposes of determining coverage amount sufficiency, including any failure to obtain lenderplaced insurance for a coverage shortage due to failure to utilize replacement cost value,” reads the May 8 Selling and Service Notice from Fannie Mae.

A spokesman for Freddie Mac said the notice means: “We are temporarily not going to require servicers to take action when we note noncompliance with obtaining RCV during certain procedural reviews.”

NAMIC officials have taken it to mean Fannie and Freddie have hit the pause button and will now obtain more input from stakeholders.

“During this period, we will conduct additional research and industry engagement to evaluate the reported obstacles to lenders’ and servicers’ compliance with our requirements related to replacement cost value,” the Fannie Mae notice reads.

Some Florida insurance carriers have been particularly keen on limiting some types of coverage, after they felt the sting of exaggerated roof claims and heavy losses from full-replacement claims in recent years. In the last 24 months, a number of Florida carriers have begun offering optional ACV endorsements for roofs, and they are breathing a sigh of relief after Wednesday’s announcement.

“This restores consumer choice and allows policyholders to match coverage with their pocketbook,” said Lisa Miller, a longtime insurance industry veteran and a former Florida deputy insurance commissioner.

The Fannie and Freddie notices said that other parts of their guidelines still apply, including the requirement of force-placed insurance when a borrower does not maintain adequate coverage.

“Freddie Mac is still requiring policies to be settled on a replacement cost basis, we’re just pausing citing findings for instances where the servicers do not obtain the replacement cost value estimate to determine if the coverage limit of the policy meets our minimum requirement,” the spokesman said in an email.

NAMIC, which speaks for some 1,500 member companies, said it is ready and willing to meet with Federal Housing Finance Agency officials to develop “a more appropriate policy.”

Rabb is Southeast Editor for Insurance Journal. He is a long-time newspaper man in the Deep South; also covered workers’ comp insurance issues for a trade publication for a few years.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Viewpoint: The 10 Major Risks Shaping Insurance Today

I readily admit that lists of top risks, top threats, and opportunities for insurance are well-trodden ground, and ranking risks in order of importance inevitably triggers debate about which risk should be near the top or bottom, rather than the actual risks on the list.

And from an insurer’s perspective looking down a typical list of risks, some will be dismissed as too far in the future that they can be ignored, or too obvious that they have already been considered and evaluated.

At this year’s Exceedance conference, our theme is to help attendees to ‘See Risk Differently.’ We know the current risk landscape and the state of the insurance industry do not represent business as usual.

This content was originally published as a Moody’s blog. It is republished here with permission.Moody’s prepared a data visual that illustrates each risk with charts, data and information.

But what risks are driving these changes in the landscape, are insurers looking at the right factors, what factors are closer to reality, and what looks more like a hallucination?

Insurers have to consider so many questions. Here’s just one – how will infrastructure that was designed before we knew our climate would change, cope under new extreme pressures, such as the dam failures in Libya and India?

Another question, what’s next for life insurers after the major global catastrophe of a global pandemic not seen since 1918?

Risk is changing, and the business environment is changing. Supply chain shocks, the overhang of the pandemic, and geopolitical risk have escalated economic issues that have been fairly benign in many countries, driving inflation, wages, and raw material price rises, with insurers reaching for an inflationary business playbook that they haven’t used for 20-30 years.

Insurance is a business, and relies on its customers – be they homeowners, life policyholders, or businesses.

Customers face the same risk and economic pressures, but for some, as climate peril risk rises along with losses, insurers have looked to pass premium increases or tighten coverage – with customer satisfaction falling and six million uninsured homes in the U.S.

More customers want cyber insurance, but insurers looking to capitalize on growth have to navigate a volatile risk landscape.

Having a conference theme ‘See Risk Differently’ means we need to show customers how, through better data and better models we can identify new business opportunities.

As part of our preparation for Exceedance 2024, we set ourselves this challenge – 10 risks (in no particular order) that represent some of the major risks shaping insurance today.

These risks are affecting all businesses, the business of risk itself, and the state of the risk landscape. Where to start?

Anytime. Anywhere. The Rapid Proliferation of Cyberattacks

Across all business sectors and all regions, as the world’s reliance on the internet reaches new heights, cyber has become one of the most ubiquitous and prevalent of all the perils that organizations must face, with the potential to stop operations at any time.

With an ever-changing risk landscape, and ever-changing threats, organizations see their cyber defenses tried 24/7, in a battle to close down vulnerabilities looking to be exploited by a wide range of threat actors, from lone hackers, and organized crime operations, to state-backed attackers.

Cyberattacks are now just ubiquitous – an everyday occurrence.

The challenge for insurers is to use frameworks that best capture this peril, as understandably, organizations are looking to their insurers for protection against the worst excesses and losses from cyber risk, and to better manage the risk overall, to make it hard for the criminals perpetrating these attacks.

The Many, Many Tipping Points of Climate Change

Every day seems to deliver a new potential threat or a ‘what if?’ question concerning climate change, a new ‘tipping point’ that will then accelerate the globe over the 1.5 degree Celsius bound and beyond.

But as with all things, it is much more complex than that, individual factors are signs, such as melting sea ice, but it is climate change feedback loops, as one factor accelerates another, where the risk of reaching a definitive tipping point can arise.

Examining the complex network of feedback loops that can accelerate global warming will prove vital to establish whether we are moving fast toward true tipping points. Any accelerations mean less time to mitigate risk, resulting in increased transition risk due to the urgency to respond – potentially impacting insurers and stakeholders including governments.

The Not So Straight Path to Net Zero

Net zero has emerged as the central goal in tackling climate change, but as a measure, it is intrinsically a scientific concept. To keep the rise in global average temperatures within certain limits, physics implies that there is a finite budget of carbon dioxide that is allowed into the atmosphere, alongside other greenhouse gases.

However, net zero is much more than a scientific concept or a technically determined target. It is also a frame of reference through which global action against climate change can be (and is increasingly) structured and understood.

Achieving net zero requires operationalization in varied social, political, and economic spheres.

With such an intricate path to tread to reach net zero, there are risks along the path itself. For instance, carbon capture and storage is widely touted as a route to sequestrate vast quantities of carbon dioxide, but would a sudden release from a ruptured storage facility cause new issues?

New green technology presents many opportunities for insurers to open up new lines of business and look to reduce their exposure to carbon-intensive sectors, but it also presents new risks for the insurance industry.

Getting Reacquainted With Unprecedented Economic Shocks

From the mid-1980s to the 2007 crash, the ‘Great Moderation’ provided a period of stability across a range of economic factors; for many developed and emerging economies, growth, inflation, and interest rates stayed at relatively stable levels.

Post-2007 then saw intervention to maintain stability, and low interest rates to stimulate a return to growth. Central banks supported many nations, including unprecedented levels of support to keep economies functioning during the COVID-19 pandemic.

Whereas the economy was fairly benign in terms of concern, such as low and stable interest rates and inflation for developed economies for most of the 2010s, insurers, similar to most businesses, are now coming to terms with an economic environment where shocks are frequent and unpredictable, and these shocks then ripple through in the form of inflation, higher costs, and higher interest rates.

For example, insurers alongside contending with increasing risks from climate-related events, are also having to contend with significant inflationary pressures, rising labor and materials costs for construction, and higher interest costs.

As consumers feel a cost of living squeeze, policies such as life insurance may not be renewed or canceled to save money, driving up lapse rates. Factoring in these issues is a central aspect of business planning, and the need to pivot in response to shocks is now the norm.

The Challenges of Insurability for Catastrophic Perils

In many U.S. states, and especially states that have suffered significant cat events such as California, Florida, or Louisiana, insurers are having to contend with higher frequency, higher severity cat events, impacting higher value exposure which is located in areas that are becoming higher risk.

In addition, rising business costs, inflation, aggressive litigation, and regulatory pressures, are forcing insurers to reconsider offering coverage to the highest-risk properties.

On the other side, regulators are reacting to this volatile environment, looking to ensure affordable coverage is maintained for consumers. Consumer protection laws such as Prop. 103 in California strains under calls for reform from insurers, to introduce risk-based pricing for perils etc.

But for the consumer, in certain U.S. states, the risk of uninsured properties in towns and cities is growing.

Similar to any other product, insurance costs have to compete with other demands on a consumer’s income, in an economic environment where housing, food, and fuel costs are rising, insurers run the risk of being seen as expensive offering no immediate value for a risk they perceive won’t happen to them.

Insurers need to be viewed as partners in allowing for the economic viability of homeowners, businesses, and the community.

To achieve this, a better understanding of the risk in front of them and efforts needed to mitigate short and long-term risk, allow insurers to be seen as active risk mitigation partners helping consumers to become more resilient and economically stable in the future.

Choppy Waters Instead of Smooth Sailing for Global Supply Chains

The global supply chain is an intricate interplay of many moving parts, but as seen with the COVID-19 pandemic or Russia’s invasion of Ukraine, the smooth functioning of the global supply chain that the world has enjoyed could be an exception, rather than the rule.

Production shortages during COVID saw whole industries such as car manufacturing, air travel, and tourism, grind to a halt, with a long, stumbling road back to recovery.

Then Russia’s invasion of Ukraine saw shocks to energy prices as Russia’s energy exports were turned away by Ukraine’s allies, and foreign businesses retreated from Russia.

Construction costs – materials and labor, can represent a sizeable slice of a property insurer’s costs, and double-digit cost increases have had to be passed through in response to supply shortages, price increases, and rising labor costs in a tight labor market.

Businesses are rapidly relearning how they approach global supply chains, assuming that nothing is certain, and building resilience and contingency into their systems. Identifying the new vulnerabilities in each supply chain, recognizing that the leanest approach may not be the best fit, and that supply continuity is now the best outcome, will help to minimize future supply shocks.

Perennial Wars Rise Back to the Surface

Concern around geopolitical issues, although ever present, had been muted, as globalization and world trade looked to create new partnerships and break down barriers for many businesses over the last 20-30 years.

But with many states now emboldened and looking to flex their new dominance, old ‘perennial’ wars, and new conflicts, have either been brought to the fore, making it more difficult to conduct world trade in a time where conflicts are reigniting with growing regularity.

Insurers have to understand the multitude of geopolitical conflicts, and how many of these are perennial conflicts, they do not go away or get resolved, but they bubble to the surface, and can quickly escalate.

Terrorist events can be a trigger, and ignite conflicts; these perennial disputes can place infrastructure, shipping routes, and resources at risk, potentially writing off business for years.

No Quick Fix for Crumbling Infrastructure

Nations have infrastructure booms, for the U.S., it was 1950-70, after which investment dropped off. As a result, vital infrastructure is predominantly 50-70 years old.

For developing nations, a different issue: by 2050, there will be 15 million miles of paved roads built around the world in total, enough to encircle the globe 600 times, and 90 percent of the road building will occur in developing nations. But is this new infrastructure going to be resilient in the future?

Although a direct issue for the insurer that insures an infrastructure asset, inadequate dams, flood defenses, drainage, power systems, and poor housing – all contribute to escalating risk for insurers who are increasingly paying out for the events exacerbated by poor infrastructure.

This is set to worsen as infrastructure struggles to cope with an environment facing extremes – be it heat, cold, rain, snow, or wind. Where infrastructure fails, businesses that rely on that infrastructure will also be hit, potentially driving up business interruption losses.

The Return of Long-Tail Liabilities

There is a growing need for (re)insurers to be prepared and even ensure reserves for the rise of ‘long-tail’ claims from many potential sources.

Social inflation factors, where awarded losses, higher litigation rates, or simply the backlog of court cases post-COVID seeing legislators extending claim deadlines or adjusting claim eligibility dates allowing more claimants to gain redress, bring uncertainty.

One source is simply where claims come in well after an insurance policy has expired. These have seen a resurgence recently; Munich Re reported a 33 percent year-on-year rise in ‘long-tail’ claims in 2023, with policies dating back as far as 2012.

Changes to the statute of limitations – the maximum time to make a claim can change, such as for molestation claims in the U.S., can reopen liabilities.

Insurance ‘archaeologists’ dig into past policies, such as potential claims navigating ‘Pollution Exclusions’ introduced in the mid-to-late eighties liability and/or property insurance policies. Claims from pollution or liability from per- and poly-fluoroalkyl substances (PFAS) keep the scrutiny on past policies.

Where policy wordings are ambiguous or have not kept up with the rising list of potential claims and attempts at litigation, such as cases ranging from COVID-19 business continuity claims in Europe, faulty products, to data breaches/data protection, long tail liabilities can arise.

Give and Take in Longevity and Mortality

From improvements in sanitation, housing, and education, the fight against infections with the development of vaccines and then antibiotics, new technology, pharmaceuticals, and screening, have seen life spans increase to 84-85 years old, on average, in eight countries.

Breakthroughs in transplants, gene therapy, blockbuster drugs that target cancers, and AI speeding up research, will all help to reduce the likelihood of premature death and extend lifespans further. The world already has nearly a million centenarians, around 1,000 at 110 years, and 68 at 115 years or greater.

With the COVID-19 pandemic, the issue of excess deaths came to the fore, with those over 65, and especially over 75 years old, being particularly hard hit, and reversing some of the top-line gains in longevity.

But the focus is now turning to ‘healthy life’ years, years without chronic illness or disability, and this, as an example, for the EU countries is at around 63-64 years. In developed and developing economies, issues around obesity, poor diet, alcohol, drugs, sedentary lifestyles, plus insufficient access to appropriate healthcare, are countering longevity gains, and making it hard to increase ‘healthy life’ years.

This then places pressure on health and social care systems as more people struggle with chronic illness and disability in their later years.

For those delivering life assurance or financial security products to aging populations, the marrying up of exceptional longevity progress, and extraordinary medical breakthroughs, together with the other side of the balance sheet, of emerging viruses and possible pandemics, Long COVID, and lifestyle and healthcare concerns, make it much more difficult to predict future trends without analyzing a wide range of factors.

For these ten risks, such as cyber illustrated above, we have also brought them to life in an interactive data visualization story, to access this, click here.

These ten risks are designed to challenge, raise debate, call for analysis, and help start conversations on embracing a risk landscape that seems more complex and opaque than in previous times.

We look forward to examining some of these risks at Exceedance, and to building a mindset that is primed and ready to see risk differently.

Was this article valuable?YESNO

WRITTEN BYRobert Muir-Wood

Robert Muir-Wood, chief research officer, for Moody’s RMS, works to enhance approaches to natural catastrophe modeling, identify models for new areas of risk, and explore expanded applications for catastrophe modeling. He has more than 25 years of experience developing probabilistic catastrophe models. He was lead author for the 2007 IPCC Fourth Assessment Report and 2011 IPCC Special Report on Extremes, and is chair of the OECD panel on the Financial Consequences of Large Scale Catastrophes. He is the author of seven books, most recently: “The Cure for Catastrophe: How We Can Stop Manufacturing Natural Disasters.” He holds a degree in natural sciences and a doctorate both from Cambridge University and is a visiting professor at the Institute for Risk and Disaster Reduction at University College London.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

An updated guideline from Fannie Mae, if it stands, could throw a wrench into the property-casualty insurance industry’s move toward actual cash value for more homeowners and condo coverage.

A Fannie Mae spokesperson said the government-backed mortgage corporation, which supports a large share of the U.S. mortgage market, has clarified a long-standing guideline that requires that insurance polices provide replacement value coverage for most homes with mortgages.

“Fannie Mae’s longstanding Selling Guide policy requires property insurance claims to be settled on a replacement cost basis. Updates made to Fannie Mae’s Selling Guide in December 2022 and February 2024 further clarified that Fannie Mae’s well-established property insurance requirements do not allow claims to be settled on an actual cash value basis, as well as related lender and servicer responsibilities,” the corporation noted.

Freddie Mac, which mostly buys loans from smaller lenders, has also had its replacement-cost requirements in place for years, but early this year reiterated the stand in updated guidelines.

Some in the insurance industry have said the updates appear to mark a new emphasis on replacement coverage and away from ACV. An April 17 letter from the National Association of Mutual Insurance Companies and Big I, the Independent Insurance Agents and Brokers of America, urged the Federal Housing Finance Agency to suspend the changes immediately. The groups warned that the rule will disrupt insureds, insurers and agents already dealing with escalating premiums and capacity issues.

“Requiring, without exception, that all consumers with mortgages owned by Fannie Mae and Freddie Mac obtain full replacement cost coverage will logically, by the very nature of this mandate, exacerbate existing challenges,” the letter reads. “While the GSE guidance is no doubt well-intentioned, it establishes requirements that will have a real-world impact on the many homeowners who are unable to satisfy the coverage requirements or who are forced to purchase a higher-cost insurance product in order to do so.”

Grande

Insurance agents would be left in a tough position by such a rule change and would have to inform homeowners that an option to help limit premium spikes is about to be taken off the table, the letter noted. And some property insurers have entire product lines that offer ACV for homes with mortgages, policies that are favored by insureds who may not be able to afford replacement-based premiums, said Jimi Grande, senior vice president for federal and political affairs at NAMIC.

It’s not clear how much of a change the guidelines create, and why the replacement value rules are in place now, in the midst of a hard market and burgeoning loss costs for property insurers. But the NAMIC and Big I letter may have done some good: Federal housing finance officials are expected to announce later this week that they are willing to put a pause on the new guideline and speak with stakeholders.

“We’re thankful. It sounds like FHFA will postpone this rule and let stakeholders come together and talk about it,” said Nathan Riedel, senior vice president for federal government affairs.

Offering actual cash value has been a growing trend around the country in recent years, but especially in Florida and especially for roofs. Insurer advocates have called ACV a simpler, fairer way to cover roofs in the wake of thousands of Florida roof claims that insurers said were fraudulent or exaggerated by some public adjusters, unscrupulous roof contractors, and by some plaintiffs’ lawyers.

Florida lawmakers have repeatedly introduced legislation that would have allowed more policies to cover only the current value of roofs, as opposed to full replacement value, which can add thousands of dollars to the cost and hundreds of dollars to premiums.

“It’s about 25% more expensive to go with replacement value than with ACV,” said Scott Johnson, of Tallahassee, a longtime insurance educator, author and consultant.

Senate Bill 1728, introduced in the Florida Legislature in 2022, came close to allowing more policies to provide only ACV coverage for some homeowner roof claims. The bill passed the Senate that year but died in the House of Representatives.

Since then, though, the Florida Office of Insurance Regulation has allowed something of a work-around: Regulators interpreted existing state law to allow carriers to offer optional endorsements that limit roof replacements and limit the amount that a policy will pay to cosmetically match new roof material to old. Several carriers have moved quickly to offer the endorsements in the last year or so, giving insureds an option.

In 2022, Florida Senate Bill 4D also revised building codes. The codes now no longer require full roof replacements when only part of the roof is damaged. Florida court rulings also have eased the replacement requirement in some cases.

In Kentucky last fall, the state Department of Insurance also weighed in on the issue. It posted an advisory opinion, essentially allowing insurers to avoid full roof replacements if the same type of shingle is used for repairs, even if the new shingles don’t exactly match the old ones in color.

Grande, of NAMIC, speculated that the FHFA may have had good intentions to protect homeowners, but the agency did not consult with enough experts in the insurance world. Perhaps regulatory officials had heard from consumer groups that some people weren’t getting full replacement value from insurers when their homes were damaged, and the agency wanted to help assist residents, Grande noted.

“That’s a nice sentiment but it was horribly ignorant and wrong,” he said. “It’s weird that no one in the food chain caught that before the guidelines were published.”

Riedel

Removing ACV coverage undermines a choice that many homeowners have embraced as a way to reduce premium increases in recent years, he and Big I’s Riedel pointed out.

A Fannie Mae official said that the clarifications “were intended to help assure borrowers have sufficient property coverage in the event of a loss and promote sustainable homeownership.”

Replacement costs also have been a tricky issue for some insurance agents in recent years. An insurance carrier’s replacement cost estimator tools are often considered proprietary, and Florida statutes and agents’ contracts bar lenders from requiring agents to provide the cost estimators, explained B.G. Murphy with the Florida Association of Insurance Agents.

“The new guidance to sellers/servicers of Fannie/Freddie-backed mortgages will likely reignite this problem for Florida’s independent insurance agents,” Murphy wrote in a blog post last week.

It is unclear the number of homeowners with mortgages in Florida and elsewhere that have opted for actual cash value policies. Florida regulators and officials with the state-created Citizens Property Insurance Corp. could not be reached Monday.

This is not the first time Fannie and Freddie have shaken the Florida housing and insurance markets.

In early 2022, the corporations began requiring lending institutions to evaluate the condition of condominium buildings before approving loans, in the aftermath of the Champlain Towers South collapse that killed 98 people.

A year later, some Florida-domiciled carriers withdrew from the Demotech rating firm’s financial stability rating system. But Freddie Mac caused some consternation when it temporarily delayed approval of another rating firm’s ranking system for insurers.

Likewise, the latest rule change has caused “uncertainty and apprehension” as the rule implementation date approaches, the NAMIC and Big I letter said.

Update: This article was updated May 7, 2024 to include more information from Fannie Mae and Freddie Mac, and to show that the replacement-value guidelines have been in place for a number of years.

Rabb is Southeast Editor for Insurance Journal. He is a long-time newspaper man in the Deep South; also covered workers’ comp insurance issues for a trade publication for a few years.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

by Sarah Gail Fri, April 26th 2024 at 5:07 PMUpdated Fri, April 26th 2024 at 6:34 PM

PENSACOLA, Fla. — The home insurance crisis in Florida could possibly see some stabilization.

But that may not be enough for some homeowners.

A survey by real estate brokerage Redfin found more than 10 percent of homeowners moved or plan to move because of the climbing insurance costs — or lack of coverage altogether.

But in our area, we’re seeing something slightly different.

Local realtor Christina Leavenworth says she’s actually seen more people backing out of moving to Florida instead.

“We have had buyers where they have gone under contract, they’ve done the inspections, the home is nearly perfect — there’s nothing wrong with it,” Leavenworth said, “And then they get an insurance quote for $4,000 — which really isn’t that bad in this market — and they go you know what, I don’t want to move to Florida.”

However, Leavenworth says things are looking up.

“We are seeing some relief,” she said. “I’ve seen that across the board. As we’re getting quotes, they’re inching down. It’s nothing amazing but they’re inching down.”

Mary Jordan is an insurance agent and owner of Gulf Coast Insurance.

She says legislation passed in 2023 is already making a difference with the rates.

With it, fewer lawsuits were filed and that helped open up the market again.

“Which made reinsurers carriers want to be back in our market because they saw a more positive affect,” Jordan said.

And with more carriers, there is more supply for the high demand.

“What my speculation would be is we’re going to start seeing rates being reduced,” Jordan said.

But Jordan says it can take up to two years to see the bigger reductions.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

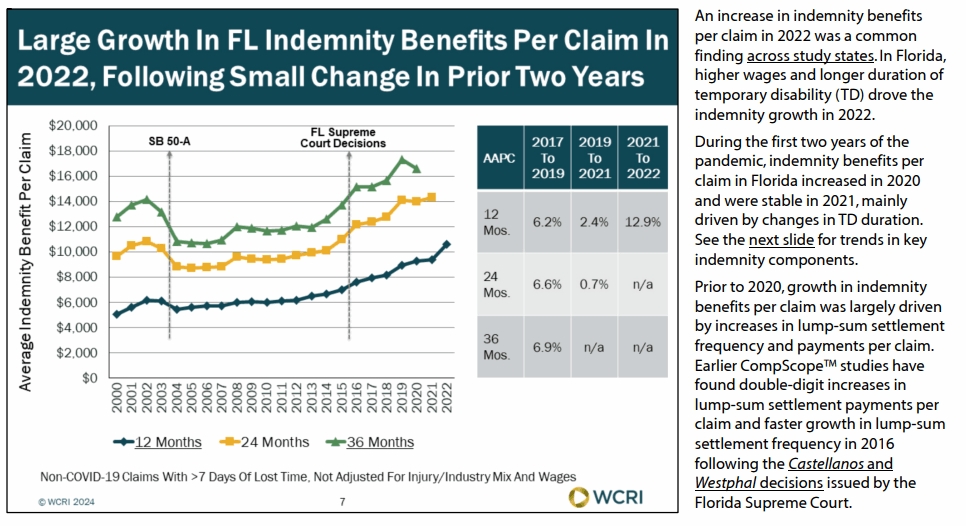

Florida Saw Jump in Workers’ Comp Cost per Claim in 2022-23, WCRI Report Shows

Call it the effects of wage creep during the pandemic, along with a little bit of creep in the duration of benefits.

Employers and insurers in Florida saw a 7% increase in total cost per workers’ compensation claim in 2022 and 2023, to just over $30,000 on average, due largely to higher wages and longer temporary disability benefits duration. That was the finding of an analysis by the Workers Compensation Research Institute, which compared COVID-19 pandemic-era costs in Florida and 16 other states.

“The large indemnity growth in 2022 was mainly driven by increases in the average preinjury weekly wage of workers with injuries and duration of temporary disability. In particular, wages in Florida grew 9.5 percent in 2022, faster than the increases in prior years,” notes the report, authored by WCRI researcher Rebecca Yang. Other study states saw similar cost increases.

The work echoed other studies that have found that as employers rebounded from the pandemic shutdowns, they were forced to pay higher wages to attract workers. That led to higher payrolls and higher weekly benefits for injured employees.

The trend was highlighted late last year when the Florida Division of Workers’ Compensation raised the 2024 maximum weekly indemnity benefit to reflect the big jump in average weekly wages. The average wage rose from $1,099 in 2021 to $1,260 in 2023 – a 15% increase. That much of an increase had not been since the high-inflation days of 1980, which saw a 20% spike in wages from two years earlier.

Click on the chart for an enlarged image.

The reasons for a half-week increase in temporary disability benefits duration were also related to the economic realities of the pandemic. In many states, including Florida, TD duration increased in 2020, declined or remained stable in 2021, then increased again in 2022. High unemployment early in the COVID era may have kept some injured workers out of a job, leading to longer injury or benefits duration times, the WCRI report said.

Later, as employment rose nationwide, “the tight labor markets and the potential workforce shortages associated with this reality may have led to longer working hours and worse overall health among current employees.”

The study underscored what other analyses have found – that many employers were forced to hire less-experienced workers in 2022, which may have led to higher injury rates in some job classifications. Post-pandemic, employers have seen an increase in comorbidities for workers. Some employees may have had problems accessing medical care due to a shortage of health care professionals, the study said.

“These factors may have led to more severe injuries, prolonged recovery, and slower return to work,” the report noted.

The analysis found that duration of temporary disability in Florida increased in 2022 in most industry groups and across age groups with workers aged 35 and above at the time of injury. The report can be accessed here.

It’s too soon to know if the higher costs will put pressure on workers’ compensation rates in Florida. The state, like most others, has seen a steady drop in comp rates over the last two decades. Late last year, Florida regulators approved a 15% average decrease in rates.

WCRI also found that medical payments per claim have remained stable in recent years, in contrast to a 5% per-year increase in the years from 2017 to 2019. Part of the stability was due to a drop in the utilization of medical services at ambulatory surgery centers and other non-hospital providers, the report noted.

That cost stability could be positively impacted, at least to some degree, by new Florida limits on emergency room costs. Florida Gov. last week signed House Bill 989, which, among other changes, clarifies that emergency care, except those procedures subject to the maximum reimbursement allowance, must be set at 250% of Medicare’s rates, unless governed by a contract.

The “agency bill,” which addresses a wide range of issues identified by the Florida Department of Financial Services, also requires DFS to work with actuarial firms to develop maximum reimbursement allowances for emergency services.

Rabb is Southeast Editor for Insurance Journal. He is a long-time newspaper man in the Deep South; also covered workers’ comp insurance issues for a trade publication for a few years.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Heritage Insurance Holdings Inc. (HRTG) on Wednesday reported earnings of $14.2 million in its first quarter of this year, about the same as earnings for Q1 of 2023, but down from the $31 million in net income reported for the fourth quarter of 2023.

The Tampa-based property and casualty insurance holding company is the parent company of Heritage Insurance, Narragansett Bay Insurance and Zephyr Insurance. The holding firm posted revenue of $191.3 million in Q1, up 8% from the first quarter last year, thanks in part to reduced exposure and to significant rate increases.

The firm’s combined ratio was 94% for Q1, a slight improvement over last year’s quarterly number, the company’s financial statements show.

The black ink reflects a significant improvement from the Heritage financial picture in 2021 and 2022, at the depths of what has been called the Florida property insurance crisis. At the end of Q1 2022, Heritage holdings reported a $31 million net loss.

Since then, a number of Florida insurers have seen a significant reduction in litigation expenses, a key metric behind the crisis. And Heritage has continued to reduce its exposure in Florida and other states. Heritage held 182,673 policies in Florida at the end of 2022 and 529,907 policies in all 17 states in which its subsidiaries write. By the end of the first quarter this year, the number of Florida policies had dropped to 147,9654. In all 17 states, policies in force fell to 436,955 — a drop of almost 18% in less than 18 months.

But the cutbacks were not across the board. Heritage said in a news release that it had increased its commercial residential premium significantly.

“As part of our exposure management strategy, we continue to grow our policy count in products and geographies which are profitable and reduce our policy count in unprofitable and over concentrated areas,” the release noted.

“The management team is resolute in our focus to generate underwriting profits across our footprint, maintain adequate rates, ensure selective underwriting, and employ meticulous but fair claims handling,” CEO Ernie Garateix said in a statement.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com. I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Southeast Seas Rising Faster than Other Regions, ‘Turbocharging’ Floods, Report Finds

From the Rio Grande to the Outer Banks, sea levels are rising faster than most other parts of the world, blocking the outflow of rivers and streams and causing inland flooding that would not have been seen just a few years ago.

That’s the conclusion of an analysis by The Washington Post and a University of South Alabama professor, published last week. The study found that flooding in many low-lying areas across the coastal Southeastern U.S. will worsen as seas rise. But it pointed out that it doesn’t take record-breaking rain events to flood large areas – even relatively moderate rainfall has nowhere to go when higher seas and unusually high tides are present.

Higher seas are now “turbocharging” flash floods, damaging homes, autos and businesses and human lives, the newspaper reported.

The authors looked at data from the National Weather Service, combined with tide gauges and satellite data, to show that sea levels along the Southeast coast, including the Gulf of Mexico and South Atlantic coasts, have risen at twice the global rate. In some areas, ocean levels have risen three to four times faster in the last 13 years than they had in the previous 30.

In Dauphin Island, Alabama, on the Gulf, the water rose about a tenth of an inch per year from 1967 to 2009. Since 2010, the seas have climbed almost 7 inches, or almost half an inch per year, the analysis showed. A 2023 flood in nearby Fowl River showed how a modest rain event collided with higher Gulf waters, spreading out into residential neighborhoods and causing heavy flooding.

Scientists are not certain why the coastal region is seeing faster ocean rise than other regions. But some have theorized that ocean currents are moving warmer water deep into the Gulf. Warm water expands, causing seas to climb.

The report was published one day before the Alabama Department of Insurance urged residents to purchase flood insurance before another flood event strikes.

The Federal Emergency Management Agency “says just an inch of water can cause more than $25,000 worth of damage. Without a flood policy, you would have to pay for repairs and replacements on your own,” the department noted.

FEMA’s flood cost tool shows estimated damage as waters rise. At 48 inches, less than what some Fowl River residents experienced last summer, damage to a home can top $103,000.

Photo: Floodwaters after a thunderstorm on April 10, 2024, in New Orleans. (Chris Granger/The New Orleans Advocate via AP)