Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Early Estimates Put Idalia’s Insured Losses at $3-9 Billion for Florida

Preliminary estimates of insured losses from Hurricane Idalia have already begun, with about $9 billion in losses predicted for Florida alone.

The estimates are far lower than some in Florida had feared and well below the $60 billion in losses from Hurricane Ian, which followed a similar path less than a year ago but targeted more heavily populated areas on Florida’s southwest coast.

UBS, the multinational investment bank, said Wednesday that its estimates for Florida range from $4 billion to $25.6 billion, with an average of $9.36 billion, Reuters news service reported. That would mean Idalia would cost insurers less than 10 of the costliest hurricanes to hit the United States.

BMS, the reinsurance brokerage, pegged losses at $3 billion to $6 billion. “This is not the devastating event that was feared even 24 hours ago,” the company said in a web posting Wednesday evening.

AccuWeather, a global forecast service, said that total damage and economic losses for the Southeastern states hit by Idalia would be in the $18 billion to $20 billion range.

“To put this event into context … Hurricane Ian last year, impacting a much more densely populated area, brought total damage and economic loss of $180-210 billion,” AccuWeather said in a bulletin. “Hurricane Michael in 2018 devastated parts of the Panhandle area of Florida, again in a slightly more populated area than Idalia, with a total damage and economic loss of about $30 billion.”

Idalia made landfall Wednesday morning as a Category 3 hurricane in Florida’s Big Bend area, a low-lying area with no large cities. The storm spared the Tampa metro area, with more than 3 million people, from the worst of the wind and surge.

Still, the hurricane came at a shaky moment for the insurance industry, just as four new property-casualty insurers have entered the long-distressed Florida market. The CEO of one of those carriers, Orion180 Insurance, said Idalia has not changed his company’s plans for Florida.

“No, and we feel this is something the market can absorb,” Orion180 Insurance CEO Ken Gregg said Wednesday.

Orion180 is based in Florida but does not yet have policies in the state. Its main book of business is in South Carolina, where a diminished Idalia blew through early Thursday. Gregg said the estimated losses there appeared to be manageable and covered by reinsurance. “It’s within our retention,” he said.

He worried that insurers that do write in the affected part of Florida, including the state-created Citizens Property Insurance Corp., will feel some pain. Many structures in the Big Bend area are older and have not been elevated or built to the stronger construction codes now required in south Florida.

Officials with one of the largest carriers in the affected part of Florida, Security First Insurance, said the damage, so far, appeared to be much lighter than expected.

“We sort of feel like the Maytag repairman: The phone’s not ringing off the hook,” said Melissa Burt DeVriese, president of Security First.

She said the carrier has seen 152 claims, including 21 homes in Taylor County with severe damage and a few in Pasco County. Damage has come from fallen trees, roof shingles ripped off, and flooding. Independent adjusters for Security First have reported that losses may be about 50% of what they had expected, DeVriese said.

For Citizens, it was too early to venture an estimate Thursday morning. “We’re fortunate that it hit an area that was not densely populated,” spokesman Michael Peltier said.

Reinsurers may see the insured losses from Idalia as a reason to raise prices yet again, which could lead to Florida P/C insurers seeking another round of rate increases for their insureds.

“Historically, what happens when you have these hurricanes is that everyone gets worried about the liability following the hurricane,” said Thomas Hayes, chairman and managing member of Great Hill Capital LLC in New York, adding that insurers typically end up being able to raise prices after such events, Reuters reported.

Nationally, U.S. reinsurance rates for policies that had claims for natural catastrophes rose 30%-50% during July renewals, while in Florida the increase was 30%-40%, reinsurance broker Gallagher Re said in July.

Much of the impact from Idalia will likely be from flooding, after the storm produced a storm surge on Florida’s coast of more than 8 feet.

A City of Tallahassee electrical worker assesses damage to power lines on Wednesday. (AP Photo/Phil Sears)

“We see tremendous flooding in the Big Bend region along with many trees and power lines down. It could take weeks for some parts of Florida to get power back after this devastating storm,” AccuWeather’s chief meteorologist, Jonathan Porter, said in a statement.

Cedar Key, Florida, near the eyewall, looked “apocalyptic” after the storm. City Hall took on eight feet of water, news outlets reported. In Perry, Florida, winds broke store windows, tore siding off buildings and knocked over a gas station canopy, the Associated Press and others reported.

In Steinhatchee, Florida, businesses and houses were swallowed up by water from Deadman’s Bay. In Charleston, South Carolina, the surge swelled over a seawall and sent several inches of water into the streets, AP noted.

Idalia, like Hurricane Ian and other storms, has highlighted the huge flood insurance gap in coastal areas.

The share of federally flood-insured properties in Taylor County, Florida, where the storm made landfall, is only 5.4%. In Hillsborough County, home to Tampa, it’s 20%, Bloomberg reported. But that still leaves four out of five properties unprotected. Only 18% of Floridians have flood insurance, according to the Insurance Information Institute.

That flood insurance gap is closing, if only slightly. The Florida Legislature last year required most insureds with state-run Citizens Property Insurance Corp. to also purchase flood coverage, but that requirement does not fully phase-in until 2027.

Top photo: Tampa Fire Rescue Department members remove a street pole after a large awning from an apartment building blew off Wednesday. (AP Photo/Chris O’Meara)

Reuters, Bloomberg and Associated Press news services contributed to this report.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Just when parts of the property-casualty industry thought it was safe to re-enter the Florida market, Hurricane Idalia made landfall closer to the heavily-populated Tallahassee area than expected and brought heavy storm surge to the Big Bend coastline.

Idalia made landfall as a Category 3 storm about 8 a.m. Eastern time Wednesday, with the eye of the storm near Keaton Beach, about 75 miles southeast of Tallahassee. Even if the strongest winds do not make a direct hit on the state capital, residents there feared that Tallahassee’s famous tree-lined streets will mean downed limbs, widespread roof damage and power outages.

“Tallahassee has so many trees, we’re bound to get some damage,” said David McKee, owner of the McKee Insurance Agency, which also has policyholders all across the most vulnerable parts of the low-lying coastal areas along Apalachee Bay, southeast of Tallahassee.

A CNN meteorologist warned that thousands of trees could fall, from north Florida across southeast Georgia. NBC News reported that a motorist in Pasco County, near Tampa, was killed in an weather-related accident. Businesses in downtown Tarpon Springs saw at least two feet of storm surge, Bloomberg News reported.

Another major loss for Florida’s insurers would come at a crucial moment for the industry – less than a year after Hurricane Ian caused $60 billion in insured losses and after 10 insurer insolvencies in the last 30 months. But the storm also comes just as state legislative reforms appear to be having a desired effect on litigation and loss adjustment expenses. Four new p/c carriers have been approved to do business in Florida in the last two months, providing a ray of sunshine for the state.

At least one industry veteran believes the revamped Florida market can now withstand another powerful blow.

“The legislative changes put in place since Hurricane Ian have strengthened Florida’s insurance industry and, notwithstanding the last five years of unprecedented losses, companies are in a stronger position to cope with a major storm,” said Fred Karlinsky, co-chair of the Greenberg Traurig insurance and regulatory law firm’s Global Insurance Regulatory and Transactions Practice Group.

Still, even with the legislative changes, heavy losses from Idalia will likely result in further rate increase filings by at least a few insurers in coming months. And some insurance advocates are concerned that insureds could also be hit with a surcharge later this year if Idalia forces Florida’s Citizens Property Insurance Corp. to burn through the surplus in its Personal Lines Account.

Citizens, created to be an insurer of last resort but now the largest carrier in Florida, has a large share of policies in the 10-county area that could be most affected by the storm – more than 16,000, according to first-quarter 2023 data from state regulators. The insurer now holds a surplus of just $420 million in its Personal Lines Account, one of three accounts set up by statute.

“If losses exceed the $420 million in that account, then, yes, that would result in an assessment,” said Michael Peltier, spokesman for Citizens.

An emergency assessment on Citizens policyholders could add 10% to premiums.

The account’s surplus is at that level due to rapid growth of policies in recent months and heavy losses from Hurricane Ian and other storm events, Peltier said.

But breaching the surplus appeared to be less than likely as of Wednesday morning. A look at Hurricane Ian gives a rough idea of claims and costs that Citizens could see from Idalia:

Ian, which struck the Fort Myers area in late September 2022, resulted in 68,000 claims by Citizens policyholders and caused an estimated $3.8 billion in losses, including litigation and loss adjustment expenses. The average Ian Citizens claim, with expenses, was more than $55,000. With the recent legislative reforms, the volume and cost of claims litigation is expected to drop significantly. And the area hit by Idalia holds fewer policyholders.

So, even if 10,000 Citizens claims were filed from Idalia, at an average of $30,000 each, that would be below the Personal Lines Account surplus level.

“It’s really premature to compare Idalia to Ian, and may not ever be a fair comparison,” Peltier said Tuesday.

The Florida Legislature earlier this year allowed Citizens to combine its three accounts into one, to provide more flexibility with surplus. But that move won’t be made until January.

Other insurers with policyholders in the Hurricane Idalia zone include American Bankers, with more than 6,000 tenant policies in force in the most-populous county of Leon, home to Tallahassee; Cypress Property & Casualty, with some 2,400 tenant policies in Leon County; Nationwide Mutual Insurance, with 4,200 homeowner policies in Leon County; and American Modern Insurance, with 1,200 tenant policies in the county.

Some insurers’ information is considered a trade secret and is not reported by Florida’s Office of Insurance Regulation, so some major insurers are not included in the OIR’s quarterly report.

Meanwhile, news reports from the epicenter of Idalia showed heavy storm surge, flooding, and winds reaching 110 mph. The Steinhatchee River rose 7 feet in one hour, putting it above flood stage, the National Weather Service reported. The storm had reached Category 4 earlier but weakened slightly before making landfall, Bloomberg News Service reported. Tornado watches were posted for parts of the state and into Georgia.

More than 140,000 homes and businesses were without power in Florida on Wednesday, according to data from PowerOutage.us. The utility with the most outages was Duke Energy with more than 40,000 customers without power, followed by Florida Power & Light Co. at more than 16,000, Reuters news service reported.

Tampa Electric on Tuesday said about 3,000 people, including line crews, tree trimmers and damage assessors, are traveling to Florida to help restore power after the storm passes.

Top photo: Reporters wade through floodwaters in Tarpon Springs, Florida, after Hurricane Idalia passed offshore early Wednesday morning. (Joe Raedle/Getty Images North America/Bloomberg)

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Florida property insurers were keeping their fingers crossed Tuesday as the latest projections indicated that the worst of Hurricane Idalia may miss some of the most heavily populated parts of the state’s west coast.

The National Hurricane Center predicted the eyewall of the Category 3 storm would push into the lightly populated Big Bend area, perhaps between Cedar Key and Crawfordville. But storm surge was expected in a wider area, bringing flooding to coastal areas as far south as Tampa Bay, according to weather service and news reports.

Citizens Property Insurance Corp. is likely to be the insurer most impacted. Data from the Florida Office of Insurance Regulation show that Citizens writes some 3,400 policies in the three coastal counties that appear likely to take the brunt of the wind and waves: Taylor, Dixie and Levy. That’s more than 30% of the total coverage in that area, but a small number compared to the thousands of policies affected by Hurricane Ian in southwest Florida a year ago. The percentage is estimated: some insurers do not report their policy totals by county, calling it a trade secret.

Citizens suspended new policy binding, statewide, as of late Sunday.

A St. Petersburg, Florida, resident boards up a doorway ahead of Idalia. (Juan Manuel Barrero Bueno/Bloomberg)

“Agents may not bind applications for new coverage or policy changes for increased coverage, regardless of effective date, when a tropical storm or hurricane watch or warning has been issued by the National Weather Service for any part of the State of Florida,” reads the agent bulletin posted Sunday.

The OIR also issued a bulletin, urging insurance companies to be ready for claims and to follow their claims manuals and industry best practices.

“Insurers are encouraged to use all available resources to effectively facilitate the claims process for consumers,” reads the memo. Those methods may include photographs of damage, videos, video conferencing between adjusters and policyholders, the use of drones and remotely operated vehicles.

Policyholders may also use video and photos to assist in claims. Florida’s chief financial officer on Monday urged insureds in the path of the storm to photograph and video their homes before and after damage occurs. Insurers should respond to policyholder needs and maintain complete records, OIR said. The office may issue fines of up to $25,000 per each violation of the Florida Insurance Code.

“We’re prepared,” said Melissa Burt DeVriese, president of Security First Insurance, which had about 144,000 policies in force across Florida.

She noted that the carrier has shed more than 200,000 policies in recent years in Florida but has added employees and has 38 adjusters ready to inspect properties in affected areas. It also has contracts with independent adjuster firms.

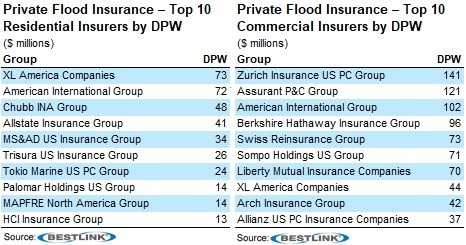

Meanwhile, the number of private flood insurance companies has been growing in recent years and could feel some impact from storm surge and inland flooding.

“Flood insurance is a very concentrated market, with a limited number of insurers covering most of the insureds,” reads a report released this week from the AM Best financial rating firm said. “However, the number of private companies writing coverage has increased substantially, from 47 in 2016 to 198 in 2022.”

Recent rate increases for many properties, the result of FEMA’s new Risk Rating 2.0, should push more residents into the private flood coverage, AM Best said.

A look at Idalia’s path so far gives an idea of its potential destruction. Heavy rainfall in western Cuba could produce flooding and landslides, forecasters said, and hurricane-force winds were expected late Monday.

Idalia was expected to move northward Monday, then turn north-northeast on Tuesday and Wednesday and move at a faster pace. The center was forecast to pass over the extreme southeastern Gulf of Mexico by early Tuesday, and reach Florida’s western coast on Wednesday.

Along a vast stretch of Florida`s west coast, up to 11 feet (3.4 meters) of ocean water could surge on shore, raising fears of destructive flooding.

Large parts of the western coast of Florida are at risk of seawater surging onto land and flooding communities when a tropical storm or hurricane approaches. That part of Florida is very vulnerable to storm surges, Jamie Rhome, deputy director of the National Hurricane Center, said Sunday.

“So it will not take a strong system or a direct hit to produce significant storm surge,” he said.

In Cedar Key, a fishing village that juts out into the Gulf of Mexico, a storm surge is among the greatest concerns, said Capt. A.J. Brown, a fishing guide who operates A.J. Brown Charters. The concern is that if the storm strikes Florida just to the north, Cedar Key would get the powerful surge that comes from being on the southeastern side of the storm.

There are worries in Cedar Key about a storm surge, Brown said. If it reaches five feet (1.5 meters) “it would cover most everything downtown.”

Mexico’s National Meteorological Service on Sunday warned of intense to torrential rains showering the Yucatan Peninsula, with winds as fast as 55 mph (89 kph).

Florida has mobilized 1,100 National Guard members, and “they have at their disposal 2,400 high-water vehicles, as well as 12 aircraft that can be used for rescue and recovery efforts,” said Gov. Ron DeSantis, the Republican governor who is a candidate for the GOP presidential nomination.

“If you are in the path of this storm, you should expect power outages,” he added.

Update: This story has been corrected to show the correct number of in-house field adjusters at Security First Insurance.

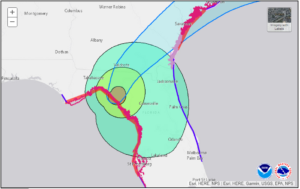

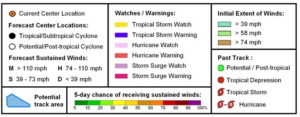

Map at top: Idalia’s projected path, as of Tuesday morning. (NOAA)

Copyright 2023 Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Health insurance. Dental insurance. Accidental death and dismemberment. Why not homeowners insurance as an employee benefit?

That’s exactly what Darren Wood is thinking.

Wood is the founder and chief product officer at Recoop Disaster Insurance, which is now in 42 states and offers a type of parametric homeowners coverage, up $25,000 per policy. Recoop, based in Iowa, announced this month that it is now doing business in Florida and most states, underwritten by Professional Solutions Insurance Co. (PSIC). Recoop’s entrance into the Florida market, along with four new carriers in recent weeks, has given some hope to a state that has been battered by insurer insolvencies, limits on new business, and soaring premiums.

Recoop is, at this point, a general agent of PSIC, a wholly owned subsidiary of NCMIC Insurance Co. which began as a malpractice insurer for chiropractors but now offers personal lines and business coverage.

To find out more about the company and the product, which is designed to cover even some of the losses from storm surge, Insurance Journal sat down for an interview with Wood. Previously with Marsh and with Holmes Murphy & Associates, Wood said he has been working on the parametric idea for a number of years, as a product that major U.S. employers can offer their remote workers, especially those in disaster-prone states where HO premiums and deductibles have risen dramatically in the last half-decade.

Wood’s comments have been lightly edited for brevity and clarity.

IJ:Why is Recoop moving into Florida now?

One of the things goes back to our overall distribution approach. With the top 15 carriers spending roughly $1 billion a year on advertising, that is not something we could compete with. So we made the decision early on, due in large part to my past work experience, that the focus was going to be on distributing the product through the employee benefits space and through associations.

Wood (Linkedin)

I spent nine years with Marsh Consumer, which is now under the Mercer umbrella. Our primary customers were Fortune 1000 employers, and we brought voluntary benefits programs to the table for them as well as the large associations out there, offering the product as a member benefit. From that standpoint, the brokers and distributors in those spaces are the ones responsible for distributing and marketing the program.

Why Florida, why now? Well, given the brokers we deal with and their customers, most of them, the employers have national employee bases. So it’s really a must for them that we have to be in all 50 states. And that’s more on the association side. We have a lot of large associations queued up but we can’t roll out to them at all until we get all 50 states, plus DC.

IJ: So brokers are actually offering Recoop as an employee benefit now?

They are. Predominantly on a voluntary basis. But also, we have seen a couple of firms realize, in today’s environment, that it had appeal and they were going to buy it for their employees as an employer-paid product. Again, we’re just kind of on the tip of that. We have two that have adopted that and we have several others, much larger, that are considering doing that. One of the primary drivers there is the workforce moving to a hybrid work environment. Really, working from home, that’s their office, so if a family is displaced from their home, they can’t get up and running, so it’s not a viable employee contributing to the workforce.

So, this gives them ability to help out with their disaster risk-mitigation plan.

I can’t give names now. But one is a smaller employer, under 500 employees. The other is offering it just to hybrid employees. One association is very large, transportation-related.

IJ: Can you say how many policies you have now, nationwide?

We went live 9/1 of last year. And given our target being employers, that was right when their open enrollment season starts. And they typically make the buy-ins for that in March, April. So we missed that window for the most part. Right now, we are between 500 and 600 policies. This year, we were in place in 42 states, including DC, with Florida being the latest. We have a host of large employers queued up, and roughly about 700,000 eligible employees that will have the opportunity to enroll this fall.

We’re really starting to make some traction. And, quite frankly, for them, Florida was the key. They have employees in Florida and in order to be able to offer it, they’re not going to offer something to only a portion of their population. We got California before that, so those two states really made a material difference in the amount of employers we could add.

IJ: Can you give an idea of the cost, the premiums for this type of coverage?

We anticipate, across the country, our average coverage amount is going to be approximately $10,000. We offer in $5,000 increments. And interestingly, the enrollees have taken an inverted bell curve on this, where $5,000 was the most common and $25,000 was the second-most common amount of coverage selected. So, with that, our average premium across the country we expect to be $440, per year.

To equate that on the benefits spectrum, accidental death and dismemberment typically ranges about $60 to $80 a year. And the average home insurance is about $1,400 a year, across the country, although I know it’s materially different in Florida. In some lower-risk areas, our product is as cheap as $125 for a $1,000 policy. In Florida, we have three zones, it ranges from $240 for $5,000 in coverage, to $360 for a $5,000 policy. For the very expensive, high-dollar, high-risk areas of Florida, it becomes much higher, about $1,000 for a $5,000 policy.

It was important when I built the product to make it affordable for families, especially for families making less than $150,000 a year. Over the last 15 years, about 78% of the disaster declarations in the country have been in low- and moderate-risk areas. Disasters are happening everywhere and with those brokers and those employers, we get to sell a lot of policies because of moderate-risk areas, which allows us to serve some of the higher-risk areas like Florida, the Gulf Coast, the Atlantic Seaboard.

IJ: I think a lot of people in Florida, with HO premiums going up and up and up, have opted for very big deductibles, so it sounds like this product could help with that cost.

You’re spot-on. And that’s one of the things we recognized early on, especially with single-peril catastrophe policies, which often have deductibles that are between 5% and 30% of the value of the home. It has been reported that roughly 60% of the population does not have an emergency fund and the same number of people have to borrow for an expense over $400. And when you see most insurers starting to treat roofs on an actual-cash-value basis, and if you’ve got a roof that’s 10 years old with a 20-year life span that costs 10 grand, you’re on the hook for 5 grand. And you stack the deductible on top of that.

Over the last 4-5 years, with the number of hurricanes that hit Florida, between 65% and 85% of the damage has been not covered by insurance, predominantly because it’s storm-surge related. That’s one of the things we cover with our product is storm surge (but we don’t cover freshwater flooding). Storm surge was an important piece for us. And insurers in a lot of cases don’t cover storm surge.

IJ: And lots of people don’t have flood insuranceto cover it.

Exactly. For a lot of people [hit by storm surge], their primary tool is still loans through the U.S. Small Business Administration. So would you rather have a $25,000 loan that you’re paying at 4% interest that costs $200 to $300 a month, or buying a policy that has a $320 annual premium?

IJ: Do you have adjusters?

To explain: In all but about four states, it’s required that the insured has to have an underlying home or renters’ policy. We use that as proof of insurability, trying to keep the cost down, so we don’t have to send somebody out. We are, for all intents and purposes, a guaranteed-issue policy. As long as you have that underlying policy and you do not live in a mobile or manufactured home, which our reinsurer said was a no-go, we will issue you a policy. We don’t look at the structure of the house.

The criteria for filing a claim are: 1.) That your’re in a state- or federally declared disater area; 2.) You have $1,000 in damage from one of our covered perils; and 3.) You have that underlying home policy. In the claim packet, we ask people to provide pictures. We ask that they provide a couple of pictures ahead of time, so we have a baseline, so that post-event, if you send a picture of the damage, we’ve got the ability to compare and contrast.

And we use Sedgwick, the largest claims administrator in the country, as claims provider. And they believe they can adjudicate 98% of the claims remotely, which really helps on the speed side. So all of those factors help us keep the pricing down.

In Florida, we had to deviate a little bit from our standard model. We have to adjudicate/adjust for all of the damage that is done. But the way we built that into the policies for Florida, we added what we call an incurred-loss endorsement. But we were also able to include items that were not related to home damage. People can submit lost wages if their business does not reopen (after a loss). If they have lost their job, they can submit expenses associated with health care. If they are not able to live in their house and have to stay in a hotel, you can submit pet boarding. If it’s tied to your exposure and covered peril, we will use that as something we can reimburse for, to get them up to the full coverage amount they’ve elected.

IJ: Do you have any concerns about fraud? I mean, say someone doesn’t have that much damage but might feel that they need a quick $25,000.

With Sedgwick’s experience, they’ve made it clear that they can tell what’s been there already and what is new damage. And that’s one of the reasons we like to have the “before” picture, before a claim is made. We just don’t expect to get a lot of fraud, just because of the nature of the product. If somebody is exposed, either the roof is going to come off, from wind, or it’s from storm surge. And those things leave tell-tale marks. In most states, fraud is not a concern because we stop counting at $1,000. [All the claimant needs to show is at least $1,000 in damage to receive the full, agreed-on coverage amount.] In Florida, we have to adjust and adjudicate for all of the covered amount.

IJ: What is your relationship with Professional Solutions Insurance Co., your underwriter?

Their focus, for most of their early years, was on providing medical malpractice for doctors of chiropractic. They formed a subsidiary to bring additional products to bear to their customer base. In the last 3-4 years they made a conscious decision to expand their footprint and get into other lines. It was a logical fit for us. They had an asset that was underutilized so we partnered with them. They have material surplus in their reserves, so they have the capability and the financial strength to grow with us.

It’s a unique situation. We are the owner of the product but we’re also the general agent at this point in time. The (Florida OIR) approval is of the product. Professional Solutions has to have a certificate of authority. But we have to be licensed in each state, as an agent. The claims agreement is between PSIC and Sedgwick. Eventually we’ll have that moved over to us. At that point in time, we have to have an MGA license. Until then, a general agent license suffices.

IJ: You were with Marsh and Holmes Murphy. How did you decide to get into Recoop?

Great question. This has been my baby for a long time. I formed the company in 2013. For the first eight and a half years, it was me pulling all the pieces together. It was no small feat. What I wanted was to have a package put together that I could bring to a carrier, with distribution partners in place, administration in place, so it was a turn-key solution. We had some close calls with a couple of major carriers that in the end just didn’t work. The catastrophe nature of the product can scare some off.

But about a year and a half ago, I got to add to the team. We decided to run lean to keep our costs down and partner with the best-in-class providers out there. For example, Sedgwick. And we’re dealing with Insurity, which provides policy admin support.

We’ve got five employees. They have good relationships with the top brokers out there. So, the pieces have fit together nicely. Because, frankly, there have not been a lot of new products out there. There’s been some “critical-illness” products where they’ve said they’re going to shuffle the benefits around and slap a new name on it. There have been some new single-peril catastrophe products out there, some on the parametric side, which is good to see. But as far as we know, we are the only multi-peril disaster product in the marketplace that has the model that’s almost like Aflac, but for your home.

Rabb is Southeast Editor for Insurance Journal. He is a long-time newspaper man in the Deep South; also covered workers’ comp insurance issues for a trade publication for a few years.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Farmers Insurance Laying Off 11% of Workforce, Citing Industry Challenges

Farmers Insurance announced it will part ways with approximately 2,400 employees – 11% of its workforce across all lines of business.

“Decisions like these are never easy, and we are committed to doing our best to support those impacted by these changes in the days and weeks to come,” Raul Vargas, president and CEO of Farmers Group, said in a statement Aug. 28.

The Los Angeles-based insurer said the moves are being made to better position itself for long-term profitability by creating a more streamlined organizational structure, and follow a thorough evaluation and reduction of operational expenses across the company.

“Given the existing conditions of the insurance industry and the impact they are having on our business, we need to take decisive actions today to better position Farmers for future success,” Vargas said.

Farmers, one of the country’s largest providers of home, auto, and small business insurance, said it would in the future share details of a plan to “reinvent how insurance is delivered, simplifying systems and introducing innovation” for employees as well as its exclusive and independent agents.

The layoffs come after Farmers has pulled back from Florida and California in recent months.

Farmers said in June it would halt sales of new homeowners policies in Florida, citing higher costs. Last month Farmers advised the Florida Office of Insurance Regulation it would further reduce business in the state by discontinuing Farmers-branded auto, home, and umbrella policies. The pullback could affect as many as 100,000 homeowner, auto and umbrella policies.

Vargas said in a statement that Farmers must manage risk and prudently align its costs as the industry continues to face macroeconomic challenges.

“Our leaner structure will make us more nimble and better able to pursue opportunities for growth and ultimately make Farmers more responsive to the needs of our insured customers and agents,” said Vargas.

Vargas, who took over as CEO at the start of the year, recently ordered workers to return to the office in a hybrid model, reversing the company’s policy on allowing most workers to do their jobs from home. Employees within 50 miles of a Farmers office must come in to work at least three days per week starting in September.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

How Aerial Imagery and AI are Helping Florida’s Insurers with Climate Change and Fraud

Residents of Southeastern states like Florida will be looking ahead to the heart of hurricane season with trepidation. With climate change bringing storms that are wetter, slower and more prone to intensifying rapidly, insurers are struggling to assess risk and underwrite profitably, and customers are struggling to afford skyrocketing premiums. In 2022 across the U.S. there were 18 climate disaster events, including floods, severe storms and wildfires, the third most destructive year ever. Florida, in particular, suffers from hurricanes, with six of the 10 costliest storms in American history hitting the Sunshine State.

Problems have been exacerbated by Florida’s excessive amounts of litigation and claims fraud. In this fraught climate, insurers are managing climate-change risk and reducing fraud by using aerial imagery and artificial intelligence to extract insights about a property’s risk profile, so they are better able to detect fraud and price premiums.

Carriers now have the ability to leverage data from historical imagery while assessing insurance claims, enabling them to detect and prevent fraudulent activities. By analyzing such data, carriers can determine when the damage happened, working out whether it predated the insurance policy or occurred after a natural catastrophe. Additionally, historical imagery data can reveal the extent of the damage and whether a specific event exacerbated the severity. This valuable information helps carriers make accurate assessments and reduces the potential for fraudulent claims.

In the past, insurers used historical trends to assess the risk of a claim, but with erratic weather patterns they are now giving a heavier weighting to information about a property’s location, roof age and condition, flood risk, first-floor elevation, and proximity to vegetation if located in a wildfire risk zone. Across time, they can then start to build up intelligence about trends in different areas to see, for example, whether flood levels have increased.

For years, gaining this information required insurers to send out inspectors to residential or commercial properties. But today, accessing valuable insights is cheap and immediate. Underwriters then have more information to price premiums competitively. They can also proactively reach out to customers, telling them how they can decrease their risk, for example by cutting down overhanging trees close to their property.

One property intelligence phenomena we have seen in recent months is the use of drones to collect detailed data in areas that are difficult for humans to reach. However, drones remain an expensive option as they still require a human operator, meaning this type of data collection is not cost-effective. The real advance that is helping the industry improve their property insights at a massive scale is improvement in aerial imagery from aircraft. Resolution is now so accurate that details at a scale of 7 centimeters can be collected across huge areas. As a result, we are seeing many more insurers use aerial imagery and AI to collect property intelligence. We have grown our own client base by 120 in 2022.

After a disaster has struck, claims processing can be streamlined, with fraudulent claims detected quickly. Rather than relying on individual teams to physically inspect damage to a property, insurers can use aerial imagery or even footage from street cameras to assess post-disaster damages. By using pre and post-disaster imagery, insurers, with the help of AI, can remotely examine the extent of damage to a property and identify exaggerated claims. They can also determine whether damage occurred due to the weather event or if it already existed on the property. For example, insurers can access evidence about roof wear, rust, or whether a tarp was already on the roof indicating pre-existing damage.

In particular, it is advances in AI that have caused a great leap forward, particularly in the field of predictive analytics for underwriting and claims. Because computer vision is able to analyze larger sets of imagery than ever before it is now possible to create and extract new types of attributes that were previously impossible to track. This has meant that suddenly it is possible to view aerial imagery at a large scale. For example, an insurer can now take historical imagery from 20 years back and identify a change like a roof replacement automatically. Doing this manually would be too expensive, but AI makes this level of tracking feasible for the first time.

With every year, imagery analysis becomes quicker and cheaper, meaning insurers can now create data sets that allow them to respond in the most effective way to a natural disaster and allocate resources in the most efficient way.

The challenges facing the insurance industry in the face of climate change are significant. Floridians are facing a projected 40% hike in property insurance premiums this year. At the same time, technological innovations offer some hope. By plugging data gaps using artificial intelligence and aerial imagery, insurers can viably continue protecting Americans from having to foot a life-changing bill post-disaster.

GeoX is a data analyitics company that uses machine vision and deep learning technology to extract information from aerial imagery for insurance companies.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Citizens Property Insurance Corp., Florida’s residual but still-largest property insurer, has posted new information about when and where flood insurance is required for policyholders.

The Florida Legislature last year approved Senate Bill 2A, making big changes to laws governing claims litigation and requiring most Citizens’ policyholders to also obtain flood insurance within three years. The idea, supporters of the bill said, was to help push homeowners back to the primary market and help protect Citizens from legal disputes over wind-versus-water damage.

This year, lawmakers revised the law slightly to exclude policyholders who own condominiums on upper floors.

The bulletin from Citizens, posted Aug. 22, explains the phase-in of the flood requirement:

Starting in January 2024, all structures with a replacement value of $600,000 must obtain flood insurance.

The value requirement of the structure drops until 2027, when all Citizens-covered structures, regardless of value, must maintain flood coverage.

The insurer said it will soon send more information to agents, including a list of their affected policies.

The recent bulletin can be seen here, and on the Citizens website.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Another insurance firm is expanding into Florida, the state in which it has had its headquarters for several years.

Orion180, founded in 2016, with corporate offices in Melbourne, Florida, has been approved by state regulators as a property and casualty carrier, the Florida Office of Insurance Regulation announced Tuesday.

“Today’s announcement marks the third and fourth property and casualty insurers approved to operate in Florida following legislative reforms designed to promote market stability,” Florida Insurance Commissioner Michael Yaworsky’s office said in a bulletin.

Last week, OIR said it had approved Mainsail Insurance Co., a sister firm to Hippo Insurance and Spinnaker Insurance companies, to operate in the state. That followed the approval of Tailrow Insurance Co., part of HCI Group.

Recoop Disaster Insurance, underwritten by Professional Solutions Insurance, also announced it will offer a parametric-type product in Florida and is seeking approval from regulators.

Orion180 will operate as two insurers in Florida: Orion180 Insurance Co. and Orion180 Select Insurance Co. Both are domiciled in Indiana and applied to operate in Florida under an expansion application, OIR said.

Gregg (Orion180)

The move allows companies to expand into several states, using a uniform certificate of authority application, the National Association of Insurance Commissioners explained. While each “uniform” state will perform its own review of the application, the applicant company does not need to file different applications in different formats.

CEO Ken Gregg said Wednesday that the Florida legislative reforms, which limited costly claims litigation and what many said were frivolous lawsuits and exaggerated roof claims, have indeed had an impact on Orion’s decision.

“I’ve always wanted to do business in Florida but we knew we had to wait for the environment to be right,” he said in an interview with Insurance Journal. “I think the reforms and what the state has done and what the department is doing have made it so the time is right.”

The carriers aren’t being shy about taking on risk in storm-plagued Florida, he said. The companies plan to write homeowners’ policies in “true coastal areas,” on the state’s east and west coasts, Gregg said. Those will include some high-end properties, with Coverage A limits above $700,000 — picking up where the state-created Citizens Property Insurance is limited by law.

Commercial policies may come later, he added.

Gregg, who was previously with CNA Insurance and Allianz, launched Orion180 as a tech-heavy company in 2018. In press releases and company information in the past year, the firm has noted that it transitioned from a managing general underwriter to a standalone carrier with the launch of Orion180 Insurance Co.

Late last year, the company said it was expanding into Georgia and South Carolina, after operating in North Carolina, Alabama, Mississippi and Tennessee. Orion180 has said it has more than 80,000 policies issued, with written premium of $150 million in 2022. It now works with about 8,000 agents.

A year ago, Orion was approved to build a six-story, $50 million office complex in Melbourne, with part of the site providing retail space and apartments, according to news reports. But the project never got off the ground after the developer was unable to obtain proper financing and make the numbers work, Gregg said. Orion180 now plans to find another office site by next summer, he noted.

The KBRA financial rating firm in June gave Orion180 Insurance Co. a BBB+ financial strength rating, with a stable outlook.

“The rating is positively impacted by the experienced management team, favorable projected capitalization levels, a business plan benefitting from an existing MGA book with good historical loss experience, minimal legacy issues, and reasonable start-up expenses,” the KBRA report noted. “These positive factors are offset by exposure to event risk and reinsurance dependence, product and geographic concentration, and some execution risk as a start-up insurer.”

Policyholder surplus for this year was just over $50 million, a big jump from the previous year. Orion180 Insurance also reported an $807,000 net loss in 2022, but its profit was expected to rise to more than $1.6 million by 2025, KBRA noted. On a consolidated basis, Orion has been profitable since 2019, a company official said.

“KBRA believes that Orion’s transition from using a fronting provider to an underwriter writing on its own paper, allows for a reasonable market opportunity to successfully execute their business plan,” the rating firm wrote. “However, management must remain disciplined, as they are not bound by the underwriting constraints of a fronting provider.”

Orion180 is not rated by AM Best but Orion180 Insurance and Orion180 Select both received an “A Excellent” financial stability rating from Demotech at the end of July.

The company plans to continue expanding, probably into some Midwestern states in coming months, Gregg said.

This article has been updated to include new information from Orion180.

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

Insureds Hot About Flood Insurance Costs? Some Areas Are Seeing 35% Discounts

Florida property owners stuck with higher premiums and new flood insurance mandates may want to nudge their local governments to take a look at the town of Cutler Bay and the counties of Monroe, Pinellas and Ocala.

Those jurisdictions are among just 17 across the country that have achieved a Class 3 rating from the Federal Emergency Management Agency, which results in 35% discounts on flood insurance premiums for homeowners.

In Cutler Bay, a storied community on Miami’s southern flank with about 45,000 residents, the average premium dropped by $338 this year. Citywide, that’s a savings of $2.3 million.

“This savings is a tangible result of the flood mitigation activities your community implements to protect lives and reduce property damage,” reads a letter from William Lesser, FEMA’s Community Rating System coordinator.

The rating system and the National Flood Insurance Program have their critics, including those who argue that the system doesn’t go far enough to discourage building in flood zones or to encourage individual property owners to take flood-proofing steps. But some local officials say the rating system and their discounts have become vitally important to homeowners at a time of soaring insurance premiums.

Casals (Cutler Bay)

It takes some some sense of urgency, some public expenditures and a little self-owning of a community’s infrastructure problems to achieve the improved rating. Cutler Bay’s experience gives some insight: Just a few years ago, Cutler Bay, hit hard by Hurricane Andrew in 1992, was near the bottom of the ratings, at Class 6.

“Cutler Bay really put their money where their mouth is and decided to leap forward on this,” said David Stroud with WSP USA, an environmental engineering consulting firm that worked with the city.

Facing rising seas, and the likelihood of more rainfall and stronger storms, city staff began working in 2011 to up its game.

“If we can do it with a city staff of just 32 people, anybody can,” said Rafael Casals, town manager.

Besides preserving 44% of the flood hazard area, as designated on flood maps, as open space, one of the most significant measures that Cutler Bay officials undertook required no commitment from builders, developers or homeowners: It was simply maintenance – on an aggressive schedule.

While the surrounding county jurisdiction vacuums out its stormwater drains on an 8-year schedule, Cutler Bay does it every two years: Half the town’s drain lines get cleaned one year and the other half gets it the next year, explained Yenier Vega, stormwater utility manager for the city.

The maintenance plan received a real test in June 2022, when the area received 26 inches of rain in less than three days. While streets flooded for several hours, the water was able to drain away faster, thanks to unclogged drains and sewer mains, officials said in a recent interview with Insurance Journal.

“It cleared up a lot faster because of all of our action,” Casals said. “It drew attention to how important it is to maintain your stormwater system.”

The cost of the enhanced flood measures has been surprisingly affordable for the city, officials said – less than $100,000 a year, from a town budget of $43 million. Much of the funding for infrastructure improvements have come from federal grants, which are easier to obtain with an improved town master plan.

“The biggest cost is the time it takes,” Vega said. “You have to sit there and go through it all. And when sit there and go through it, you’re going to find deficiencies in your program.”

And that’s part of the reason why more coastal cities, even in the face of dire climate-change warnings, have not taken similar steps, Casals and Vega said.

“A lot of cities don’t like that,” Casals said. “Why? Because you have to expose yourself and show what are your vulnerabilities.”

The measures can also meet with resistance from developers who want to build homes and commercial properties in vulnerable areas.

But in a low-lying area and with new flood insurance mandates, the improvements are worth the headache, town officials said. Parts of Cutler Bay are just 14 feet above current sea level. And the Florida Legislature last year required most properties covered by Citizens Property Insurance Corp. to also obtain flood insurance, regardless of locale.

An estimated 4,000 property owners in Cutler Bay are insured by Citizens, out of about 228,000 Citizens policies for all of Miami Dade.

“When we have to tell developers that they have to build another foot above the base flood elevation, what do you think the pushback is going to be?” Casals asked. “But our town council gets it and they would take that hit.”

The town’s drainage improvements have the added benefit of keeping polluted runoff out of adjacent Biscayne Bay, an already stressed body of water, Vega said.

Still, vacuuming drains, preserving greenspace and raising buildings by just a few feet may be only a short-term balm for a long-term problem that studies show is growing worse by the year. By 2030, much of Cutler Bay will face serious, regular flooding, according to computer modeling done by Climate Central, a nonprofit group of scientists.

Without extensive pumping and inland storage measures, coastal cities’ drainage systems may have nowhere to drain the floodwaters to, no matter how clean the drain lines are, explained Craig Poulton. Poulton is head of Poulton Associates, a private company that writes flood and catastrophe insurance. He has been a staunch critic of the NFIP and the Community Rating System.

Although he and Stroud, of WSP, have said that some models suggest that sea levels may not rise as severely as many studies have predicted, cities like Cutler Bay will still face consequences in coming decades.

The CRS itself is flawed because it undercuts FEMA’s newly established Risk Rating 2.0, which aims to base flood insurance rates more on the risk of individual properties, not area-wide and outdated flood maps, Poulton said.

“It goes back to the old paradigm of ‘everybody gets the same rate,’ only in this case, it’s ‘everybody gets the same discount,” he added.

A house at a lower elevation in a Class 3 community gets the same 35% discount as one that has taken the trouble of raising its foundation by eight feet, he noted. The more at-risk property now has less incentive to reduce flood risk, since the city has reduced its cost of flood insurance.

Poulton

And while Cutler Bay and Monroe, Pinellas and Ocala counties have taken steps to reach the higher ratings, most communities have not, Poulton pointed out. The majority of cities and counties – 1,485 in all – have settled for lower ratings and smaller discounts, probably because of the commitment and expense involved in upgrading infrastructure and building restrictions, he noted.

“Most communities are like water: They take the path of least resistance,” Poulton said. He added that the time and expense involved in improvements means that most cities aren’t stepping up, yet can still claim some discounts, thanks to the structure of the CRS.

Cutler Bay officials said that FEMA audits their master plan and other improvements, to ensure the city is meeting the Class 3 requirements. But for the lower ratings, FEMA has a history of not stringently enforcing the requirements, Poulton said. Many of the CRS requirements for discounts in the lower ratings do nothing to reduce flood risk for communities and homes, he noted. These include points for simply advertising the need for homeowners to purchase flood insurance.

“If anything, it adds to the burden of the taxpayer, because the property gets discounts on flood insurance from NFIP,” he said.

Still, Cutler Bay’s administrators believe in the rating system and now plan to undertake additional improvements to reach Class 2 – and a coveted 40% discount for most flood insurance policyholders. Only six communities nationwide, none of them in Florida, have achieved Class 2. Just two, Tulsa, Oklahoma, and Roseville, California, have made it to the top rung of Class 1.

“At least for us, we are charting our own course,” Casals said. “Our role is to protect our integrity and provide the best service we can to our residents.”

Please call Lee from USAsurance Powered by WeInsure. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer.

When Citizens Property Insurance Corp. in June filed for the maximum rate increases allowed by its statutory glidepath, many in the Florida insurance industry saw it as a good thing, needed to help steer policyholders back toward the beleagured primary market.

Today, at least some in the industry are scratching their heads after Florida Insurance Commissioner Michael Yaworsky struck down part of Citizens’ 12% average rate increase request on homeowners’ policies, ordering the state-created insurer to come back with a new proposal within 30 days.

The proposed, overall increase exceeded the glidepath, Yaworsky’s order explains. But one insurer executive said the order may have gone too far and some personal lines increases could have been approved.

“I was surprised, because given the data that’s come from Citizen’s leadership and their board, it seems clear that Citizens’ policies are underpriced and a rate increase is justified,” said Melissa Burt DeVriese, president of Security First Insurance Co., the 12th-largest property insurer in Florida.

With Citizens’ rates limited by law, premiums are significantly lower in many parts of the state, which has caused the residual insurer to become the largest carrier in the state with more than 1.3 million policies in force. Without the larger rate increase, primary market carriers will continue to find it difficult to compete with Citizens, DeVriese said.

Citizens now has until mid-September to come back with a smaller proposed rate increase on personal property, although Yaworsky’s office approved the requested increase for some commercial properties.

Yaworsky signed the orders late last week.

“The Office finds that due to the inadequate support as it relates to Citizens being non-competitive … rates should be subject to a modified policyholder capping methodology with the lower cap of 0% and an upper cap of +12%, until such time that Citizens can provide support in a subsequent rate filing,” the Aug. 18 order reads.

Dwelling fire and mobile home proposed rate increases also must be revised, Yaworsky’s order notes.

The Office of Insurance Regulation did not provide further comment Tuesday morning on the reasoning behind the denial order, but said more information may be released later. Kevin Comerer, a former lobbyist for a Florida insurer, noted that OIR had little choice.

“Everyone wants Citizens’ rates to be comparable, but OIR was simply interpreting the law and implementing rates based on the statutes,” Comerer said Tuesday. “They have to follow actuarial science and they have to follow the law.”

He argued that a more limited Citizens’ rate increase will have little impact on the market, compared to the effect from sweeping legislative reforms approved late last year, designed to stem the vast amount of claims litigation that has plagued insurers in recent years.

It’s not uncommon for regulators to ask insurers to reconsider or to provide more information, even on seemingly straightforward math questions.

“It’s part of the process,” said Citizens’ spokesman Michael Peltier. “There’s always room for interpretation.”

Revised filings don’t always follow the script. Last year, for example, the Florida OIR asked Florida Farm Bureau to revisit its request for a 41% rate increase. The insurer did that, and came back a few months later with an even larger rate request.

On the recent Citizens filing, it’s possible that regulators also heard an earful from irate policyholders, many of whom have seen private carriers leave the market and raise premiums significantly in recent months. The OIR held hearings on the Citizens proposal and received some 724 written comments from the public, Yaworsky’s final order notes.

For condominium associations in Citizens’ commercial lines account, Yaworsky did approve a 9.2% average statewide rate increase, effective Oct. 1. For other commercial residential property, the order OK’d a 9.5% rise. For non-residential commercial property, Citizens’ proposed 7.7% increase also was approved.

The homeowners’ rate order can be seen here. The commercial and condo order can be seen here.

The OIR orders come just a few weeks after the office and carriers announced that primary market insurers so far this year have requested more than 350,000 takeouts from Citizens. It was unclear Tuesday how or if a smaller-than-expected Citizens rate increase will affect the number of policyholders that agree to the takeout offers.