Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

How will the insurance bills that passed in the recently completed 2024 Florida legislative session compliment past marketplace reforms? Is a property insurance market marred by carrier insolvencies in recent years and ongoing double-digit rate increases starting to stabilize?

Former Florida Deputy Insurance Commissioner Lisa Miller talks with two legislators about the new laws expected to impact Florida’s property insurance and real estate markets, reinsurance prices, condominium affordability, and their joint belief in bipartisanship for finding workable policy solutions.

Florida State Representative Tom Fabricio (R-Miami Lakes)

Florida State Senator Nick DiCeglie (R-St. Petersburg)

Show Notes

Florida State Representative Tom Fabricio (R-Miami Lakes) sits on the House Insurance & Banking Subcommittee and Chairs the House Ethics, Elections & Open Government Subcommittee. He is a former insurance defense attorney whose practice now focuses on commercial and real estate litigation, including real estate transactions.

Florida State Senator Nick DiCeglie (R-St. Petersburg) is Vice Chair of the Senate Banking and Insurance Committee, Chair of the Senate Transportation Committee, and a former Chair of the House Insurance & Banking Subcommittee. He is President and CEO of Hope Villages of America, a Tampa Bay area nonprofit organization addressing hunger, homelessness, and domestic violence.

Both lawmakers discussed their motivation for entering the Florida Legislature and their vision for Florida’s homeowners insurance marketplace and by extension, the state economy. Topics included the admitted insurance market (those companies whose rates and policy forms are approved by state regulators) and the surplus lines companies (those whose rates and forms are largely unregulated, and who often insure risks admitted companies don’t), along with reinsurance companies, who provide catastrophe insurance for insurance companies. Among the bills and issues discussed on the podcast with host Lisa Miller:

HB 1503 authorizes surplus lines insurance companies to take out policies (“takeouts”) from the legislatively-created and state-backed Citizens Property Insurance Corporation’s non-homesteaded residential properties, such as second homes, among other risks. “I think surplus lines are important (for) it allows other free market competition,” said Rep. Fabricio. “Because ultimately, with Citizens having a population of over 1.2 million to close to 1.3 million policies, we need to depopulate Citizens. We need to bring Citizens down to a number under a million policies, where Citizens will be truly our carrier of last resort,” he said. HB 1029 applies the popular My Safe Florida Home homeowners program to condominium complexes and individual condo unit owners in an initial pilot program. The program offers a $2 to $1 match to incentivize homeowners to harden their homes from future hurricanes. “Anytime that we can mitigate losses in the state, it’s going to go a long way in contributing to that healthy insurance market,” said Sen. DiCeglie, who sponsored the Senate companion bill. “In my district alone, we have thousands of condominium associations and those folks are looking for relief as well. Recent condominium reforms requiring them to put more money in reserves, so that they’re making the necessary repairs and upkeep of the condominiums (together with) the same increases in insurance, they’re getting hit on both sides,” he said. Reinsurance, with rate increases of 20% to 40% over each of the past three years onto insurance companies that in turn, pass the cost along in premiums to homeowners, “has been difficult for us to specifically address from the Florida Legislature’s perspective,” said Rep. Fabricio. “Part of the reason is that we don’t want to tinker with the market too much. We’ve been seeing some very positive effects of our past legislative reforms…and I think and am hopeful that the reinsurance carriers see that there was benefit for them, helping us fill our reinsurance towers in the last hurricane cycle. Coming forward this year, we’re hoping that their appetite, their pricing will be commensurate with the reduced risk that we’ve brought into Florida by balancing the markets,” he said. HB 1021 overhauls current statutes to impose criminal penalties for violations and fraud on condominium boards, other community and homeowner associations, and their elections. The bill outlines new education requirements for condo managers, requires building records to be available online, and clarifies obligations surrounding hurricane protection. It follows the collapse of the Champlain Towers South condominium high-rise, a tragedy which claimed the lives of 98 condo residents in Surfside, Florida in June of 2021, which since has highlighted the shortcomings in state law, infrastructure, and governance. Host Miller noted the current trend of condo sell-offs, as unit owners have been pushed to lower their selling price as insurance and homeowner association fees have increased. “There’s no sense in sugarcoating this,” replied Sen. DiCeglie. “Many of these folks are retirees, they’re on fixed incomes, and they’re having a really, really difficult time making these assessments that they’re getting. It’s translating into higher monthly costs for them and they are very concerned whether or not they can they can afford to live in these condominiums. So anytime you hear that we’re in that situation, certainly the banks and rightfully so, should be concerned about potential foreclosures and things like that. It’s really that perfect storm,” said Sen. DiCeglie.

Host Miller also asked Representative Fabricio and Senator DiCeglie about a topic that she knows from years observing them in the legislature is one that both are passionate about: the ability to work across the aisle, with Democrats, in a true bipartisan way.

“I would say that approximately 90% of the legislation that’s passed in the House and I suspect in the Senate as well, is bipartisan for the most part,” said Rep. Fabricio. “While there are disagreements within those 90%, they’re not always necessarily partisan disagreements. They’re just disagreements over policy, as we should have in the legislature. We’re working together to figure out what’s the best policy for Florida,” he said of the 120-member body.

Senator DiCeglie agreed with the 90% figure. “It’s about relationships. In the Senate, we’re 40 members and so we spend a lot of time together, in committee and on the floor,” said Sen. DiCeglie, noting both Republicans and Democrats build relationships with one another, sharing stories about family and their professional lives. “I go out of my way to make sure with the legislation I’m working on, that I get it right. I want to know what those potential unintended consequences are and the only way to do that is to get the feedback not only from Republicans, but you have to get that from Democrats as well. We’re all duly elected, we all represent the same number of people. I think that’s really what makes this legislature work so well, is that we have these relationships. We work behind the scenes with each other,” he said.

Both legislators said property insurance rates will be the number one issue in state elections this fall.

Links and Resources Mentioned in this Episode

Florida Legislature Bill Watch – final 2024 edition (Lisa Miller & Associates)

HB 1503 “Citizens Property Insurance Corporation”

HB 1029 “My Safe Florida Condominium Pilot Program”

The Path to Homeowners Rate Relief Now (Lisa’s Blog, January 1, 2024)

HB 1021 “Community Associations”

Closing 2024 Budget Discussion in the Florida House of Representatives (The Florida Channel, March 8, 2024)

LMA Newsletter of March 11, 2024 (Lisa Miller & Associates)

Subscribe to the LMA Newsletter (free)

** The Listener Call-In Line for your recorded questions and comments to air in future episodes is 850-388-8002 or you may send email to LisaMiller@LisaMillerAssociates.com **

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

Author: Céline McArthur Published: March 15, 2024 Updated: March 15, 2024

With property insurance costs skyrocketing and coverage dwindling, you may wonder if it’s worth the money.

if you have a mortgage, you must have insurance, but more Floridians who own their homes opt to go without it.

WINK News investigative reporter Celine McArthur explores this trend to show you what impact it can have across Florida.

Block parties happen often on Miramar Street in Fort Myers Beach.

“We have a text chain of people on the street,” said Don Hunter. “I think there’s 17 folks on there and everybody’s invited, and there would be 17 responses,” said Don Hunter.

Don and his wife Leslie Hunter repurchased their bungalow in 2005.

Céline inquired, “What made you come down here?” Don chuckled in response, “The weather.”

Leslie shared, “The first time we came across that bridge, that was it. We saw the town and fell in love with it.”

The Hunters held property insurance for years but dropped it in 2018 as premiums skyrocketed.

“It got to the point where we thought, you know, if nothing happens for five years, we would break even. I mean, it was well over $12,000 a year,” Don explained.

After getting slammed by Hurricane Ian four years later, the Hunters admit dumping their insurance might not have been the best call.

Fortunately, the Hunters could dip into their savings to lift their bungalow and fix the damage, which will cost about $200,000. Once it’s done, they plan to pay for some insurance.

Don noted, “We’ll probably have wind insurance, but not flood.”

Mark Friedlander with the Insurance Information Institute, a trade association funded by insurance companies, warns the Hunters took a risk that would devastate most homeowners.

“It’s good to hear that certainly, it worked out very positively for that homeowner,” said Friedlander. “You may have saved funds for 20 years or so. That’s fabulous. But now, what if you get another storm in the next year or two? You don’t have 20 years to save. It’s just not a realistic picture.”

This sentiment is underscored by a new Bankrate survey, revealing that 56% of American adults lack the emergency funds to pay for a one-thousand-dollar expense.

Friedlander questioned, “How could they possibly think they could pay for a catastrophic loss of their home out of pocket?”

Stefan Contorno, Senior Vice President and Partner at Touchstone Wealth Partners UBS emphasizes the importance of asking yourself a critical question if you’re considering canceling your policy: “Should you be living in a home to begin with, right? If it is too expensive, you might want to rethink your situation.”

Public Adjuster Rod Buvens has worked in the insurance industry for decades and explains how the growing number of uninsured homeowners will impact the Florida market.

According to Buvens, “Even a 5% or a 10% movement is catastrophic for the market because we are in a pool together. We’re all grouped in, and the folks that pay higher premiums, generally the people that don’t have mortgages on their property, they’re all kind of subsidizing the people that have mortgages.”

Elaine and Michael Damiano’s home was badly damaged by Hurricane Ian 17 months ago, and their insurance claim remains unresolved.

“We’re still fighting,” Elaine declared. “We haven’t given up, and we’re not going to give up. We’re not going away.”

Despite their ongoing nightmare, the Damianos say they won’t give up their insurance coverage.

Elaine reflected on their situation, stating, “For what happened to our house in the 10 years, you would have to be able to save almost $400,000 to put the house back together…” Michael interjected, expressing his determination, “I’d rather fight them…” Elaine responded firmly, “No, you have to have insurance…” Michael concluded confidently, “and win.” Emphasizing his stance, Michael stated, “I believe in insurance for everything that’s insurable.”

Insurance experts recommend that if you’re looking to trim expenses while maintaining your coverage, you should contemplate opting for a higher deductible. While it means more money out of pocket initially, it can prove to be less costly in the long run compared to bearing the full financial burden on your own.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

Accuweather meteorologists are predicting an above-average Atlantic hurricane season with as many as 20-25 named storms.

The 2024 hurricane season is forecast to feature 8-12 hurricanes including 4-7 major hurricanes.

This year has the potential to break the all-time record of 30 named storms in one season, Accuweather experts say. Texas, Florida Panhandle, South Florida & Carolinas face heightened risk of named storms.

“All indications are pointing toward a very active and potentially explosive Atlantic hurricane season in 2024,” said Accuweather lead hurricane forecaster Alex DeSilva. “There is a 10 to 15 percent chance of 30 or more named storms this year. Surpassing 30 would break the record set in 2020.”

Forecasters at Accuweather call for a dramatic shift from the 2023 hurricane season in which there were 19 named storms but only four storms that directly impacted the United States.

Accuweather experts say the potential for destructive hurricanes is driven by above-average sea-surface temperatures across much of the Atlantic basin, especially across the Gulf of Mexico, Caribbean, and the Main Development Region.

Atlantic water temperatures in March were just as warm or warmer as March 2005 and March 2020, years that saw catastrophic hurricane impacts in the US.

The 2020 hurricane season broke records with 11 different landfalls in the US, causing an estimated $60 billion to $65 billion dollars in damage and economic losses, Accuweather data shows.

Unusually warm sea temperatures could also support tropical systems forming before the start of the official hurricane season on June 1, according to Accuweather experts.

“When you look back at historical sea surface temperature in the Atlantic’s Main Development Region, recent average water temperatures jump off the chart. They are the highest observed this early in the season in the available records,” said Accuweather chief meteorologist Jon Porter. “This is a very concerning development considering this part of the Atlantic Ocean is where more than 80 percent of the storms form which go on to become tropical storms or hurricanes.”

Other factors Accuweather points to that could contribute to a volatile hurricane season include the shift from an El Niño pattern to a La Niña pattern, a stronger African jet stream that could lead to more robust tropical waves to form later in the season, and changes in location and strength of steering winds.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

A board appointed by Ron DeSantis to oversee the municipal authority that governs Walt Disney Co. in Florida has voted to settle a state lawsuit against the company.

The board of the Central Florida Tourism Oversight District unanimously approved a settlement offer made by Disney in a meeting Wednesday, putting an end to almost year-long legal battle between the Florida Governor and one of the state’s biggest employers.

Under the settlement, Disney will agree to revoke some of the changes that limited the powers of the municipal authority and were quietly approved before the DeSantis-appointed board took over. The changes had restricted the powers of the new board members, including their ability to review theme-park expansions and billboard advertising.

“We are pleased to put an end to all litigation pending in state court in Florida between Disney and the Central Florida Tourism Oversight District,” Jeff Vahle, president of Walt Disney World Resort said in a statement. “This agreement opens a new chapter of constructive engagement with the new leadership of the district and serves the interests of all parties by enabling significant continued investment and the creation of thousands of direct and indirect jobs and economic opportunity in the state.”

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

For the first time in seven years, Florida’s property insurers turned a profit. Don’t get too optimistic, though: you can mostly just chalk their performance up to getting lucky during hurricane season.

Insuring homes in Florida has become a tough business. The state’s population has continued to rise in recent years, even as frequent and more devastating hurricanes cause billions in property damages: insurers’ underwriting losses cost them $1.8 billion in 2022, and $1.52 billion in 2021.

Last year, though, was a bright spot in what’s become a concerning downward trend, according to a new report from S&P Global Market Intelligence. In 2023, Florida’s property insurers turned a profit of almost $150 million, helped by a less-deadly hurricane season, strong returns on investment portfolios and new insurer-friendly laws.

“Florida is one of those feast or famine states when it comes to property insurance losses,” S&P Global Market Intelligence analyst Tim Zawacki told Fortune. “The wind blew the right way last year.”

Florida homeowners have been facing skyrocketing insurance costs in recent years, as increased hurricane risk and a shrinking pool of private insurers have pushed rates up. Citizens Property Insurance Corp., a taxpayer-owned “insurer of last resort” created in 2002, has picked up the slack. After posting meager gains in the early 2010s, Citizens and the remaining private insurers started losing money in 2017, and the three-year stretch between 2020 and 2022 cost them upward of $3 billion in losses. The market has suffered: nine residential property insurers went under or merged with their competitors between 2021 and 2023.

Related video: Florida insurers made money last year for first time in 7 years, report says (WPTV West Palm Beach, FL)

Loaded: 30.59%Pause

Current Time 0:00

/

Duration 1:57Quality SettingsCaptionsFullscreen

WPTV West Palm Beach, FL

Florida insurers made money last year for first time in 7 years, report saysUnmute

“Citizens is the public entity that, you know, the larger it gets, the more risk that is out there for all insurance customers in Florida, regardless of who their carrier is,” said Zawacki. Because Citizens is owned by taxpayers, taxpayers are ultimately on the hook for any losses Citizens incurs that exceed its reserves. “There has been encouragement by the state to bring in new private carriers.”

Last year’s positive returns are helping to do just that—reversing the trend in recent years, Florida regulators approved six new property insurers to start writing policies in 2024. The state also recently passed two insurer-friendly laws that will make it easier to operate in the state: one law helps disincentivize citizens from making frivolous insurance claims, and another helps prevent customers from assigning their insurance benefits to other people, such as contractors.

“The industry is on a much firmer footing today than it was prior to [the latter law] being passed,” Zawacki said. “If you look back in terms of what have been the drivers of higher losses in the Florida market, major hurricanes are obviously a big driver. But also, fallout from the litigated claims following a weather event has been a significant issue.”

The three largest counties in South Florida—Miami-Dade, Broward, and Palm Beach—are some of the state’s most densely populated, and are also some of the most vulnerable to hurricanes. Taxpayer-owned Citizens writes a much higher proportion of the policies in those three counties than any private insurer. Zawacki pointed out that diversity within the Florida market can create attractive opportunities for private insurers less willing to take risks.

“Florida’s a very large and diverse state in terms of geography and catastrophe risk. The Tri-County area down in South Florida is a very different area than, you know, say some of the areas on the Gulf Coast or up in the panhandle,” Zawacki said. “Companies can come in and maybe focus on specific attractive segments that may be lower risk.”

One year of positive returns doesn’t change the broader, worrying trends in Florida’s property insurance market. New legislation and tentative willingness from private insurers to step in are positive signs, but experts agree that the state is likely too heavily reliant on Citizens, and a healthy market requires that more private insurers pick up the slack across the state.

“The industry is in a much better place, but that doesn’t necessarily mean that it’s in a good place,” Zawacki said. “There needs to be more private investment in the market.”

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

Florida is not alone when it comes to property insurance. One in 13 homeowners across the U.S. are uninsured, according to a recent study by the Consumer Federation of America. Forgoing homeowner coverage, or going bare, is more of a thing than many elected officials want to believe.

“Going bare puts consumers at risk of accruing significant financial debt to repair their homes, having to live with unsafe and inadequate housing conditions, or moving from homeowner to homeless after disaster strikes,” the Consumer Federation’s study stresses.

America’s property coverage crisis is quickly turning into a calamity. It’s time for the insurance industry and those elected officials who have dithered with the problem to take some out-of-the-box ideas seriously.

The Florida Legislature had a chance during its most recent session. State Reps. Spencer Roach, R-Fort Myers and Hilary Cassell, D-Dania Beach, offered a bill requiring homeowners obtain coverage from Citizens Property Insurance instead of private insurance firms. Citizens, they said, would collect premiums and act like the National Flood Insurance Program, leaving the private insurers to cover fire, theft and other property damage.

Related video: Real estate settlement reached could lower some costs for home buyers, NE Florida realtor says (Action News Jax)

Those are two changes. Kelsey E Barb Rembold,

Loaded: 44.17%Play

Current Time 0:15

/

Duration 1:48Quality SettingsCaptionsFullscreen

Action News Jax

Real estate settlement reached could lower some costs for home buyers, NE Florida realtor saysUnmute

The idea didn’t get far. For years, state lawmakers have been content to follow the industry’s lead in blaming lawsuits and fraud and making it harder for consumers to sue insurers, as premiums soared. Of late, the state has implemented home-hardening programs and even a modest tax cut — baby steps at best.

The Federation study shows the precariousness of today’s insurance market and urges better data on access to coverage and on coverage gaps, to help our elected officials come up with better policies to help homeowners. The problem, a big concern here in Florida, is a national one and needs far more attention than it has received.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

Worst Is Over: Most of Casualty Reserve Hole May Be Filled, Analyst Says

Predictions that the property/casualty insurance industry is in the midst of repeating the type of loss reserving cycle that accompanied the hard market of the beginning year of this century may be overblown, according to an analyst.

In fact, William Wilt, president of Assured Research, believes that “much (but not all) of the financial hole the industry had dug for accident years 2016-2019 has now been filled.”

The industry analyst and Fellow of the Casualty Actuarial Society delivered the assessment as part of his firm’s analysis of the year-end 2023 carried loss reserve position for the P/C insurance industry, which Assured Research puts at roughly $11.7 billion redundant in a new report titled, “P&C Loss Reserves: Keep Calm and Carry On.

While that’s about half the redundancy Assured Research estimated for year-end 2022, for some well-reserved individual lines of business, including workers compensation and short-tailed property, estimated reserve redundancies are even bigger for year-end 2023 than they were for year-end 2022. (Editor’s Note: The Assured Research analysis is limited to the last 10 accident years.)

Like the year-end 2022 study, the Assured Research analysis for year-end 2023 puts the biggest deficiencies in the liability reinsurance, commercial auto liability and other liability insurance-occurrence lines. But the latest annual report notes that the industry added some $8 billion to loss reserves for these two “most problematic lines.”

“We believe a substantial portion of the adverse development expected on the problematic accident years of 2016-2019 is now behind us,” Wilt wrote in the Assured Research report, which starts with a comparison of adverse development in the other liability-occurrence line that emerged for accident years 1997-2002 during the previous hard market and expected development for accident years 2015-2019, showing a better picture for the more recent years. A graphic in the report notes, for example, that accident year 1999 ultimately had 31 loss ratio points of adverse development. In contrast, the worst year of among the 2015-2019 accident years—2017—is only expected to develop by 13 points, according to Assured Research’s latest estimates.

This article is based on the Assured Research report, “P&C Loss Reserves: Keep Calm and Carry On,” published March 19, 2024, revealing an $11.7 billion P/C industry loss reserve redundancy at year-end 2023.In last year’s report, “Year End 2022 Reserve Study: Disrupted Diagonals Manifesting,” published March 16, 2023, and in a prior report, “Assured Industry Study | 2021 Industry Reserve Analysis: Reserves Are Level Set; Bring on 2022,” Assured Research estimated redundancies of $22 billion for year-end 2022 and year-end 2021.All three reports break down the results by line of business.Assured Research’s reserve analyses cover the most recent 10 accident years only. Legacy liabilities from prior years are not considered.To learn more about Assured Research or to contact the author visit the Assured Researh websitehttp://assuredresearch.com/

Bottom line, there is still some development left in those problematic 2016-2019 accident years that executives at companies like AXIS Capital, Markel Corp., Everest Group, and Swiss Re, among others, have been talking about on earnings conference calls.

But for other liability-occurrence, what is yet to come will not put the industry back into “a 9/11-era reserving cycle,” according to the Assured Research estimates.

“We expect more adverse development for the line but we also believe the worst is over,” the report says.

In addition, Assured Research doesn’t estimate “that the industry in commercial auto has meaningfully more reserve charges to take” for the problematic accident years, Wilt said on an audio digest that he recorded to summarize the report findings for subscribers to his firm’s research.

Still, there are some problems ahead for commercial auto insurers. “It just looks bad,” he said, referring instead to concerns about the 2021, 2022 and 2023 accident years which look to be “short by some five percentage points.”

“That’s a problem not just from a reserving perspective, but also from a pricing perspective,” he said, contrasting other liability where Assured Research’s ultimate loss ratio estimate for accident year 2023 almost matches the industry aggregate ultimate loss ratio.

The report offers presentations of incremental reported loss ratio histories by accident year and development period (triangles), along with commentary, for seven of the 17 lines of business Assured Research studied—workers comp, property insurance, other liability (claims made and occurrence), private passenger auto liability, liability reinsurance and commercial auto liability.

While Assured Research estimates deficiencies of about $3 billion for both the private passenger auto liability and liability reinsurance lines, that shortfall for private passenger auto liability represents less than 2 percent of carried reserves for the line. For liability reinsurance, its more than 8 percent.

Throughout the report, Assured Research refers to the impacts of economic and social inflation on loss costs, and the pricing implications of reserve positions by line. On a “technical commentary” page of the report and in the audio digest, Wilt revealed that his firm has made explicit, conservative adjustments for inflationary impacts that “may not be baked into loss development factors” already. The conservatism probably added $18.6 billion of indicated reserves (across all impacted lines) to the analysis, he noted.

Separately, late last month, analysts at Morgan Stanley estimated that social inflation added $13.3-$24.5 billion of excess losses to the commercial auto liability line—or 7-13 industry commercial auto losses from 2013-2022.

Sclafane is Executive Editor of Carrier Management, a publication of Wells Media Group serving property/casualty insurance carrier executives. She is a media professional with deep background in the P/C insurance industry including 25 years as editor and reporter for trade magazines, online news services, digital journals. Her prior experience includes 14 years as a casualty actuary.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

Orlando Sentinel (FL) | January 14, 2024

Facing a crippling bill to repair flood damage to their homes, board members of an Orlando condo community sued their contractor this week for inflating his cost estimates — just weeks after that same contractor was arrested in Lee County for alleged overbilling.

The arrest and lawsuit — along with a companion legal filing against former board members for awarding the contract — marked the latest chapter in the horror story gripping residents of the Dockside at Ventura Condominium. Suffering some of the region’s most dramatic flooding from Hurricane Ian, the residents were hit with as much as $1,000 a month in assessments for repairs, leading to an uprising that deposed the condo board.

No sooner did a new board take over than residents became aware of the legal troubles faced by the principal owner of SFR Restoration, who was allegedly hired on a no-bid contract by the previous board and is seeking $27 million in repair bills and interest — a bracing total considering there are 266 units in the condo complex.

“Last year I was paying $483 in regular HOA fees, and then the special assessment for my size unit was $1,001,” said Elizabeth Leuven, 74. “That’s about the regular HOA if you live in Manhattan with a 24-hour concierge.”

The two suits were filed Monday in Orange County Circuit Court. The condo board is seeking relief from a judge for the contract with SFR Restoration.

The condo association also sued three former board members, who were recalled and eventually removed from their posts last year. The lawsuit alleges that Richard Pannullo, Ronaldo Loyo and Niya Loyo breached their fiduciary duty in rewarding the contract, and also that they received improper personal benefits for doing so.

Reached by phone, Pannullo said he had no comment. The Loyos couldn’t be reached.

In addition to a ruling on the validity of the construction contract, the filing against the contractor seeks an injunction on the firm’s $18 million loan to Dockside at Ventura condominiums in east Orlando. In essence, the loan allows the residents to pay off their debt to the contractor over time, and lets work proceed without waiting for an insurance settlement, but it also balloons the total bill to about $27 million including interest.

Dockside filed that lawsuit against several affiliated companies involved in the work and loan: SFR Services LLC, Southern Florida Restoration, LLC, and South Florida Real Estate, LLC. The three companies are based in Stuart and managed by Ricky McGraw, the principal of SFR.

Last month Florida Chief Financial Officer Jimmy Patronis announced McGraw’s arrest in Lee County, accused of felony charges of grand theft and insurance fraud following an investigation by the Florida Department of Financial Services. The arrest was “for his alleged involvement in intentionally inflating and overbilling a roof replacement claim to defraud Tower Hill Insurance Companyout of more than $214,000,” according to a Dec. 5 news release.

McGraw declined to comment on the lawsuit’s allegations this week, and he previously declined comment to the Insurance Journal about his arrest.

Dockside’s lawsuit alleges that SFR’s $27 million estimate “contains millions of dollars of interior work that would ordinarily be the responsibility of individual unit owners (rather than Dockside itself),” and that because it exceeds 5% of the association’s budget, the prior board should have sought multiple bids.

The community also alleges that remediation and reconstruction should have been “priced and completed for less than $10 million” and that the inflated costs were to seek a greater insurance award.

The 266-unit condo neighborhood is off Curry Ford Road just east of Semoran Boulevard in Orlando.

When Hurricane Ian blew through Central Florida in 2022, the retention pond in the middle of the community spilled over, sending floodwaters into first-floor units, and destroying vehicles in the parking lot.

Many residents were rescued by airboats after the storm.

Today most of the first floor units remain under construction, stripped down to the studs and uninhabitable for their owners.

The loan came with monthly assessments ranging from $650 per month to more than $1,000 per month depending on the unit size, stoking fears from the community of seniors and young families that they wouldn’t be able to afford to stay there. Residents began paying the new charge in October.

In the wake of the upheaval, Leuven helped organize a recall effort of the former board, which proved successful as they were ousted by an arbitrator late last year.

With the new board in place for weeks, Leuven said she and her neighbors are tired, and just want to their community back to normal.

“We need to get people back home again,” she said. “We just want to get back to how we were.”

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

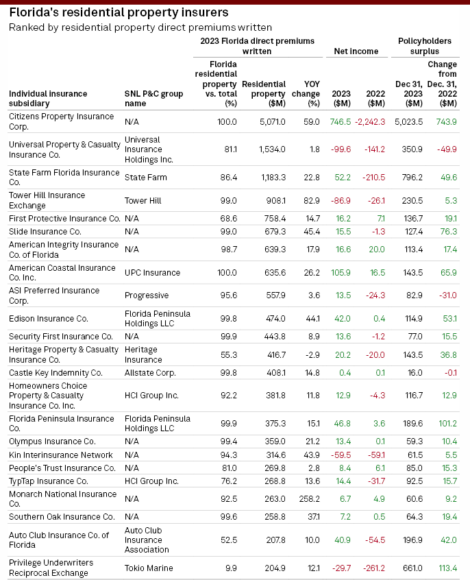

Florida’s beleaguered property insurance market is starting to look normal again, with the top insurers in the state showing a collective profit for the first time in seven years, S&P Global Market Intelligence reported this week.

The turnaround for 2023 was due in part to heightened investment income, along with improved underwriting losses aided by no major hurricane losses in the state last year, said the report by the analytics firm.

Investment income for the top 50 Florida insurers topped $346 million – more than the two previous years combined.

“On the underwriting side of the ledger, the industry posted collective losses of $190.8 million in 2023,” reads the report, which excluded the state-backed Citizens Property Insurance Corp. “Though that marked the eighth-straight year of underwriting losses for Florida insurers, it was considerably better than losses of almost $1.80 billion in 2022 and $1.52 billion in 2021.”

Overall, the top 50 carriers tallied $147 in net income for 2023, a far cry from the $1 billion in net losses reported in 2021 and in 2022.

The report was authored by senior research specialist Jason Woleben and is based on data reported by carriers to the National Association of Insurance Carriers and from Citizens’ market data and S&P Global’s own research.

Source: S&P Global report

The much-heralded legislative reforms of 2022 and 2023, which aimed to disincentive baseless claims lawsuits – shown to be a major cost driver in Florida –appear to have had an impact on insurers’ litigation costs. Direct incurred defense expenses fell to $739 million last year. While still a huge number, it’s far less than the $1.6 billion bleed seen in 2022, the report noted.

The defense and cost-containment expense ratio, considered a key measurement of the impact of litigation, fell to 3.1, down from 4.7 in 2019 and 8.4 in 2022.

But Florida, known for leading the nation in claims lawsuits, is still “far and away” producing the highest defense costs. The national median ratio is 1.2. By comparison, California-based insurers reported $402 million in litigation costs in 2023, followed by Texas, with $285 million, S&P said.

Most insurers remain optimistic about the long-term impact of the legislative reforms, though, Woleben reported.

Citizens showed continued growth in 2023, the analysis noted. But this year, Citizens’ own reports show that the insurer has slimmed down a bit, from 1.23 million policies in force at the end of last year to 1.17 million in February before climbing slightly to 1.18 million in March. Total direct premiums for Citizens climbed 53% in 2023, to more than $5 billion, the S&P report noted.

The analysis also looked at some of the numbers for individual carriers. Universal P&C Insurance Co., the second-largest property insurer in the state, reported a $99 million net loss in 2023, which was an improvement over 2022’s losses. Policyholder surplus fell by $50 million for Universal.

State Farm’s Florida subsidiary saw a $52 million profit, up from its $211 million net loss the year before. Tower Hill Exchange saw another net loss in 2023, of $87 million. That followed a $26 million loss in 2022.

Security First Insurance notched a $13.6 million profit in 2023. People’s Trust Insurance was $8.4 million in the black.

Rabb is Southeast Editor for Insurance Journal. He is a long-time newspaper man in the Deep South; also covered workers’ comp insurance issues for a trade publication for a few years.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer

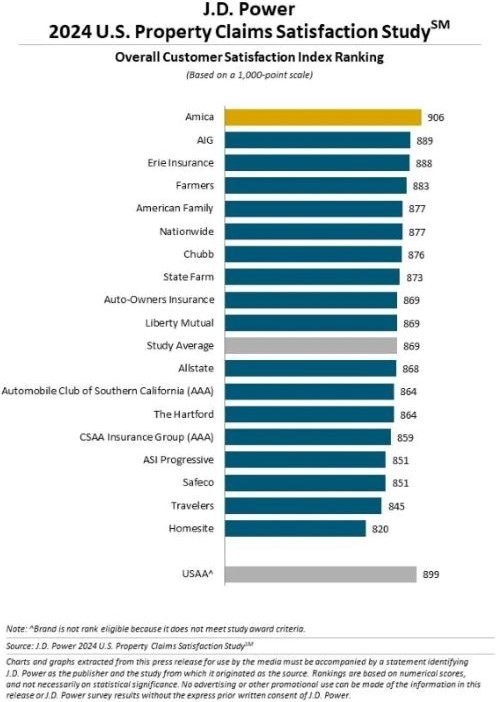

With 28 catastrophic weather events in 2023 causing nearly $93 billion in damage, customer service satisfaction plunged to a seven year low, according to the latest J.D. Power 2024 U.S. Property Claims Satisfaction Study released today.

More extreme weather events led to a larger number of high-severity claims and longer claims settlement times, negatively affecting satisfaction, which declined to the lowest level in seven years, the report said.

The average claims cycle time—the amount of time from reporting the claim to finished repairs—has now reached 23.9 days, over six days longer than in 2022.

For claims related to catastrophic events, that average repair cycle time jumped to 34.2 days.

As a result, customer satisfaction has declined by five points to 869 (on 1,000-point scale) from a year ago, the study found.

The average overall satisfaction score among customers who experienced catastrophic claims is 841.

“Catastrophic weather events are straining an already fragile system still experiencing supply chain issues that affect the availability and cost of materials,” said Mark Garrett, director of claims intelligence at J.D. Power. “Resources become strained for both insurers and the contractors doing the work. Unfortunately, it’s when claims last beyond three weeks that J.D. Power sees things decline. When claims last less than three weeks, satisfaction improves, so it’s the longer claims that are solely responsible for the decline. Insurers are challenged to manage expectations and proactively communicate during longer claim periods as customers tend to have more questions when experiencing delays.”

Surprisingly, even customers who utilized digital tools for reporting claims or submitting photos and experienced faster claim cycle times didn’t always report higher levels of overall satisfaction.

Claims taking longer than expected are partially to blame as satisfaction dropped at a greater pace among digital users than non-digital users, J.D. Power said.

Overall satisfaction among customers reporting their claim digitally is 903 when the claim is settled in less than three weeks, but that score fell to just 727 after 31 days.

“Insurers are offering digital tools and managed repair partners to help streamline the process, but these efforts are met with mixed results,” Garrett said. “Customers still expect things to move along quicker so expectation management is key.”

Because of rising insurance premiums, when customers have a claim and have to cover $1,500 or more in costs, the study found that satisfaction is negatively affected, even if it is to cover their deductible.

The increasing frequency of catastrophic weather events coupled with policies that often have higher deductibles for this type of weather event (wind, hail, named storms, etc.), means more customers will be paying higher deductibles.

J.D. Power reported a five-percentage-point increase to 28% from 23% in 2022 among those spending $1,500 or more for either their deductible or out-of-pocket expenses, with satisfaction declining 27 points.

Customers using digital tools to report claims and submit photos tend to have lower severity claims and report faster repair cycle times of 15 days, on average, compared with nearly 28 days among non-digital users.

“No time is more critical than during the initial reporting of the claim,” Garrett said. “The biggest declines in satisfaction are related to explaining the claims process to customers and showing concern for their situation. To navigate this difficult stage, insurers need to redouble their efforts to proactively manage customer expectations and streamline the claims process.”

When multiple insurance representatives are involved in claims handling, consistency of service is an important driver of satisfaction, J.D. Power noted.

“From sharing information so the customer does not need to repeat themselves to reps having similar knowledge and soft skills is critical in delivering very consistent levels of service,” the study noted.

Among the 27% of customers who report that level was not achieved, satisfaction dropped 200 points.

Amica, AIG, and Erie Insurance ranked highest in overall customer satisfaction.

WPTV West Palm Beach, FL

WPTV West Palm Beach, FL Action News Jax

Action News Jax