Universal Insurance Holdings Inc., the parent company of Universal Property & Casualty Insurance Co., Florida’s second-largest carrier, posted a $72 million loss for the third quarter of this year. That’s in contrast to a $20 million profit for Q3 2021.

The publicly traded company (UVE on NYSE) said in a statement that the losses are largely the result of Hurricane Ian, which struck southwest Florida two days before the quarter ended. The $110 million in Ian losses were offset by Universal’s lowered expense ratio and higher investment income and commission revenue.

The company reiterated that total storm losses were not expected to be more than $1 billion, less than some in Florida had expected, because Universal writes only about 3.8% of the market (by value) in four of the hardest-hit counties. By comparison, Citizens Property Insurance Corp., the state-created insurer of last resort and the largest P/C carrier in the state, expects about $2.6 billion in insured losses from Ian.

“As we recently disclosed, our portfolio is underweight in the most impacted regions and is further cushioned by our high proportion of condo unit and renters policies, which provide interior and contents coverage,” not roof and exterior structure coverage, Universal CEO Stephen Donaghy said Thursday.

Donaghy

So far, claims volume from Hurricane Ian reflects about 50% of Hurricane Irma’s volume that the insurer had received at this point in 2017. Through mid-October, Universal had received about 18,000 claims from Ian.

The firm also said it maintains a $3 billion reinsurance tower, providing protection should another named storm hit the state. “Our consolidated retention would be meaningfully lower, highlighting the strength and breadth of our catastrophe reinsurance program,” the company statement noted.

Unlike a number of other Florida property insurance executives, which have fretted about the rising cost of reinsurance, Donaghy appeared less concerned. He noted that the company has protection through catastrophe bonds, through the Reinsurance to Assist Policyholders, known as the RAP fund that was created by the Legislature earlier this year, and from other sources.

“Coupled with our 90% participation in the FHCF (Florida Hurricane Catastrophe Fund), we estimate that the vast majority of our first-event 2023 catastrophe reinsurance program will be insulated from open-market pricing dynamics,” he said.

Overall, Universal, which has worked to shed policies in the last 12 months, said it had 872,926 policies in force at the end of the third quarter, down almost 10% from a year ago. But it also had $501 million in direct premiums written – up 16% from this time in 2021.

Total revenues for the carrier for the nine months that ended Sept. 30 were more than $892 million, a 7.6% increase from the first nine months of 2021.

Top photo: Satellite image of Hurricane Ian, taken Sept. 28, just before landfall. (NOAA via AP)

It has been a month since Hurricane Ian wiped out parts of southwest Florida. Now multimillion-dollar cleanup contracts are generating new tempests in the Category 4 storm’s wake.

Contractors who remove debris and perform post-storm repairs are fighting over local government contracts that could be worth tens of millions in tax dollars. The skirmishes offer a preview of likely fights over local, state and federal funds that will be distributed over the next several months to help southwest Florida get back on its feet.

A case in point is the recent contentious expansion of a land-based storm debris removal contract that had been put out to bid well before the hurricane. Coincidentally, the contract was awarded to Crowder-Gulf Joint Venture just days after Ian made landfall at the county’s Cayo Costa State Park on Sept. 28.

In response to the wide hurricane damage, county officials expanded the contract’s scope on Oct. 2 to include waterways and private property.

(AP Photo/Gerald Herbert)

Disposing quickly of downed trees, blown-off roof shingles and shredded drywall is one of the most challenging but important parts of hurricane recovery. County officials want to get the job done speedily since local governments get direct payment from the Federal Emergency Management Agency for the cost of debris picked up within 60 days of a storm. Officials estimate Lee County has 1.8 million cubic yards of storm debris.

“We are bumping up against some very important timelines,” Lee County Commissioner Ray Sandelli said at a recent meeting.

But Bart Smith, an attorney for one of the contractors that lost the bid to Crowder-Gulf Joint Venture, told Lee County commissioners that not putting the extra work contained in the contract’s expansion out to bid put them at risk of a “clawback,” which is when FEMA takes back previously awarded money.

“Decisions are always made after storms, and these are emergencies, but you have to understand that hindsight is 20-20 and FEMA, when they do all these reimbursements years later and review it and audit it and then tell you you have to give the money back, there are ramifications,” Smith said.

Daniella Sanabria, an attorney for another rival contractor, also warned commissioners about a possible clawback, saying the expansion of the debris-removal contract to cover waterways and private properties was anti-competitive.

“In light of Hurricane Ian, it’s an enormous addition to the contract’s scope, potentially worth hundreds of millions of dollars,” Sanabria said. “It’s being improperly and uncompetitively awarded.”

The federal government regularly claws back disaster money that it believes was incorrectly distributed or when procedures weren’t followed correctly. Federal agencies tried to take back $73 million from more than 1,800 New Jersey households that received federal disaster monies from Superstorm Sandy a decade ago. After Hurricane Irma in 2017, FEMA claimed $4.3 million in clawbacks from Lake Worth Beach, Florida.

Officials have estimated the damage caused by Ian in Florida and North Carolina at anywhere from $40 billion to $70 billion, making it among the costliest storms ever to hit the U.S. At least 118 deaths in Florida are attributable to the storm.

Lee County’s manager, Roger Desjarlais, dismissed the complaints, saying that vendors who don’t get a piece of the pie will try to “muddy the waters” because so much money is at stake in hurricane cleanup efforts.

“Every time, disaster politics takes over at some point because there is so much money to be made by some of these companies, millions of dollars,” Desjarlais said.

Because the money awarded for cleanup is so large, it can be an easy target for corruption. In Bay County, Florida, where a Category 5 storm, Hurricane Michael, made landfall in 2018, 10 businessmen and high-ranking officials from the city of Lynn Haven were indicted on charges of theft or fraud for allegedly overbilling or billing for cleanup work that was never performed. Federal prosecutors have obtained guilty pleas from seven of the 10 defendants.

Douglass Whitehead, Lee County’s solid-waste director, said the new, expanded contract with Crowder is cheaper per truckload than the old contract, under which costs had risen due to inflation. He said expanding a contract already in place provides continuity in an emergency situation.

But two of the five commissioners said no to the deal when it came up for a vote last week.

“I’m going to vote against the motion,” Commissioner Brian Hamman said at the time. “I don’t feel comfortable with the way it’s gone down.”

Photo: A crew collects debris from Ian, at Ponte Vedra Beach, Florida. (Phelan M. Ebenhack via AP)

Copyright 2022 Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

NEWYou can now listen to Insurance Journal articles!

Listen to this article

0:00 / 1:571X

A 14-story condominium building in Miami Beach, less than two miles from the collapsed Champlain Towers South, has been ordered evacuated after engineers found expanding cracks in a main support beam.

The Miami Herald reported Thursday that city officials ordered residents of the 164-unit Port Royale, at 6969 Collins Ave., to clear out immediately. Engineers plan to reinforce the damaged support structure within 10 days, but it wasn’t clear when or if residents will be allowed to return.

A Miami-Dade County ordinance, approved after the Champlain Tower in nearby Surfside collapsed in June 2021, killing 98 people, requires condo building owners to provide three months of housing if the structure is deemed unsafe due to negligence or lack of maintenance, the newspaper reported. It was unclear if the Port Royale management was offering the assistance at this time, the newspaper said.

The Port Royale building is undergoing repairs identified as part of its 50-year recertification, required by law. Inspectors recently found spalling, cracking and other deterioration, and temporary supports had been installed. But a letter from an engineering firm this week said that needed repairs for a main support beam in the garage were much more complicated that originally expected, the Herald noted. The city of Miami Beach also had issued an “unsafe structure notice.”

Engineers and municipal inspectors in south Florida are working to evaluate hundreds of buildings after the 2021 collapse put officials on high alert, and after new statutes required more inspections. The Florida Legislature in May approved Senate Bill 4D, which requires inspections for high-rise condos in Florida 30 years after construction, and more frequently for structures closer to the coast.

Another condo building near the collapse site was ordered evacuated in April of this year after a scheduled recertification process found it to be unsafe.

Photo: The site of the Champlain Towers South, which collapsed in June 2021, north of Miami Beach. (AP Photo/Gerald Herbert, File)

NEWYou can now listen to Insurance Journal articles!

Listen to this article

0:00 / 6:071X

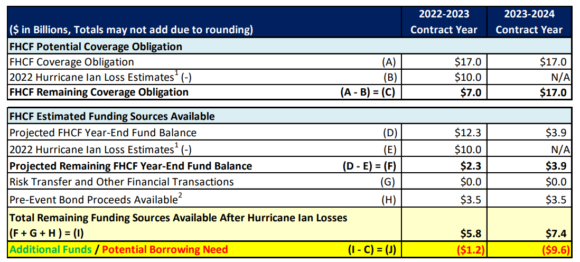

The Florida Hurricane Catastrophe Fund is well equipped to handle losses from Hurricane Ian, which are now estimated to cost the fund about $10 billion, but it could mean the fund will have borrow billions next year – at steep interest rates.

“We’ve been here before. We’re going to do what we’ve always done, and we’ve done it well,” Gina Wilson, chief operating officer of the cat fund, said at a fund advisory council meeting this week. “We are well-prepared for Hurricane Ian and we can cover our obligations.”

A claims-paying capacity report from the Raymond James investment banking firm, which advises the cat fund, backed up Wilson to a large degree. But it also indicated that the fund’s surplus could fall short next year, even without another storm.

“After adjusting for Hurricane Ian loss estimates, the FHCF has liquid resources that are significantly below its statutory limit for the subsequent season,” reads the report, presented by Kapil Bhatia of Raymond James.

The report shows that the cat fund will likely need to borrow as much as $1.2 billion this year and another $9.6 billion for the 2023-2024 contract year to meet its statutory obligations.

“The projected 0-12 month bonding capacity of $8.4 billion allows for the FHCF to fund a majority of its maximum statutory obligation, but additional funding sources are needed to fund its statutory limit of $17 billion for the 2023-2024 Contract Year,” the Raymond James analysis said.

And while the cat fund can lay a surcharge on Florida policyholders if needed, and has an excellent credit rating, it’s not guaranteed by state government. Given the current volatility of the global market now, along with rising interest rates and inflation, the cat fund could expect to pay bond interest rates as high as 7% to 9%, Bhatia said.

The report’s findings appear to give some credence to warnings raised earlier this month from analysts who fear that issuing bonds could be prohibitively expensive for the fund and would ultimately mean less cat fund reinsurance for Florida property insurers.

The principal and interest on new debt would mean “they never build surplus – even with no losses,” said Ian Gutterman, of Chicago, founder of a startup insurance company and a longtime insurance industry analyst and blogger. “There would be years with no debt maturities where surplus would temporarily build but then it would be drained by the next maturity.”

In other words, a bond buyer would have to assume either no more hurricanes will strike Forida for as long as the debt is outstanding, perhaps 10 years, or if there is one, the state of Florida will make good on the bonds if the cat fund doesn’t have the resources, Gutterman said.

“But there is no path for the FHCF on its own to both pay a future hurricane claim AND pay back bondholders,” he argued. “The debt can get you through, but the debt has to be paid back. And if you have more hurricanes, what do you have to pay the debt back with?”

The crux of the issue is that the fund’s diminished liquidity could force some insurance companies to seek more reinsurance coverage from the private market. With reinsurance prices expected to rise again next year, that could lead to lowered financial ratings and could doom a number of insurers that are now teetering, Gutterman and others have said.

The Raymond James analysis underscored the problem of escalating reinsurance costs.

“Due to Hurricane Ian losses and global macroeconomic factors, the global reinsurance markets are expected to harden further, which will further reduce the reinsurance capacity for the Florida market,” the report said.

John Rollins, an actuary and former chief financial officer for a large Florida insurance carrier, also questioned some of the cat fund’s recent assumptions, highlighted in the Raymond James analysis.

“The first question is, how lucky do Florida leaders feel about each of those ‘no shock’ assumptions?” he wrote on his Linkedin page. “Irma loss estimates have proved low at each milestone, and the fund must commute with 100+ individual insurers by June 2023 to determine the final tally.”

The Raymond James review also noted that the retention level – the deductible that insurers must pay before they can tap into the cat fund’s low-cost reinsurance – will rise to $9.1 billion for next year, up from $8.5 billion.

“Can insurers survive an inflation of the retention to $9.1 billion next year and an increase in premiums to $1.6 billion next year, or will legislators reform the fund and reduce premiums?” Rollins asked.

Florida Gov. Ron DeSantis said this month that he will convene a special session of the Legislature, probably in late November or early December, to tackle some of the most pressing issues still facing Florida insurers. Lowering the retention level on the cat fund has been discussed for years as a way to save Florida insurers on their reinsurance costs. But it’s not yet clear if that will be on lawmakers’ agenda. Other ideas include outlawing assignment-of-benefits agreements, a move that could stem the number of claims lawsuits filed in Florida.

Others have suggested that Ian’s impact won’t be so drastic. The cat fund won’t have to pay all of its reimbursement obligations at once but will likely space payments out over the next several years.

Wilson, the cat fund’s COO, told the advisory council meeting that for Hurricane Irma, in 2017, and Michael in 2018, FHCF has incurred losses of $9.25 billion but has not quite finished paying on that. The fund has paid 137 insurers for losses in the two storms, but expects to reimburse about seven more carriers.

Wilson also said that no insurers have yet requested reimbursement for Hurricane Ian losses. But when they do, the fund should be able to pay quickly.

The $10 billion projected cat fund loss from Hurricane Ian, which made landfall in southwest Florida on Sept. 28 of this year, is a “conservative point” in a range arrived at by the cat fund’s consulting actuary, based on a range of factors, the Raymond James report noted. The actuary, Paragon Strategic Solutions, has estimated that FHCF’s share of losses will be between $4 billion and $12 billion.

“There is significant uncertainty regarding the ultimate loss amount as losses are just beginning to develop,” the Raymond James analysis said. “Estimates are based on the output of models and are subject to significant uncertainty; therefore, there is no guarantee that actual losses will fall within the projected range.”

Top chart: From an Oct. 26 Raymond James analysis of the FHCF’s claims-paying capacity.

Rabb is Southeast Editor for Insurance Journal. He is a long-time newspaper man in the Deep South; also covered workers’ comp insurance issues for a trade publication for a few years.

Florida’s property insurance crisis continues to worsen, despite recent legislative changes focused on stabilizing the rapidly collapsing home insurance market. Many property insurance companies continue to liquidate or no longer write new business in Florida, and many of the remaining carriers are requesting rate increases. What’s worse, potential financial strength rating downgrades could cause issues for millions of homeowners. Bankrate dug deep into the Florida insurance industry to discover the cause of this problem. We can help you understand why the Florida home insurance crisis is happening and your options if you receive a cancellation or nonrenewal notice on your homeowners insurance policy.

Key insights

Florida’s home insurance crisis is picking up speed as rates potentially increase and financial strength ratings worsen.

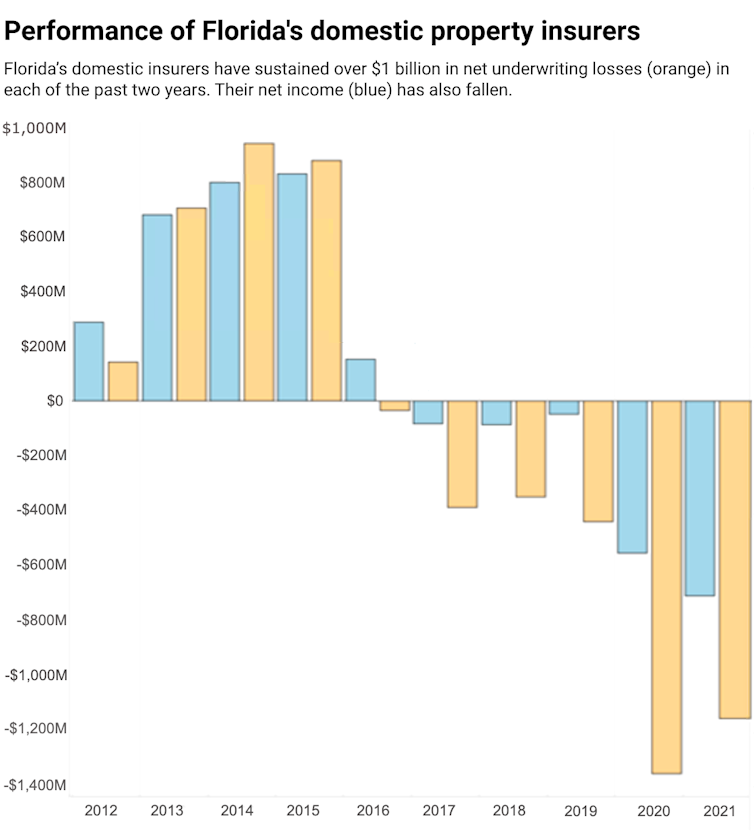

Florida accounts for only 9% of the country’s home insurance claims but 79% of its home insurance lawsuits, many of them fraudulent.

Because of the fraudulent lawsuits and the high overall claim risk in Florida, insurance companies have faced two consecutive years with net underwriting losses over $1 billion.

The effects of September’s Hurricane Ian will likely put further strain on Florida insurers and could worsen the crisis.

The crisis in the Florida insurance market

Florida has always been a complex home insurance market, but recent issues are pushing the state’s market to the point of collapse. Since 2017, six property and casualty companies that offered homeowners insurance in Florida liquidated. Five more are in the liquidation process in 2022. Other insurance companies are voluntarily leaving the state. Even more are choosing to nonrenew swaths of home insurance policies, drastically tighten their policy eligibility requirements or request substantial rate increases.

For Florida homeowners, this is resulting in fewer home insurance companies and increased premiums. When a company goes insolvent, the Florida Insurance Guaranty Association (FIGA) takes on any claims that still need to be paid by that company. In late August, FIGA’s board and the Florida Office of Insurance Regulation (OIR) approved a .7 percent assessment to help cover the costs of open claims associated with the liquidated companies. That’s the second assessment this year, with a 1.3 percent assessment approved in March. Homeowners will pay these fees regardless of the insurance company they are with.

According to Logan McFaddin, Vice President of State Government Relations at the American Property Casualty Insurance Association,

Florida’s property insurance market is in crisis as insurers grapple with out-of-control litigation costs and billions in losses from recent natural disasters.

Florida’s Insurance Consumer Advocate (ICA) Tasha Carter agrees, saying, “Homeowners insurance options in Florida have become more and more limited, and consumers are facing dire consequences.”

Why are home insurance companies leaving Florida?

Florida insurers are canceling policies, leaving the state or liquidating at a rapid pace. Why? What is behind these companies’ aversion to insuring Florida homes?

Florida has always presented a risky market to home insurance companies due to the high threat of widespread weather-related damage, but the current crisis is caused by a number of factors reaching a boiling point at the same time.

Insurance fraud in Florida

The biggest issue right now in Florida is home insurance fraud, driven by fraudulent roofing claims. A proclamation from the office of Governor Ron DeSantis notes that, although Florida only accounts for 9% of the country’s home insurance claims, it is home to 79% of the country’s home insurance lawsuits. Many of these lawsuits are fraudulent. ICA Carter explains how the scams generally work:

First, roofers canvas neighborhoods and offer inspections to unsuspecting homeowners. These contractors inevitably “find damage” on the roof and often promise a “free roof” to the homeowner, claiming they can have the home insurance deductible waived.

Homeowners are pressured to sign an assignment of benefits form, giving contractors the right to file an insurance claim on their behalf.

A claims adjuster from the insurance company inspects the alleged damage. The adjuster either finds no damage or far more minimal damage than the contractor found, and the claim payout is less than what the contractor demanded.

The contractor brings legal action against the insurance company, demanding a claim payout for the contractor’s original quote. Remember, the homeowner signed the benefits of the policy to the contractor, so the contractor doesn’t need the homeowner’s permission to do this.

The insurance company now has a choice: it can pay the legal costs to fight the lawsuit or pay the costs to settle out of court. Either way, the insurance company loses money due to the legal action.

ICA Carter notes that “these schemes are real and are happening more frequently,” which puts more and more financial pressure on insurance companies, especially in a state with high claims costs due to weather-related events.

According to Mark Friedlander, Director of Corporate Communications at the Insurance Information Institute, “Florida property insurers are projected to post a cumulative underwriting loss of $1.7 billion for 2021” due to these runaway litigation costs. The governor’s office reports that, for two consecutive years, net underwriting losses have exceeded $1 billion. It’s no wonder that so many companies are going insolvent or leaving the state before they reach that point.

Roof age

Instead of leaving altogether, some companies are tightening their underwriting restrictions to lessen the risk of these scams. This may be the reason why several companies — including Southern Fidelity, Progressive and Universal — have chosen to continue operations in Florida but have nonrenewed tens of thousands of policies.

However, companies are now prohibited from denying coverage solely based on roof age if the roof is fewer than 15 years old and has a life expectancy of five years at the time the policy is issued. That said, insurers will have to decide if they are comfortable with these restrictions or if they will continue leaving Florida.

Storm risk

Risk will always be a consideration for home insurance companies in Florida. The state’s shape and geographic location mean that it could get hit from either side by a hurricane. Because the peninsula is so thin, even homes in the interior counties aren’t entirely protected.

To make matters worse, fraudulent claims may be more common after severe storms — and storms may be coming. Colorado State University predicts that the 2022 hurricane season will be more severe than usual, with 18 named storms, including eight hurricanes, four of which are predicted to be “major.” Hurricane Ian made landfall on September 28 as a powerful Category 4 storm, causing widespread damage. The full effects of the storm may not be known for weeks or months, but the damage could push the already-teetering home insurance market into collapse due to increased home repair expenses, including the potential of fraudulent roof claims.

However, although the risk of hurricane damage complicates things, it isn’t what’s driving the market to the brink of collapse. After all, other risky states don’t have this problem. A high likelihood of damage generally means paying a higher premium to offset that risk, but coverage is usually still available. Oklahoma, for example, has the highest average cost of home insurance in the nation at $3,593 per year for $250K dwelling coverage due to the likelihood of tornado damage, but homeowners in the state don’t face the same difficulty finding coverage that Floridians do.

Is anything being done to curb the crisis?

Yes, although the full effects of the measures have yet to be seen. Senate Bill 76 went into effect in July 2021 and included several provisions to curb fraudulent claims causing insurers so much strain. One such provision is aimed at reducing the solicitation tactics that fraudulent contractors often use at the start of a scam. While this legal measure may help solve the problem, Sean Harper, CEO of Kin Insurance, warns that “there will need to be additional action taken to restore the market to health.”

Florida lawmakers met for a special session from May 23 through May 27. The Legislature passed an insurance reform bill that includes several provisions to help slow the spiral of the market. The provisions included setting up the My Safe Florida Home Program, which provides grants to help Florida homeowners strengthen their homes against damage. Additionally, home insurance companies will not be able to deny coverage for homes solely based on roof age if a roof is less than 15 years old and still has five years of useful life left (older roofs may still be denied as they present a high risk of damage). Finally, lawyers will be restricted in the rates they can charge for property insurance claims cases, hopefully discouraging fraudulent lawsuits and decreasing litigation costs.

Recent developments: Demotech responds to potential rating downgrades

Because many home insurance companies have been hit hard by the rampant and fraudulent litigation, they may no longer be as financially stable as they were. In late July 2022, financial strength rating company Demotech announced it was considering downgrading the financial strength ratings of 27 property insurance companies.

The situation is complex. While these carriers may no longer have the financial strength they used to, downgrading also causes issues. Downgrading financial ratings impacts homeowners with federally-backed mortgages — those from Fannie Mae and Freddie Mac — because these lenders require home insurance companies with Demotech ratings to maintain at least an ‘A’ level. Demotech has not released the names of the companies it is considering downgrading.

“Preliminary evaluations are just that — preliminary,” Demotech President Joe Petrelli told Bankrate. Some of the 27 could retain an ‘A’ or higher rating. But if these downgrades happen, homeowners whose coverage is with an affected company may need to find another insurance carrier in a market where options are already limited or expensive.

While a rating downgrade may present challenges for a company and its insureds, that hardship cannot, and does not, factor into our ratings, which are based on specific data and the objective application of our rating methodology.

— Joe PetrelliPresident of Demotech

The Florida OIR established a reinsurance fund through its last-resort insurer, Citizens. This means that if an insurance company’s financial strength rating is downgraded below the ‘A’ level, the downgraded company could purchase coverage from Citizens to back it, similar to a co-signer backing a loan. Reinsurance through Citizens would allow the downgraded insurance company to meet Fannie Mae and Freddie Mac’s requirements. This is important because it would prevent policyholders from being required to find a new property insurer. However, a reinsurance solution further strains Citizens, which is already taking on substantial risk by insuring more policyholders in the state as other insurance companies exit Florida.

On September 9, the Florida legislature approved a $1.5 million plan to search for a financial strength rating company to replace Demotech. The state will hire a consultant to seek out alternatives that may include finding another company or creating a state-backed financial strength rating agency. Petrelli released a statement in response:

“Since 1996 in Florida, Demotech has provided neutral, unbiased ratings to property insurers, among the approximately 50,000 such ratings we have produced across the country. Our review and analysis process has remained consistent throughout this time. Currently, at least four rating organizations acceptable to the government-sponsored mortgage enterprises operate in Florida and countrywide, and a research effort on rating alternatives could be accomplished at no cost to the taxpayers by reviewing existing Freddie Mac and Fannie Mae sellers or servicer guides. Today’s action is an unnecessary response to a problem that does not exist. The reality is that when Hurricane Andrew devastated the state nearly 30 years ago, the rating agencies involved in Florida chose to step away — but Demotech stepped up.”

It remains to be seen if finding another ratings agency will produce meaningful results toward correcting the Florida home insurance crisis. As always, Bankrate continues to monitor the situation.

How to lessen your risk of nonrenewal

If you live in Florida, having a plan could help you lessen your risk of receiving an insurance nonrenewal. There’s nothing you can do to prevent your company from pulling out of the state, but there are steps you can take to make your home as insurable as possible:

Keep your roof updated and in good shape: Inspect your roof regularly and repair minor damage as it happens. If you can afford to, replace your roof before it reaches 15 years of age to lessen the risk of being nonrenewed.

Install wind mitigation features: State law requires Florida home insurance companies to offer discounts for certain wind protection features, such as hurricane straps and other roof-bracing measures. These features lessen the risk of severe damage to your home, thus making your property more attractive to insurers.

Maintain your property: Generally, maintaining your property will make finding insurance coverage easier. Along with checking your roof, also regularly check the rest of the exterior features of your home for damage. You should also make sure no large tree branches or other potential hazards overhang your home, as these could put you at risk of roof damage in a windstorm.

Additionally, there are ways you can lessen the impact of home insurance fraud and help keep companies from having to liquidate. ICA Carter points out that “consumers have the power to help stop contractor fraud by being informed and reporting fraud.”

Know the signs and stay educated: ICA Carter created educational resources called “Demolish Contractor Fraud: Steps to Avoid Falling Victim” that may help homeowners recognize the signs of fraud, stop it before it happens and report it.

Be wary of solicitation: Soliciting business isn’t against the law, but contractors who canvas neighborhoods after storms — and especially those who offer incentives and rebates for an inspection — may be part of a scam. Instead, contact your insurance company if you are concerned your home sustained damage after a storm.

Do not sign an assignment of benefits form: By keeping control of your policy, you decide if a lawsuit is filed, which vastly cuts down on fraudulent litigation. It’s worth noting that these forms are often buried within otherwise legitimate-looking contracts. Once you’ve signed, the form is legally binding, so it’s important to read everything you are asked to sign. Do not let a contractor simply point out a signature section on paperwork or scroll past the details on a tablet screen. Read the entire document carefully.

Additionally, some companies now offer a discount if you agree to make your policy unassignable. Kin is one such company, and Harper notes that having a high number of unassignable policies has shielded the company from much of the litigation nightmare ensnaring other carriers.

What to do if your home insurance has been canceled

If you’ve received a Florida homeowners insurance cancellation, act quickly. With hurricane season approaching and the insurance market in turmoil, getting another policy could be difficult, but it is possible.

McFaddin recommends that you “work closely with your insurer or insurance agent to see what options may be available to you.” ICA Carter’s advice was similar, advising that “consumers should contact their insurance agency immediately to determine what their options are for homeowners insurance.”

If you’re struggling to find home insurance coverage in Florida, there are still a few companies that may be able to help.

Hurricane risk might seem like the obvious problem, but there is a more insidious driver in this financial train wreck.

Finance professor Shahid Hamid, who directs the Laboratory for Insurance at Florida International University, explained how Florida’s insurance market got this bad – and how the state’s insurer of last resort, Citizens Property Insurance, now carrying more than 1 million policies, can weather the storm.

What’s making it so hard for Florida insurers to survive?

One is the rising hurricane risk. Hurricanes Matthew (2016), Irma (2017) and Michael (2018) were all destructive. But a lot of Florida’s hurricane damage is from water, which is covered by the National Flood Insurance Program, rather than by private property insurance.

Another reason is that reinsurance pricing is going up – that’s insurance for insurance companies to help when claims spike.

But the biggest single reason is the “assignment of benefits” problem, involving contractors after a storm. It’s partly fraud and partly taking advantage of loose regulation and court decisions that have affected insurance companies.

It generally looks like this: Contractors will knock on doors and say they can get the homeowner a new roof. The cost of a new roof is maybe $20,000-$30,000. So, the contractor inspects the roof. Often, there isn’t really that much damage. The contractor promises to take care of everything if the homeowner assigns over their insurance benefit. The contractors can then claim whatever they want from the insurance company without needing the homeowner’s consent.

If the insurance company determines the damage wasn’t actually covered, the contractor sues.

So insurance companies are stuck either fighting the lawsuit or settling. Either way, it’s costly.

Other lawsuits may involve homeowners who don’t have flood insurance. Only about 14% of Florida homeowners pay for flood insurance, which is mostly available through the federal National Flood Insurance Program. Some without flood insurance will file damage claims with their property insurance company, arguing that wind caused the problem.

How widespread of a problem are these lawsuits?

Overall, the numbers are pretty striking.

About 9% of homeowner property claims nationwide are filed in Florida, yet 79% of lawsuits related to property claims are filed there.

The legal cost in 2019 was over $3 billion for insurance companies just fighting these lawsuits, and that’s all going to be passed on to homeowners in higher costs.

Insurance companies had a more than $1 billion underwriting loss in 2020 and again in 2021. Even with premiums going up so much, they’re still losing money in Florida because of this. And that’s part of the reason so many companies are deciding to leave.

Assignment of benefits is likely more prevalent in Florida than most other states because there is more opportunity from all the roof damage from hurricanes. The state’s regulation is also relatively weak. This may eventually be fixed by the legislature, but that takes time and groups are lobbying against change. It took a long time to pass a law saying the attorney fee has to be capped.

Thirty more are on the Florida Office of Insurance Regulation’s watch list. About 17 of those are likely to be or have been downgraded from A rating, meaning they’re no longer considered to be in good financial health.

The ratings downgrades have consequences for the real estate market. To get a loan from the federal mortgage lenders Freddie Mac and Fannie Mae, you have to have insurance. But if an insurance company is downgraded to below A, Freddie Mac and Fannie Mae won’t accept it. Florida established a $2 billion reinsurance fund in May 2022 that can help smaller insurance companies in situations like this. If they get downgraded, the reinsurance can act like co-signing the loan so the mortgage lenders will accept it.

But it’s a very fragile market.

Ian could be one of the costliest hurricanes in Florida history. I’ve seen estimates of $40 billion to $60 billion in losses. I wouldn’t be surprised if some of those companies on the watch list leave after this storm. That will put more pressure on Citizens Property Insurance, the state’s insurer of last resort.

Some headlines suggest that Florida’s insurer of last resort is also in trouble. Is it really at risk, and what would that mean for residents?

Citizens is not facing collapse, per se. The problem with Citizens is that its policy numbers typically swell after a crisis because as other insurers go out of business, their policies shift to Citizens. It sells off those policies to smaller companies, then another crisis comes along and its policy numbers rise again.

Three years ago, Citizens had half a million policies. Now, it has twice that. All these insurance companies that left in the last two years, their policies have been migrated to Citizens.

Ian will be costly, but Citizens is flush with cash right now because it had a lot of premium increases and built up its reserves.

It has the Florida Hurricane Catastrophe Fund, established in the 1990s after Hurricane Andrew. It’s like reinsurance, but it’s tax-exempt so it can build reserves faster. Once a trigger is reached, Citizens can go to the catastrophe fund and get reimbursed.

More importantly, if Citizens runs out of money, it has the authority to impose a surcharge on everyone’s policies – not just its own policies, but insurance policies across Florida. It can also impose surcharges on some other types of insurance, such as life insurance and auto insurance. After Hurricane Wilma in 2005, Citizens imposed a 1% surcharge on all homeowner policies.

Those surcharges can bail Citizens out to some degree. But if payouts are in the tens of billions of dollars in losses, it will probably also get a bailout from the state.

So, I’m not as worried for Citizens. Homeowners will need help, though, especially if they’re uninsured. I expect Congress will approve some special funding, as it did in the past for hurricanes like Katrina and Sandy, to provide financial aid for residents and communities.

It has been three weeks since Hurricane Ian struck Florida on Sept. 28, 2022. The storm took at least 119 lives and caused estimated insured losses ranging from $31 billion to $74 billion, with most estimates in the $60 billion neighborhood. These damages exceed those caused by any other U.S. natural catastrophe, with the exception of Hurricane Katrina.

Above and beyond the tragic ongoing personal and economic hardship wrought, Ian will leave a troubling legacy in Florida’s insurance and real estate markets. Prior to Ian, homeowners insurance premium for Floridians was already three times the national average. The state’s property insurance market was already faltering and under extreme stress, with half a dozen insurance carriers in the state declaring insolvency in 2022 alone.

And this is just the beginning. The storm’s aftermath will cause insurance rates to increase, rendering insurance coverage so out of reach that Florida home values will drop for want of buyers.

At the core of these rising insurance rates is the shrinking availability and affordability of reinsurance.

Reinsurance is insurance bought by insurance companies

Reinsurance acts as a shock absorber in the insurance industry by assuming risk above and beyond what insurance companies are willing to bear.

Jerry Theodorou

Insurance companies buy one type of reinsurance—excess of loss reinsurance—to set a cap on the most they are willing to pay out in claims from a major loss event. When losses burn through this maximum, insurers pay losses up to its maximum limit (the retention), and the rest is ceded to reinsurers. Without reinsurance, insurers’ face existential threats from catastrophes such as Ian, so they transfer a portion of their risk to the reinsurance industry to protect their capital base. Insurance, at its heart, is the management and assessment of risk, and reinsurance allows insurers to measure and account for more of it.

In locations where there is a significant risk of natural catastrophe loss, such as in Florida, insurers buy more reinsurance protection. The Florida insurance market is unique in that many of its insurers are small-to-medium-sized insurers based in the state that plug the gap left by national insurers who limit their Florida business because of the state’s outsized risk. These Florida-only or Florida-mainly insurers are called “take-out companies” because they were established to take business away from the state-run insurer, Citizens Property Insurance Corporation (Citizens), which is the insurer of last resort. This means that if an individual cannot get insurance from any other Florida insurers, Citizens is their final option.

The average Florida take-out insurer cedes close to two-thirds of its premium and risk to reinsurers. This means that Florida insurers are very heavily dependent on availability of reinsurance. If the supply of reinsurance shrinks, or prices increase, insurers have to account for that market change, often meaning that homeowners must pay more for property insurance.

Additionally, reinsurers are careful not to bear too much Florida risk. Individual reinsurers will only take on a small portion of an insurer’s risk, requiring insurers to cede risk to multiple reinsurers. For example, the Florida take-out insurer American Integrity, which writes less than a half billion dollars of premium, cedes business to 41 reinsurers.

Reinsurers grow skittish

In the aftermath of Hurricane Ian, Swiss Re, one of the world’s largest reinsurers, is cutting back on its Florida exposure, raising rates and paying less commission to its insurer partners. Because the reinsurance market is largely driven by supply and demand, a drop in the supply of reinsurance capacity at the same time that demand for reinsurance grows is a formula for inexorably higher rates, passed on to insurers—and passed on in turn to insurance buyers or homeowners seeing premium increases.

Another reinsurance development contributing to scarcer and more expensive insurance premiums is the damage Ian caused to the Florida Hurricane Catastrophe Fund (FHCF). The FHCF was created in November 1993 during a special legislative session a year after Hurricane Andrew. Its purpose is to serve as an additional source of reinsurance capacity for Florida insurers. The FHCF is one of the largest reinsurance partners for Florida insurers. At year end 2021, the FHCF had a fund balance of approximately $11.3 billion. If Ian’s losses prove sufficient enough to wipe out the FHCF’s limits—which they may be according to a recent insurance industry analyst‘s report—Florida insurers will be hard put next year to find the reinsurance capacity they so desperately need. This means that when the next catastrophe hits the state, further crisis in the insurance market will follow, increasing rates, collapsing insurers and worse.

When reinsurers buy reinsurance

Even reinsurers need reinsurance protection to avoid too much risk accumulation at any one location. Reinsurance for reinsurance companies is called retrocessional reinsurance. One of the largest providers of retrocessional reinsurance is Berkshire Hathaway’s National Indemnity Group. The Berkshire company is cutting back renewing its retrocessional business with its reinsurance clients. If reinsurers cannot replace this lost capacity elsewhere, the decline in retrocessional capacity supply from one of the largest providers will mean reinsurers may bear more risk, and raise their rates—with the increase reflected in higher homeowner insurance premiums.

Some good news

The bleak landscape of the Florida insurance market, with rising costs for consumers, potential insolvencies at some take-out companies and evaporating reinsurance capacity, also features some bright spots. First, the industry is sufficiently capitalized to absorb a $60 billion loss. What is more, two government insurance providers, state-run Citizens and the federal National Flood Insurance Program (NFIP), have prudently purchased sufficient reinsurance to protect their balance sheets. Citizens is expected to pay out approximately $2.5 billion in Ian claims. It has over $7 billion in capital, so its balance sheet can sustain the loss payments. After first dipping its toe in the reinsurance markets several years ago, the NFIP now secures significant reinsurance capacity from the traditional reinsurance market as well as from the insurance linked security (cat bond) market.

Litigation, not insurance, drives Florida’s insurance woes

There is one way to offset the inevitable rise in Florida homeowner’s insurance rates caused by higher reinsurance costs. The answer is a head-on attack at the root cause of Florida’s insurance woes – excessive litigation. Florida’s insurance woes stem from a man-made crisis rooted in excessive, unjustified litigation. Florida’s broken insurance market is caused by a liability crisis. Uniquely in the United States, Florida is home to excessive volumes of homeowner insurance litigation, so much so that although Florida has 9 percent of the nation’s homeowner insurance claims, it has 79 percent of the nation’s homeowner insurance litigation. Insurance risk modeling firm Karen Clark & Company estimates that over a quarter or more of Ian losses will be litigation-related.

Florida must address this crisis once and for all to strip out the unnecessary load from unjustified litigation. To do this, it must enforce the reforms enacted in this spring’s special legislative session and put an end to contractors and attorneys engaging in unscrupulous practices and unjustified litigation. With reinsurance market forces driving higher rates, the only way to restore affordable premiums is to end the state’s out-of-control litigation. Reinsurance supply and demand factors will be a headwind for insurance rates. But if the liability epidemic is addressed once and for all, it can be a tailwind to counter the impact of costlier reinsurance.

Jerry Theodorou is director of the Finance, Insurance and Trade Policy Program at R Street Institute, a think tank. He develops free-market public policy solutions to complex issues where federal and state governments have intervened. Prior to R Street, he was a director in insurance research at Conning in Hartford, Connecticut.

The Florida Housing Finance Corp. is providing $5 million to help low- to moderate-income families and individuals in six counties hit by Hurricane Ian to pay their homeowners’ property insurance deductibles, Gov. Ron DeSantis announced.

The corporation serves as the state’s housing finance agency and receives state funding for the State Housing Initiatives Partnership, known as the SHIP program. Some $5 million is set aside to be used in natural disasters and that money will now be allocated to homeowners in Charlotte, Collier, DeSoto, Hardee, Lee and Sarasota counties in southwest Florida, the governor said in a statement posted Saturday.

“Following the impacts of Hurricane Ian, it was really important to us to make sure people were able to get back into their homes and rebuild as quickly as possible – today’s announcement will help do just that,” DeSantis said. “We know a lot of homeowners had coverage for the storm, however, insurance deductibles are expensive and often a gap not covered by other support.”

As of late last week, almost 400,000 property owners in those six counties have filed insurance claims since Hurricane Ian made landfall on Sept. 28, according to the Florida Office of Insurance Regulation. The office did not show the average homeowners’ deductible for those areas, but the amount has likely increased for many in recent years as a number of insurers have raised premiums and insureds have sought ways to save money.

Hurricane deductibles can be much higher, and a burden on some families struggling to rebuild after Ian, said Trey Price, executive director of the Florida Housing Finance Corp.

Price

Residents in the six counties can apply through their county housing offices. A link to the insurance deductible program was not shown on the housing corporation website, but the press secretary for the housing corporation said that staff was meeting with local offices in each county this week to streamline the application process.

Links to the corporation’s other housing programs’ income eligibility guidelines may give an idea of who can qualify. In the Fort Myers/Cape Coral area, a family of four with “very low income” would need to have no more than $40,200 in annual income to qualify for a home investment program, for example, the site shows.

Top photo: Fort Myers Beach a few days after Ian. (AP Photo/Alex Menendez)

NEWYou can now listen to Insurance Journal articles!

Listen to this article

0:00 / 5:261X

Hurricane Ian made landfall in southwest Florida at the worst possible time for many in the agricultural community, cutting a path through the heart of Florida’s citrus belt and smashing tomato fields just before the start of seasonal harvests.

Ian impacted 375,300 acres of citrus groves — nearly every acre where oranges are grown in Florida — and 153,638 acres of vegetable and melon crops, among others, Christa Court, a University of Florida economist, said in a Zoom press conference last week.

Ian’s damage to Florida’s $8.1 billion agricultural sector is estimated at between $787 million and $1.56 billion, University of Florida economists said.

Damage estimates by county won’t be available until mid-November, but those in Manatee County’s agricultural community say local damage is significant.

“We took a big hit,” Gary Reeder, president of the Manatee County Farm Bureau, said this week of the tomato, watermelon and citrus crops as well as Dakin Dairy, which lost more than 200 head of cattle and suffered significant structural damage.

The Myakka City community rallied around Dakin Dairy with chainsaws and other equipment after the storm to aid recovery efforts.

“We are slowly regaining our footing and we are milking again, delivering milk again and we have fresh milk in the market. As we recover, regroup and restructure, keep checking back with us. We feel so fortunate to be part of this community,” Courtney Dakin posted recently on the dairy’s Facebook page.

The Citrus Crop

Although Manatee County is not one of Florida’s top citrus growing counties, it is home to juice maker Tropicana.

Manatee County has an estimated 12,807 acres of citrus and most of it, like 90% of the Florida orange crop, goes into juice production.

Nearby Polk, Highlands, DeSoto and Hendry counties all have far larger citrus crops.

Florida’s citrus crop has been declining for decades because of diseases, such as greening and canker. Greening, also known as Huanglongbing disease, is a bacterium that kills the tree and is spread by a tiny insect, the Asian Citrus Psyllid.

Tropicana has been turning increasingly to imports, and the company earlier this year stopped processing OJ at its Fort Pierce plant, consolidating that function in Bradenton.

SeaPort Manatee saw 520,212 tons — or nearly 125 million gallons — of fruit juice imports in the latest 12-month period, up 14% from a year earlier.

“There is a tremendous amount of fruit on the ground,” Reeder said of Manatee County groves.

Higher Priced Tomatoes

Bob Spencer, president of West Coast Tomato in Palmetto, said he expects his crop will be down 50% because of Ian.

Damage to Manatee County’s tomato crop, historically the largest in Florida, will have an impact on consumers with higher prices likely.

Much of Manatee County’s tomato crop goes to food services, such as cafeterias and fast food restaurants in the eastern United States, and retail stores.

West Coast Tomatoes was planning to start its first harvest Thursday, and some of the crop may show evidence of wind burn, which won’t affect the taste, Spencer said.

“You will see higher prices in the stores because of this,” Spencer said.

Jones Potato Farm was more fortunate. “We had to replant about 20 aces of green beans in Parrish,” Leslie Jones said.

“We just started planing potatoes. We feel really blessed.”

Horticulture

Dennis Cathcart, owner of Tropiflora, 3530 Tallevast Road, and Ralph Garrison, owner of Suncoast Nursery, 6012 18th Ave. E., have both been in the nursery business for decades.

They say the damage from Ian is the worst they have seen from any storm.

“It’s a vast amount of damage. Seven greenhouse structures were destroyed and about all of the others were damaged,” Cathcart said of his operation specializing in bromeliads.

The plants are essentially OK, but its difficult reaching them because of damage to structures on the property.

“Our irrigation system got shredded, too,” Cathcart said.

“We have had hurricane damage a number of times with Charlie, Irma and others, but nothing like now. This is worse than all of the damage we have had over the years,” he said.

Tropiflora’s bromeliads go to collections at botanical parks and zoos around the world, including Garden by the Bay in Singapore, he said.

Suncoast Nursery’s Garrison says that what happened at his business sums up the life of a farmer.

Like Cathcart, Garrison said he has never seen so much damage from a single storm.

“Not this much, no sir. This is about a $1.6 million loss,” he said. “It’s frustrating. I don’t know if at this age and day if I will rebuild or not.”

Compounding the challenge is the sharply higher cost of replacement materials and the labor shortage.

Cattle

Jim Strickland, past president of the Florida Cattlemen’s Association, owner of Strickland Ranch and manager of Blackbeard’s Ranch, had one word for the aftermath of Ian: “fences.”

“My crew has been working around the clock,” mending fences, he said. “It’s been hard work, it’s been wet. If I told you we had 1,000 trees on fences, I would not be lying.

“We have all the chain saws and swamp buggies and are ready to go,” he said, adding that his biggest worry is that cattle might wander onto roads, posing a danger to drivers.

“As soon as I saw my family and friends were safe after Ian, we began working on fences,” he said.

Some of that help came from outside the Bradenton area, including shipments of fence posts and wire, and several cowboys from North Carolina, he said.

Photo: Dennis Cathcart, founder of Tropiflora, a major grower of bromeliads, and his heavily damaged grow-houses in Sarasota, Florida. (Tiffany Tompkins/The Bradenton Herald via AP)

Copyright 2022 Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

Florida’s besieged property insurance industry is hoping the second time will be the charm, after Gov. Ron DeSantis announced that he is working with lawmakers to schedule another special session to help stablilize the market.

The governor’s office did not provide details or a copy of an executive order calling the session, but at an event in hurricane-ravaged southwest Florida, the governor said lawmakers could convene after the Nov. 8 election and before the end of the year, according to news reports. House and Senate leaders and insurance industry activists indicated they are ready to tackle issues facing an insurance industry that has seen six insurers become insolvent this year while others have raised premiums significantly.

“We support it. We’re hoping to see more legal reforms, especially on one-way attorney fees,” said Michael Carlson, lobbyist and president of the Personal Insurance Federation of Florida, which represents a number of carriers.

DeSantis at a news conference before Ian made landfall. (Alicia Devine/Tallahassee Democrat via AP)

A special session held in May approved two measures that aimed to reduce claims litigation, bar plaintiffs’ attorney fees in assignment-of-benefits claims, provide insurers with a layer of state-provided reinsurance, and allow policies to pay only for roof repairs, not full replacement, in many cases.

But insurance executives and advocates have said much more is needed to stabilize a market that appears to be overwhelmed with litigation and soaring reinsurance costs. DeSantis said Thursday that he wanted some further steps in Mayt that the Legislature as not willing to go along with, according to Politico, a news site.

Several ideas have been discussed in the industry for the upcoming special session, including:

AOBs. Revising state law to allow insurance policies that bar assignment of benefits agreements. Florida’s chief financial officer, Jimmy Patronis, on Wednesday – the day before DeSantis announced the special session plans – proposed an outright ban on AOBs. But it wasn’t clear Friday if DeSantis and legislative leaders are on board with that for a special session. It’s also not clear if such a ban would stand court scrutiny, Carlson said, since Florida law has long allowed people to assign contracts.

Cat fund. Lowering the retention level, or deductible, that Florida insured losses must reach before insurers can access the Florida Hurricane Catastrophe Fund. The state-created fund provides less-expensive reinsurance after major hurricanes, but accessing it sooner could save some carriers millions of dollars on their reinsurance tab, advocates of the idea have said. Providing another layer of state-backed reinsurance, at reduced premiums, also has been kicked around.

Attorney fees. At the heart of Florida’s insurance crisis, many insurers have said, are Florida statutes that allow claimants’ attorneys to win large fees when they prevail in litigation, even if fees are much more than the judgment award or settlement. The May special session banned plaintiffs’ attorney fees but only in AOB cases.

Industry insiders and company leaders have said waiting until the 2023 regular session of the Legislature to make reforms will be too late and would not give insurers relief before the reinsurance renewal deadlines next summer. Reinsurance prices spiked this year and are expected to rise again.

Whatever measures the Legislature considers to rescue the property insurance industry, those must be accompanied with some type of short-term relief for homeowners, many of whom have seen premiums double or triple in the last two years, some insurance advocates have said.

Carlson and others have said that Hurricane Ian, which raked across the state Sept. 28 and Sept. 29, may have provided the final straw needed to prompt state leaders to consider another session and take broader measures. Patronis, insurance agents and policyholders have reported that the hard-hit Fort Myers area has been flooded with public adjusters, plaintiff attorney advertisements, and contractors hoping to benefit from property owners filing insurance claims.

As of Thursday, Oct. 20, the Florida Office of Insurance Regulation reported that 564,399 insurance claims had been filed from Hurricane Ian, with estimated insured losses so far reaching more than $6.6 billion.

The call for a special session also came a week after Democratic gubernatorial candidate Charlie Crist blasted DeSantis for not fully addressing the crisis and allowing premiums to soar.

“No one believes that Ron will finally do the right thing and fix his broken insurance market in his last month in office,” Crist said in a press release, according to Politico.