Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

A broken bottle of whipped cream-flavored vodka may have turned into a just dessert for an Orlando-area woman who allegedly filed false insurance claims.

Florida authorities announced Thursday that Anita Jovic, of Seminole County, has been charged with insurance fraud and other crimes after she claimed that a bottle of Pinnacle vodka – whipped cream flavor – had broken and caused severe injuries to her hand.

The woman submitted a photograph and a fraudulent hospital invoice to Broadspire, a Georgia-based workers’ compensation and health insurance company, Florida’s chief financial officer said in a news release. Another claim was made to Beam Suntory, the liquor manufacturer, under the name of Annette Jobita.

Broadspire identified many similarities between the two claims and alerted the state Department of Financial Services’ investigative division, CFO Jimmy Patronis said.

An investigation found that Jovic had filed five product liability claims using numerous false identities, attempting to defraud Beam Suntory, Broadspire and Travelers Insurance of more than $30,000. She received some $13,000 in settlement payouts between 2017 and 2022, the DFS statement said.

Jovic this week turned herself into the Seminole County Sheriff’s Office.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Three Florida insurance carriers, one large and two small, are seeking approval for major rate increases, with one condominium policy increase as high as 103%.

Citizens Property Insurance Corporation’s board of governors this week voted to file for a 14.2% average increase for personal lines and a 12.3% spike for commercial policies. The rate change, if approved by the Florida Office of Insurance Regulation, would take effect Nov. 1.

The rate appears to be slightly above Citizens’ statutory glidepath restrictions, which limit increases to no more than 12% for 2023. That’s because it includes surcharges and fees paid, including payments to the Florida Hurricane Catastrophe Fund, a Citizens spokesman said.

But the rate hikes are far below what is actuarially indicated if Citizens had no rate caps: Officials noted that increases of almost 58% for personal lines and almost 69% for commercial policies are indicated, according to information provided to the board of governors.

It’s not certain regulators will approve the rate increase. In 2022, Citizens filed for an 11% increase but OIR trimmed it to 6.4%, despite a push to make Citizens less competitive with the primary market carriers.

On Thursday, the OIR held public hearings on massive increases requested by two smaller insurers: First Community Insurance, a Bankers Insurance subsidiary; and Kin Interinsurance Network.

First Community, based in St. Petersburg, raised its average rate by almost 45% in November for more than 25,500 homeowners, then asked for approval under Florida’s use-and-file practice. About the same time, First Community announced it would non-renew most of those policies as it exits the homeowners market in five Southern states.

In other words, thousands of Florida homeowners saw an average premium increase of $847 last fall, only to have their policies nonrenewed, starting next week. If approved by OIR, it would be the fourth rate increase in three years for First Community. OIR approved a 50% rate hike in 2021 – double what the carrier had requested.

First Community and Bankers Chief Financial Officer Scott Charbonneau said at the hearing that the insurer had seen more than $50 million in underwriting losses since 2020, mostly due to hurricanes in Florida and Louisiana. The insurer also has been hit with heavy litigation costs in Florida, and reinsurance costs jumped 45% in 2021 and 83% last year, he said.

The rate request was filed before the Florida Legislature late last year approved significant reform measures designed to limit claims litigation and attorney fees for property insurers. Charbonneau said the legislation should help reduce loss costs in the long run, but the “deterioration of the loss experience” will offset that, and could have led to even more rate increases had the company stayed in the Florida market.

A sweeping tort-reform bill signed into law last week “would not have changed our decision,” Charbonneau said. Its sister company, Bankers Insurance, also stopped writing homeowner policies in Florida last June.

First Community and Bankers, which has been domiciled in Florida since 1976, will maintain a tiny presence in the state, with some HO-4 tenants insurance and some dwelling fire policies – only about $500,000 in total premium.

“Is there hope that Bankers could come back in?” Charbonneau asked. “I think that door hasn’t completely shut but we’ll need to see more in the development of these reforms in the marketplace. We would love to come back in to the Florida marketplace if the time is right but we have no plans in the near future, at all.”

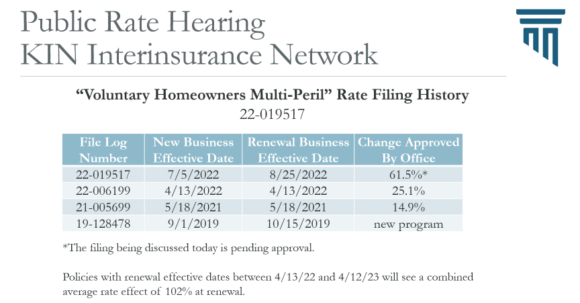

Later Thursday, OIR held a hearing on some startlingly large use-and-file rate increases proposed by Kin Interinsurance Network – of 61.5% for HO-3; 84.3% for DP-3; and 103.2% for condominium policies.

Conlin (Linkedin)

Dan Ajun, chief actuary, and Angel Conlin, CEO of Kin, said the large numbers reflect soaring reinsurance prices, competitors’ recent rates, Kin’s surplus levels and a need to keep the company on a sound financial footing. The increases took effect last July for new business and last August for renewals, before Florida lawmakers enacted some of the litigation-limiting reform measures.

But the Kin officials said that Senate Bill 2A, approved at a special legislative session in December, may not have a significant impact on Kin’s rates going forward. That’s because SB 2A outlawed assignment-of-benefits agreements in homeowner policies, but Kin, launched in 2019, has already offered premium discounts for policyholders who refuse AOBs.

Kin is a reciprocal exchange insurance company owned by policyholders. It operates in several Southern states and in California. Kin Interinsurance Network, which provides Florida homeowner policies, is based in St. Petersburg.

Kin’s HO-3 rate increase affected some 27,150 homeowners, raising their annual premiums an average of $1,395, the filing shows.

Comments on the Kin and the First Community rate increases can be emailed to ratehearings@floir.com by April 13.

Rabb is Southeast Editor for Insurance Journal. He is a long-time newspaper man in the Deep South; also covered workers’ comp insurance issues for a trade publication for a few years.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

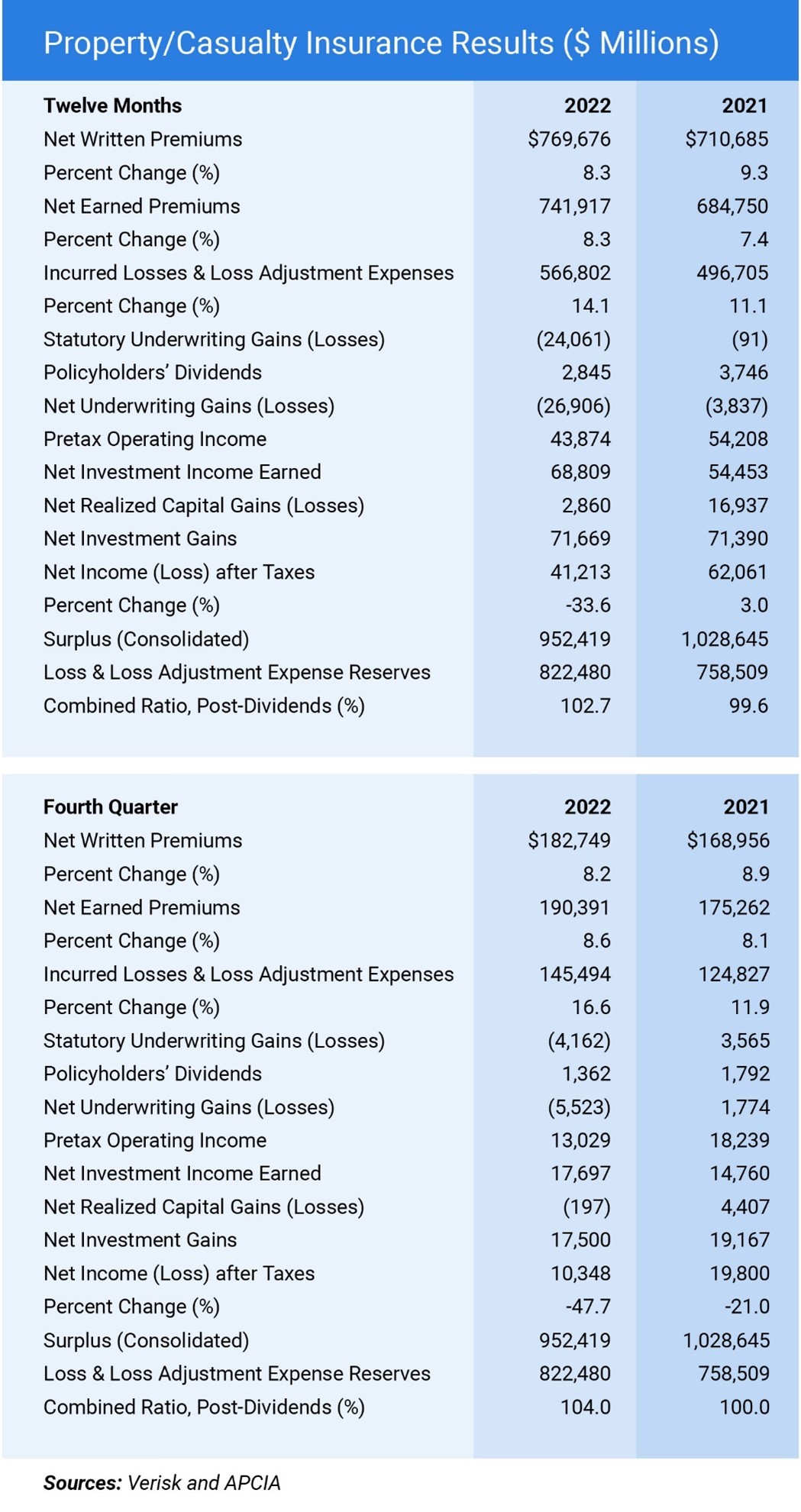

Key financial results for private U.S. property/casualty insurers significantly worsened in 2022 from a year earlier, according to preliminary results from global analytics provider Verisk and the American Property Casualty Insurance Association (APCIA).

The industry recorded a net underwriting loss for 2022 of $26.9 billion, more than six times the $3.8 billion underwriting loss in 2021. The underwriting loss in 2022 was the largest the industry has seen since 2011.

“The insurance industry is being hammered by increasing input costs, natural catastrophes, legal system abuse, and resistance in some states to adequate rates,” said Robert Gordon, senior vice president, policy, research & international for APCIA. “Insurers suffered a 14.1% increase in incurred losses and loss adjustment expenses, contributing to a more than $76 billion contraction in insurers’ surplus at a time when loss exposures are rapidly growing. In 2023, insurers are faced with a significant challenge to close the rate gap in order to meet their growing cost of capital.”

Policyholders’ surplus recovered somewhat to $952.4 billion from Q3 2022’s $911.7 billion total, but still remains below that of year-end 2021 driven primarily by the large amount of unrealized capital losses accrued during 2022. Insurers’ rate of return on average policyholders’ surplus, a measure of overall profitability, declined to 4.2% in 2022 from 6.4% in 2021.

Verisk and APCIA said U.S. P/C net income fell 33.6% to $41.2 billion in 2022, compared with 2021. The combined ratio deteriorated to 102.7% in 2022, from 99.6% in 2021.

The preliminary results outlined in the table below are consolidated estimates based on annual statements filed by insurers with insurance regulators. The results are based on about 94% of all business written by U.S. property/casualty insurers, Verisk and APCIA said.

“Hurricane Ian and the effects of inflation resulted in major losses for property insurers last year, while accident severity continued to plague personal and commercial auto lines,” said Neil Spector, president of underwriting solutions at Verisk. “To remain profitable in these challenging times, many insurers are looking for new ways to reduce expenses, increase efficiencies, and enhance the customer experience. And they’re finding help from an ecosystem of advanced technology and analytics that is growing every day.”

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Citizens Property Insurance Corp. has weighed in on a question that could shake up the appraisal process in Florida insurance claims disputes, urging state regulators to require that appraisers be licensed adjusters.

In a motion to intervene in a petition filed with the Florida Department of Financial Services, the state’s largest property insurer said a determination that appraisers do not have to be adjusters would have a “perverse and unintended outcome,” and could potentially impact premiums and assessments paid by Florida policyholders.

The controversy arose in January in the case of an infamous property adjuster and appraiser whom Citizens and other insurers said had repeatedly blocked company adjusters from accessing property and even threatened at least one insurer’s adjuster with violence. An administrative law judge recommended that Scott David Thomas’ adjuster’s license be suspended for two years and that he pay a $5,000 fine.

DFS officials can accept the judge’s decision or may take it a step further and revoke his adjuster’s license altogether. Thomas can appeal the decision to a Florida appeals court.

In its recommendation to the administrative law judge, DFS noted that “because the work of an appraiser falls within the statutory definition of ‘public adjuster,’ an appraiser is subject to the requirements of the Florida Insurance Code” and the adjuster’s code of ethics.

That raised concerns for appraiser associations and the Windstorm Insurance Network, which provides education courses for appraisers. The network, known as WIND, along with the Insurance Appraisal and Umpire Association, and the Property Loss Appraisal Network, filed a petition Feb. 23 with DFS, seeking clarity on the issue.

Appraisers are widely used to help settle the value of damages in claims disputes. But requiring them to be licensed adjusters could cause a shortage of appraisers in Florida, WIND, the associations, and some insurance attorneys have said. Many appraisers are considered experts in their fields, such as engineering, but may not want to take the time to become licensed adjusters, the appraiser associations have said.

Citizens disagrees and noted in its motion that without the licensing requirement, troublemakers like Thomas could continue to serve as appraisers, perhaps leading to inappropriate valuations and higher costs to insurers.

“This would be the natural consequence of granting the relief requested by petitioners despite the fact that much of the problematic conduct that led to the administrative complaint against Mr. Thomas involved his actions in appraisal proceedings, including appraisal proceedings involving policyholders of Citizens,” the insurer’s motion reads.

State law appears to require that appraisers must be licensed, Citizens’ senior corporate counsel, Russell Kent, wrote in the motion.

Citizens, created by the Florida Legislature in 2002 as an insurer of last resort, has a “special interest” in the matter. Kent’s motion noted that a DFS decision that avoids a license requirement would have a significant impact on Citizens, which participated in 4,605 appraisal proceedings in 2022 and has already been party to 3,471 in the first few months of 2023.

“Citizens’ circumstances are unique among insurers in Florida,” the motion explains. “Consequently, Citizens respectfully requests that the Department allow it to intervene in this declaratory statement proceeding.”

The filing pointed out that licensed attorneys are exempt from adjuster licensing requirements and could serve as appraisers.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

PROPERTY

1. Condominium and Cooperative Associations – HB 1395/SB 154

By Rep. Lopez and Senator Bradley

This is a cleanup package for the Surfside bill that passed in special session last May. The House bill passed its first of three committees on March 23rd by a vote of 11-0. The Senate bill is ready to be heard by the whole chamber.

SB 154 revises the milestone inspection requirements for condominium and cooperative buildings that are three or more stories in height to:

· Limit the milestone inspection requirements to buildings that include a residential condominium or cooperative;

· Provide that the milestone inspection requirements apply to buildings that in whole or in part are subject to the condominium or cooperative forms of ownership, such as mixed-use buildings;

· Clarify that all owners of a mixed-use building in which portions of the building are subject to the condominium or cooperative form of ownership are responsible for ensuring compliance and must share the costs of the inspection;

· Delete the 25-year milestone inspection requirements for buildings that are within three miles of the coastline;

· Authorize the local enforcement agencies that are responsible with enforcing the milestone inspection requirements the option to set a 25-year inspection requirement if justified by local environmental conditions, including proximity to seawater;

· Authorize the local enforcement agency to extend the inspection deadline for a building upon a petition showing good cause that the owner or owners of the building have entered a contract with an architect or engineer to perform the milestone inspection services and the milestone inspection cannot reasonably be completed before the deadline;

· Provide that the inspection services may be provided by a team of design professionals with an architect or engineer acting as a registered design professional in responsible charge; and

· Clarify that an association must distribute a copy of the summary of the inspection reports to unit owners within 30 days of its receipt.

Requires the Florida Building Commission to establish by rule a building safety program to implement the milestone inspection requirements within the Florida Building Code. The commission must specify the minimum requirements for the commission’s building safety program by December 31, 2024, including inspection criteria, testing protocols, standardized inspection and reporting forms that are adaptable to an electronic format, and record maintenance requirements for the local authority having jurisdiction.

Revises the requirement that all personal lines residential policies issued by the Citizens Property Insurance Corporation must include flood coverage to exempt condominium or cooperative units that are in certain flood-risk areas and above specified floors in a building.

Clarifies that both the condominium or cooperative unit owner and any person authorized by any owner as his or her representative may inspect the official records of the association.

The bill provides additional presale notice requirements in contracts for sales of a unit by a developer or non developer. This provision is similar to current contract notices to unit owners obligated to furnish certain governing documents to the prospective buyer of a unit more than three days before closing for sales by a non developer or 15 days before closing for sales by a developer. A contract that does not conform to these notice requirements is voidable at the option of the purchaser prior to closing.

2. Collateral Protection Insurance on Real Property HB 793/SB 410

By Rep. Fernandez-Barquin and Sen. Garcia (I)

This is the first time this type of language has been introduced in Florida. The House and Senate bills have received three committees of reference. SB 410 passed the Banking and Insurance committee by 11-0. With the majority of House subcommittees ending in week 5, HB 793 needs to be heard in its second committee reference in the next two weeks or the bill is dead.

The bill creates a new section of law dealing with real property collateral protection insurance, also known as “forced-placed” insurance. The bill seeks to promote the public welfare by regulating collateral protection insurance on real property, create a legal framework which collateral protection insurance on real property may be written in the state, help maintain the separation between mortgage lenders or servicers, and insurers or insurance agents, and minimize the possibilities of unfair competitive practices in the sale, placement, solicitation, and negotiation of collateral protection insurance.

The scope of the bill applies to insurers and insurance agents engaged in any transaction involving collateral protection insurance on real property and all collateral protection insurance written in connection with mortgaged real property, including manufactured and mobile homes.

3. Insurance HB 505/SB 418

By Rep. Berfeild and Sen. Perry

This bill has turned into the Insurance Omnibus bill for the 2023 Legislative Session. As usual for every session the House and Senate versions will move through the process picking up smaller industry specific language and turning the bill into a train. On March 23, HB 505 received a favorable vote from the State Administration and Technology Appropriations Subcommittee by a vote of 14-0 and is currently waiting to be heard Commerce Committee. The Senate bill is still waiting to be heard in its final committee.

The Senate bill is ahead of the House version and has the following provisions:

· Allows a residential property insurer’s rate filing to estimate projected hurricane losses by using a weighted or straight average of two or more models approved by the Florida Commission on Hurricane Loss Projection Methodology.

· Provides that, in lieu of themselves, the Executive Director of the Citizens Property Insurance Corporation, and the Director of the Division of Emergency Management, respectively, may appoint a designee to be a member of the Commission on Hurricane Loss Projection Methodology.

· Authorizes an insurer to file a personal lines residential property insurance rating plan that provides premium discounts, credits, and other rate differentials based on windstorm construction standards developed by an independent, not-for-profit, scientific research organization.

· Limits the requirement that an insurer provide a policyholder who has an automatic bank withdrawal agreement with the insurer with 15 days advance written notice of any increase in policy premiums. Instead, notice will only be required for premium increases that result in an increase in the automatic withdrawal of more than $10 from the previous withdrawal amount.

· Revises provisions regarding the delivery of a policy to a policyholder by expanding the type of policies authorized to be delivered by electronic transmission to include individual and group health insurance policies, including dental.

· Revises the mandated deductibles that must be offered for hurricane loss when issuing a personal lines residential property insurance policy. For policies with a dwelling limit of at least $1 million, the bill no longer requires the offer of the current mandated deductibles of 2 percent, 5 percent, and ten percent of the dwelling limit. Instead, the bill provides that an insurer may offer deductibles of up to:

Ten percent, for a policy covering a risk with dwelling limits of at least $1 million, but less than $3 million;

Fifteen percent, for a policy covering a risk with dwelling limits greater than $3 million.

· Revises the requirement that the waiver by a policyholder of windstorm coverage or contents coverage, must be in the policy holder’s own handwriting, by also allowing the waiver to be typed.

· Eliminates the requirement that a notice be stamped on the declarations page of limited coverage automobile policies. Such policies generally cover antique motor vehicles.

4. Hurricane Protection for Condominium Association (Mitigation Credits)

HB 395/SB 556 By Rep. Tuck and Sen. Hooper

Both House and Senate bills have received three committee references. The Senate bill has cleared its first of three committee by a vote of 9-0 and is on the agenda in its second committee, Community Affairs, on March 29. The House bill has not moved and will have to clear two subcommittees in back to back weeks or its procedurally dead.

Adds in the definition section of condominium a term “hurricane protection” which covers hurricane shutters, impact glass, code-compliant windows or doors and other code-compliant hurricane protection products in order to potentially earn insurance mitigation credits.

The bill allows for condominium associations to let members vote and by a simple majority require unit owners to install hurricane protection that complies with or exceeds the applicable building code.

The House and Senate bills have received three committee references and should move through the process minus any objections from the engineers regarding vagueness of the term.

The bill adds “wind uplift prevention” to a list of techniques that can be used to reduce property loss and potentially receive a discount, credit or other rate differentials on property insurance.

HB 799 has passed its first of three committees, while SB 594 passed its first of three committees and is on the agenda in the Senate Community Affairs committee on March 29.

6. Flood Zone Disclosures for Dwelling Units HB 1291/SB 716

By Rep. Antone and Sen. Stewart

Both the House and Senate versions have received three committees of reference. Neither of these bills has been heard in committee.

Requires landlords or persons authorized to enter into rental agreements on behalf of landlords to make specified disclosures relating to flood zones before the commencement of a tenancy and reinform tenant if the flood zone changes.

The bill has three references in the House and Senate. The Senate bill will be heard in its second committee on March 27. The House bill still has not been heard in a committee.

The bill creates the “Flood Damage Prevention Act of 2023.” The bill seeks to allow the Florida Building Commission to develop certain mitigation strategies in rule to mitigate property damage and encourage continued investment in Florida.

8. Resolution of Disputed Property Insurance Claims HB 1141/SB 1174

By Rep. Gottlieb and Sen. Polsky

The bills received three references each in the House and Senate. The bills have not been heard and with the current climate in both House and Senate, I would expect this bill not to pass.

The bill creates mandatory mediation for resolution of disputed property insurance claims. If agreed to by both parties, it allows for mediation to be conducted via telephone. Once mediation is invoked, the policyholder must, within 10 days, provide to the insurer any and all supporting documents and information that serve as the basis for the claim.

AUTO

1. Motor Vehicle Liability Policies – HB 57/SB 516 for Risk Retention Groups

Truenow/DiCeglie

The House version only received two committee stops and cleared House Insurance and Banking 15-0 and goes next to the Commerce committee. The Senate version was referred to three committees. On March 22nd the Senate version was passed as a committee substitute by the Banking & Insurance committee. The bill has 2 more stops in the Senate.

The bill permits the owner or operator of a motor vehicle to provide proof of financial responsibility by obtaining an insurance policy from a risk retention group that: 1) has an “A” or higher rating for financial strength, and “VIII” or higher for financial size by the A.M. Best Company, and 2) only provides commercial coverage to its members and shareholders. The bill would permit an RRG to directly provide commercial auto insurance at a lower price to its Florida members.

2. Motor Vehicle Insurance and Driver Licenses for Foster Youth SB 168

By Sen. Garcia (I)

The Senate version is moving quickly through the process and only has two committees to go. A House bill has not been filed. The only hold-up may be the fiscal impact associated with the expansion of the program.

Expands the “Keys to Independence” program by removing language in statute that restricts one of the eligibility paths to receive Keys support. Currently, youth and young adults who achieve eligibility for the Keys program via enrollment in postsecondary educational services and supports (PESS) must also have been in licensed care when he or she reached 18 years of age. The bill expands eligibility for the Keys program by removing the requirement for young adults who are eligible by enrollment in PESS to also have been in licensed care when turning 18 years of age.

The Keys program is a state-funded normalcy support program designed to remove barriers to obtaining a driver license for foster and former foster youth. The program removes barriers to obtaining a driver license by young adults by paying, subject to available funding, the cost of driver education, licensure, other costs incidental to licensure, and motor vehicle insurance for certain populations. The change will allow approximately an additional 450 young adults to be eligible to participate in the Keys program.

3. Electronic Motor Vehicle Registration Certificates SB 370

By Sen. Brodeur

The Senate version has moved through the second of three committee stops. A House version has yet to be filed.

Authorizes acceptance of an electronic certificate of motor vehicle registration as documentation required to be in the possession of a motor vehicle’s operator or carried in the vehicle while the vehicle is being operated on the roads of this state. The bill provides that displaying an electronic registration certificate does not constitute consent for an officer or agent to access any other information on the electronic device, and the person who presents the device assumes liability for any resulting damage to the device.

4. Motor Vehicle Insurance HB 429/SB 586

By Rep. Alvarez and Sen. Grall

This is the PIP repeal bill for the 2023 Legislative Session. It has been filed by members of the legislature who are plaintiffs’ attorneys. The bill repeals Florida’s Motor Vehicle No-Fault Law and replaces it with a bodily injury liability system. In talks with leadership in the House, they have told us that PIP repeal is off the table or this session.

5. Commercial Vehicle Insurance SB 434

By Sen. Wright

The Senate bill has received three committees of reference and no House bill has been filed. We don’t expect this bill to be heard.

The bill increases the liability coverage from $350,000 per occurrence to $700,000 per occurrence for commercial motor vehicles with a gross weight over 44,000 pounds.

6. Towing Vehicles SB 438

By Sen. Rodriguez

The Senate bill has received three references and a House bill has yet to be filed. The bill has not been heard.

This bill seeks to make tow operators whole when towing vehicles from a scene to an investigating agency’s storage facility by mandating that the agency collects the towing and storage cost from the owner of the vehicle before the agency releases the vehicle and if they fail to do so the agency must pay that amount to the tow operator within 5 days.

7. Post-lost Benefit Assignments Under Motor Vehicle Insurance Policies HB 541/SB1002

By Rep. Griffitts and Sen. Stewart

This tort bill has received three committee references in the House. HB 541 was added to the Civil Justice Subcommittee agenda and will be heard on March 27. Its Senate companion received a favorable vote on the 20th of March in the Commerce and Tourism Committee and only must clear Senate Rules before it heads to the floor.

This bill eliminates auto “assignment agreements” for any policy issued after July 1, 2023. This is another anti-trial bar bill designed to stop excessive litigation on auto insurance policies.

GENERAL INSURANCE

1. Department of Financial Services HB 487/SB 1158

By Rep. Salzman and Sen. DiCeglie

The House version of this bill passed its first of three committees on March 21. The Senate version passed its first of three committees Banking and Insurance on March 22. The House staff director removed several sections of the bill claiming they were not germane to the title of the bill.

This is an omnibus department package and includes the following:

· Workers compensation – changes jurisdiction of the three-member panel and reimbursement schedule;

· Guaranty funds: Makes changes to the board composition of FSIGA, FIGA, FLAHIGA and Medical Malpractice JUA. Allows CFO to remove a director for malfeasance.

· Changes fingerprint requirements for agent licensing exam centers;

· Exempts title, life insurance and annuity contracts from agency closure notification provisions.

· Agent examination is not required for Professional in Claims (PIC) from 2021 Training, LLC;

· Specifies elective continuing education courses for public adjusters may must be any course related to commercial and residential property coverages, claim adjusting practices, and any other adjuster elective courses;

· Strikes prohibitions on agents holding limited lines licenses for credit insurance for sales of motor vehicle physical damage and physical breakdown insurance, and combinations of other lines as well;

· Contains various public adjuster licensing updates;

· Revokes health insurance Navigator licenses where they fail to maintain a valid federal navigator registration;

· For property, casualty, except mortgage guaranty, surety, or marine insurance, other than motor vehicle insurance subject to s. 627.728 or s. 627.7281, reduces the period from 90 days to 60 days when such cancellation or termination occurs during the first 60 days during which the insurance is in force and the insurance is canceled or terminated for reasons other than nonpayment of premium, then at least 20 days’ written notice of cancellation or termination must be given accompanied by the reason why;

· Corrects a glitch for HB701 (2021 session) for Behavioral Health notification and disclosure requirements; (removed from the House version; remains in Senate version)

· Prohibits a liability insurer is prohibited from denying coverage for property and bodily injury liability claims made against an insured for up to the property and bodily injury liability limits set in s. 324.021(9) solely based on the insured’s failure to cooperate with the insurer’s investigation — unless the insurer can clearly demonstrate by a preponderance of the evidence that the insured’s lack of cooperation has resulted in actual prejudice to the insurer;

· Alternative Dispute Resolution: Would require an insurer is to make a claim determination or elect to repair pursuant to s. 627.70131 before participating in mediation.

· Imposes new restrictions against Collateral Protection insurance on a mortgaged property;

· Mediation of Claims: Increases the jurisdictional amount from $10,000 per claim to $50,000 per claim for personal injury or property damage claims related to a motor vehicle; insurers must bear all costs of the mediation, which must be reasonable; allows DFS to adopt rules for the program;

· FIGA: allows sharing of the insolvent insurers records with the prospective solvent assuming insurer for purposes of due diligence and allows transfer of the insolvent insurers book of business and policies; allows adjustment of cancellation date of policies by the receiver;

· Establishes a Direct Support Organization for the State Fire Marshal;

· Service Warranties: allows DFS to issue salesperson license for motor vehicle service agreement companies and insurers to nonresident applicant where there is reciprocity with the applicant’s home state; licensees charged with a felony may be immediately suspended; licenses must report actions against their license within 30 days of final administrative action;

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Florida authorities on Friday charged a man with unlicensed contracting, insurance fraud and failing to obtain workers’ compensation coverage on his workers, after he solicited Tampa-area homeowners for roof replacement work.

John Sutton, doing business as Kaizen Construction Group, had salesmen go door to door in Pasco County in 2021 and 2022, instructing homeowners on what to say in filing an insurance claim, Florida’s chief financial officer said in a bulletin. Some of the homeowners agreed to sign “direct to pay” documents, essentially assigning benefits to the roofing company.

Investigators from the Department of Financial Services and the Pasco County Sheriff’s Office determined that Sutton and Kaizen Construction were unlicensed as roofers and were responsible for more than $41,000 in insurance claims. Sutton later reportedly made a statement saying that he has victimized hundreds of homeowners throughout the state, the DFS said.

Florida Department of State records show Kaizen Construction in Thonotosassa, Florida, was registered as a limited liability company with Sutton listed as manager, until it was dissolved in 2021.

If convicted of the charges, Sutton could face up to 25 years in prison. People who know of homeowners that may have been subject to the company’s solicitations are urged to call the CFO’s fraud hotline at 800-378-0445.

DeSantis says the state’s insurance regulation office is investigating reports of people being shortchanged or unlawfully dropped following the filing of their claims.

By Lisa Willis |

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Three months after allegations surfaced in Tallahassee concerning South Florida insurance carriers altering insurance adjusters’ reports, Florida’s home insurance crisis is now at the center of a state investigation.

Gov. Ron DeSantis announced the probes.

In Fort Myers last Friday, the governor was asked at a press conference for an update on comments made in front of the chairman of the House Commerce Committee in December.

DeSantis’ reply: “The reports of people getting shortchanged or getting unlawfully dropped because someone was looking to make more money, the insurance regulation office is investigating that. … They need to be held accountable, and I know they will be aggressively doing it.”

Florida Chief Financial Officer Jimmy Patronis confirmed criminal investigations are now underway.

When contacted by ALM’s Daily Business Review, his office said, “The Department’s Division of Investigative and Forensic Services opened an investigation into these fraud allegations.”

“That investigation is currently open and ongoing,” said Devin Galetta, communications director for the state’s CFO. “No further details are available at this time.”

Adjusters weigh in

Boca Raton public adjuster and insurance appraiser Karen R. Schiffmiller is not surprised.

“This happened to an elderly client of mine, and sadly, her insurance company went under in the process while we were trying to settle her claim,” Schiffmiller said. ”We were trying to go back-and-forth and get the coverages put back in, and they kept asking for additional inspections — delaying — then they went out of business.”

Schiffmiller co-owns Reliant Insurance Adjusters, and is past president of the Florida Association of Public Insurance Adjusters.

She said this happened to multiple clients of hers where the adjusters inspect the damages, and “by the time they submit their report to the insurance company, it gets changed once it gets back to us. And it happens more often than not, and I believe the carriers or the management at the insurance company are making those decisions.

“I’m standing there fighting for everything that they should be covered for, and I know it’s covered, I’ve reviewed their policy and I find that the management of the carriers are not following through … the field adjusters agree to the damages,” Schiffmiller added. “We discuss it. We have an agreement before we walk away for the property in the sense of what’s damaged, and then when you get the estimate, it’s something completely different.

“I don’t see how that could not be construed [as fraud], because I think that’s pretty fraudulent,” Schiffmiller claimed.

A Florida licensed independent adjuster mentioned the alleged “scheme” to the committee in December, alleging fraud on reports filed after homeowner visits in Southwest Florida, post-Hurricane Ian.

Attorneys divided

Jack Hickey of Hickey Law Firm in Miami said this is exactly why we need laws with “teeth” to enforce the concept of operating in good faith.

“We need the bad-faith laws to keep the insurance companies in check, and to make sure they don’t continue fraud like this,” he claimed.

Hickey said that if the Legislature is successful in taking away attorney fees, for example, when a policyholder sues its insurance company, that will lead to further problems in claim denials.

“What all these laws add up to is the fact that the insurance companies get a big giveaway by our state,” he said. “Insurance companies have freedom, but the policyholders and the 28 million citizens of the state of Florida do not have the freedom to get their insurance claims paid.”

But other lawyers have different views on the issue, which they say will create more problems.

“I anticipate that there will be more litigation, despite the Legislature’s efforts to curb it,” said Stephen A. Marino Jr. of Ver Ploeg & Marino in Miami.

“Curbing litigation, making it harder to get to the courthouse doors doesn’t mean that the need to get to the courthouse doors goes away,” Marino continued. “It’s unfortunate that the Legislature found reasons to make the steps to the courthouse doors harder to climb. But that doesn’t mean that the need to climb those stairs is missing.”

Patronis’ office said the state’s CFO is taking this matter seriously.

“Anyone who suspects fraud should report it immediately to our Insurance Fraud Hotline at 1-800-378-0445,” the office said.

Two months after Allstate announced that a Florida subsidiary would non-renew 33,000 condominium policies, the company has filed for a 53.5% average rate increase.

Castle Key Indemnity Co., which as of year-end 2022 held some 287,000 policies in Florida, making it one of the largest property-casualty carriers in the state, this week asked the Florida Office of Insurance Regulation for the rate change on its remaining condo policies.

“This change will be accomplished by revising the non-hurricane and hurricane base rates, as well as the non-hurricane and hurricane coverage A rates,” reads the filing with OIR. “For the base premium and coverage A premium calculation, Castle Key is proposing changes to the non-hurricane and hurricane territorial relativities rating plans.”

The company cited hurricane models for Florida and reinsurance costs in its explanatory memo. The use-and-file increase took effect March 14, but OIR can later review the action and approve or reject it.

Castle Key Indemnity is officially closed to new business, company consultant Jennifer Olson said in the filing. The carrier insures condo units and does not write master condo policies. Policies in force at end of last year included condominium, homeowner and tenant policies, according to OIR’s latest quarterly report, released Friday. Direct written premium was almost $371 million.

The filing is the latest bleak financial news about Allstate’s Florida companies, which were created in 2009, and about Florida’s property insurance market, despite recent efforts by Florida lawmakers to reduce litigation costs for carriers. The AM Best rating firm earlier his month said that it had given the Castle Key Group of companies a “B+ good” financial strength rating, but had lowered the long-term credit rating to “bbb-, with negative implications.”

The lowered credit rating was the result of Castle Key’s “material deterioration in its surplus position as a result of challenging personal property insurance conditions in Florida,” including soaring reinsurance costs, AM Best said in a bulletin.

Castle Key Insurance Co., with about 40,000 policies in Florida, provides the reinsurance for Castle Key Indemnity. An industry analyst said that the rating firm probably wanted to see Allstate shore up the surplus levels at Castle Key Insurance.

It’s also another blow for Florida condo unit owners, many of whom have been hit with non-renewals and premium spikes after the collapse of the Champlain Towers South condominium building in Miami Beach in 2021, which killed 98 residents. Unit owners who have switched to Citizens Property Insurance Corp., the state-created insurer, also face higher premiums and a new statutory requirement to purchase flood insurance.

Two months after Allstate announced that a Florida subsidiary would non-renew 33,000 condominium policies, the company has filed for a 53.5% average rate increase.

Castle Key Indemnity Co., which as of year-end 2022 held some 287,000 policies in Florida, making it one of the largest property-casualty carriers in the state, this week asked the Florida Office of Insurance Regulation for the rate change on its remaining condo policies.

“This change will be accomplished by revising the non-hurricane and hurricane base rates, as well as the non-hurricane and hurricane coverage A rates,” reads the filing with OIR. “For the base premium and coverage A premium calculation, Castle Key is proposing changes to the non-hurricane and hurricane territorial relativities rating plans.”

The company cited hurricane models for Florida and reinsurance costs in its explanatory memo. The use-and-file increase took effect March 14, but OIR can later review the action and approve or reject it.

Castle Key Indemnity is officially closed to new business, company consultant Jennifer Olson said in the filing. The carrier insures condo units and does not write master condo policies. Policies in force at end of last year included condominium, homeowner and tenant policies, according to OIR’s latest quarterly report, released Friday. Direct written premium was almost $371 million.

The filing is the latest bleak financial news about Allstate’s Florida companies, which were created in 2009, and about Florida’s property insurance market, despite recent efforts by Florida lawmakers to reduce litigation costs for carriers. The AM Best rating firm earlier his month said that it had given the Castle Key Group of companies a “B+ good” financial strength rating, but had lowered the long-term credit rating to “bbb-, with negative implications.”

The lowered credit rating was the result of Castle Key’s “material deterioration in its surplus position as a result of challenging personal property insurance conditions in Florida,” including soaring reinsurance costs, AM Best said in a bulletin.

Castle Key Insurance Co., with about 40,000 policies in Florida, provides the reinsurance for Castle Key Indemnity. An industry analyst said that the rating firm probably wanted to see Allstate shore up the surplus levels at Castle Key Insurance.

It’s also another blow for Florida condo unit owners, many of whom have been hit with non-renewals and premium spikes after the collapse of the Champlain Towers South condominium building in Miami Beach in 2021, which killed 98 residents. Unit owners who have switched to Citizens Property Insurance Corp., the state-created insurer, also face higher premiums and a new statutory requirement to purchase flood insurance.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

More than 18 months after he pleaded guilty to absconding with almost $5 million in premiums, a Florida insurance agent has been sentenced to 14 years in prison.

John M. Thomas, 52, the former owner of Thomas Insurance agency in Pensacola, also must pay more than $8 million in restitution, a federal judge decided this week.

“This sentence should serve as a significant deterrent to those who would defraud our citizens, in this case depriving them of critical insurance coverage, simply to unlawfully enrich themselves,” U.S. Attorney Jason Coody said in a statement.

For more than seven years, Thomas collected premium payments from at least 67 clients, then produced fraudulent policy documents and certificates purporting to show that clients were covered. Thomas used the money for personal gain, including an African safari, a Utah ski resort condominium, a Florida beach condo, a Lexus automobile and restorations to a 45-year-old Jeep vehicle, according to his 2021 indictment.

The independent agency sold homeowners, commercial property, commercial liability, auto, workers’ compensation and other lines of insurance to some well-known commercial interests in Florida and Alabama before the fraud was discovered, attorneys said.

“It appears that he was well connected with the country club set, some of whom he was taking money from,” said Craig Rettig in 2021.

Rettig is a Pensacola plaintiffs’ attorney who filed suit against Thomas on behalf of some commercial property owners who said they were defrauded. “You don’t see many insurance agents with resort condominiums and luxury cars and restored Jeeps like that.”

By failing to secure actual insurance policies, some clients lost more than $2 million in unpaid hurricane, fire and liability claims, federal prosecutors said.

After the allegations came to light in 2021, more than 15 former clients filed complaints or lawsuits against Thomas. Pensacola Beach Properties Inc. suffered damage to multiple buildings when Hurricane Sally hit the Pensacola area.

“When plaintiff began making contact with the insurance companies believed to have been providing coverage, she was informed that defendant had failed to forward payment to the insurance companies,” the lawsuit complaint noted.

That suit explained that questions also arose when a major apartment complex in Mobile, Alabama, was damaged in a fire in May 2020. The Texas-based owners contacted the insurance carrier, only to be told that Thomas had never taken out a policy on the apartments.

Thomas said there was a “mix-up” and paid $500,000 from a personal account as a downpayment on the claim, Rettig said. A second check from Thomas’ bank account bounced, and that’s when the property owners decided to take legal action.

In another suit, a New York couple that owned a home near the beach charged that their house sustained wind and flood damage in the storm. Thomas told them he had filed the wind claim and promised to send the couple the documentation and policy. He never did, the complaint notes.

Thomas was arrested then unexpectedly pleaded guilty to the criminal charges in August of 2021. His sentencing was set for later that year. Prosecutors did not say why the sentencing had to wait for another 18 months, but court records suggest that Thomas’ pro se filings with the court may have delayed the proceedings.

In August 2022, while incarcerated, he hand-wrote a motion asking to terminate his attorney from the case. “Defendants retained counsel has consistency (sic) demonstrated material neglect with regard to … communicating with the defendant” and providing sound legal advice, the motion reads.

It’s unclear if the motions helped or hurt Thomas’ sentencing, but the length of the prison time and amount of restitution is near the maximum recommended by federal sentencing guidelines.

“Today’s sentencing should serve as a warning to anyone who uses illegal means and criminal behavior to take advantage of others,” said Sherri Onks, special agent in charge of the FBI’s Jacksonville Division. “The victims in this case suffered significant loss and pain as a result of this deception, never knowing they were without insurance coverage until disaster struck.”

The prosecution resulted from a joint investigation by the FBI and the Florida Department of Financial Services’ fraud bureau, prosecutors said.

U.S. District Judge Casey Rodgers recommended that Thomas serve his time in federal prison in Tucson, Arizona or San Diego. After prison, he’ll face three years of supervised release.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

The Florida Senate is set to approve a take-no-prisoners tort-reform bill today and it could be signed into law as soon as Friday.

The bill, which extends limits on one-way attorney fees, assignments of benefits, and other provisions to most types of insurance claims, would take effect as soon as the ink is dry on the governor’s signature.

And that won’t be a minute too soon, as plaintiffs lawyers have moved to file tens of thousands of claims lawsuits before the new restrictions kick in, insurance industry advocates said Thursday.

An email from Cole, Scott & Kissane, one of Florida’s largest insurance defense law firms, was sent to the firm’s lawyers and has been forwarded around the state. It relates a phone conversation with Matt Morgan, partner with Morgan & Morgan, one of the country’s largest plaintiffs’ firms. Morgan said that the Orlando-based firm will have filed 25,000 insurance-claim cases by this week.

“The defendants won’t initially be served but the carriers will be sent a letter demanding the policy limits,” reads the email from Richard Cole, managing partner with Cole, Scott & Kissane.

Insurance carriers will have five days to respond. If the policy limits are not tendered, full litigation will follow, Morgan said.

“The call was cordial but direct,” Cole noted in the email. “Feel free to let your client carriers know of Morgan and Morgan’s position and plans.”

John Morgan (Joe Burbank/Orlando Sentinel via AP)

John Morgan, head of the firm, said Thursday in a statement to Insurance Journal: “At this moment we are doing what all lawyers should be doing – protecting the interests of our clients.”

He added: “There is no insurance crisis in Florida. Rates won’t go down. They never have and never will. All tort reform this year should be titled ‘F*** the People.’”

Cole, reached by phone Thursday, said other plaintiffs’ firms will likely take similar actions and the state could see as many as 100,000 suits filed by today.

Insurance groups agreed, noting that the flood of litigation gives urgency to the governor to sign House Bill 837 as soon as possible.

“I expect to see a tidal wave of suits filed by today, frankly,” said Michael Carlson, president of the Personal Insurance Federation of Florida, which includes some of the largest property insurers in the state. “The trial bar knows that the governor could sign the bill by today, so they’re trying to get these in before then.”

He noted that an excessive number of lawsuits is exactly what HB 837 is designed to prevent going forward. Until the law has an impact, though, insurance carriers and county clerks of court will likely be swamped with work, Carlson and Cole predicted.

“It will put a lot of stress on the whole system,” Cole said.

“Giving five days to respond, and no settlement for less than the policy limits – that’s just ridiculous,” Carlson added.

Others in the industry joined in the criticism of the claimants’ lawyers’ legal efforts.

“This is the exact reason the state of Florida needs this tort reform bill. These opportunistic lawyers are acting in bad faith by sprinting to file 25,000 cases ahead of the law’s passage,” Neil Alldredge, president and CEOof the National Association of Mutual Insurance Companies, said in an email. “This last-ditch stunt is yet another example of how legal system abuse has added to the challenges of providing insurance coverage in the state and increased costs for consumers.”

HB 837 passed the full House last week and was set for a third reading in the Senate Thursday afternoon. It has survived largely intact since it was introduced by Sen. Tommy Gregory, R-Lakewood Branch.

Democratic senators on Wednesday attempted a last-minute rewrite to soften the impact on policyholders and their attorneys. That amendment failed to pass on the Senate floor.

An explanation of the bill’s provisions can be seen here.

")