Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

Allstate said it is raising auto insurance rates more due to continued upticks in physical damage and bodily injury severity.

The personal property insurer said in a statement on April 21 that first quarter unfavorable non-catastrophe prior-year reserves re-estimates were about $160 million, reflecting the impact of “rapid increases in loss costs since the second quarter of 2021.”

“Given the ongoing loss-cost impacts of the current inflationary environment, Allstate has increased the magnitude of auto rate increases we expect to implement throughout 2022,” said Mario Rizzo, CFO in the statement.

Rizzo said Allstate increased auto rates in 15 states an average of 9.8% in March and has now implemented 53 rate increases in 41 locations averaging about 8.2% since the start of the fourth quarter. Additionally, Allstate’s National General brand increased auto rates an average of 3.8% in seven locations in March.

Last month Allstate addressed the topic of auto rate hikes. Glen Shapiro, president of property-liability, said auto-claim frequency remained below pre-pandemic levels even though miles driven increased, but claims from non-rush-hour accidents have returned to historical norms. Repair costs have increased due to supply-chain delays and higher labor costs.

In the latest statement, Rizzo said Allstate continued to see “the impact of elevated severity inflation in the current report year” with incurred severity estimates to increase by 11% for property damage and 8% for bodily injury.

All Allstate brand auto insurance rate increases totaled $862 million in the first quarter 2022 after $702 million of rate increases in the fourth quarter 2021, Allstate said.

Allstate also said first-quarter catastrophe losses totaled $462 million pre tax. Catastrophe losses, which primarily included tornado and wind losses from Texas and the southeast, were $227 million March.,

Chad is National News Editor at Insurance Journal. He has been covering the insurance industry since 2007, reporting on trends and coverage in most lines of insurance as well as natural catastrophes, modeling, regulation, legislation, and litigation. Chad can be reached at chemenway@wellsmedia.com

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

Digital Insurance spoke with Kevin Mitchell, president of TypTap Insurance Company about market conditions in Florida, technology and the company’s plans for the future.

The following responses have been lightly edited for clarity.

Can you tell me about your work TypTap?

Kevin Mitchell

I joined HCI Group Inc, in 2013 in the role of vice president of investor relations and reinsurance. When we launched TypTap in March 2016, I became more involved in the operations and marketing of the company. I continued to take on more roles and responsibilities. In 2019, I became the president of TypTap.

How is the company using technology?

Oftentimes, insurance companies will ask policyholders to fill out pages and pages of underwriting questions to receive a quote. These questions vary from the age of a roof to the year a home was built. Some homeowners may or may not know the answers.

At TypTap we were confident that our technology could simplify the customer experience by only asking a handful of questions for a quote. The technology gathers underwriting information and analyzes each home to determine coverage decisions. The tech allows us to solve a challenge that most insurance companies face—predicting the future cost of goods sold. The technology also allows us to remove geographic limitations and select profitable policies.

We believe that the technology must drive a better underwriting result and that has been our focus since the launch of the company.

In the insurtech space, most companies are focused on distribution but being able to improve underwriting results, we believe, is the key to long-term success.

AIG says BlackRock will manage up to $150B of its assetsThe insurer has been sharpening its focus on its core operations and making necessary preparations to split off its life and retirement unit, which is planned for the first half of this year.

Florida has always been a challenging state to do business from a homeowners insurance standpoint. You have hurricane risk, severe convective storms like thunderstorms and hail and there are sinkholes too–a whole host of challenges that make doing business as a homeowners insurance company challenging.

Weather risk also creates opportunities. TypTap’s first product in the state was flood insurance for single-family homes. We had policyholders contacting us asking for help with flood insurance. We started offering flood insurance in Florida in March of 2016.

From a technology standpoint, you only need a few key variables to underwrite flood insurance, for example, the exact latitude and longitude of the home, first-floor elevation and estimated replacement value of the home. We liked the flood insurance business but it has a limited market of only $5 billion, across the U.S., and we wanted to further accelerate growth.

The next logical step was building a homeowners insurance offering. And in 2018, we launched the first product and wrote about 1,000 policies that first year.

Why has the company paused new business in Florida?

In late February, TypTap decided to pause new homeowners’ business in Florida. An approach we have applied since 2018 to manage our capital for the benefit of existing policyholders. This approach allows us to be a stable market for Florida homeowners.

The approach is a part of our long-term business philosophy. We often place a pause on new business in Florida each spring because we experience rapid policy growth in the first and fourth quarters of each fiscal year. A new business pause gives TypTap the time to evaluate the book of business to make sure it is performing to expectations.

TypTap announced a national expansion in August 2020. We currently operate in 12 states and more are set to launch this year.

We started in Florida because our headquarters are here. We learned a lot of important lessons by launching in Florida. We’re applying those lessons learned in other states. The success in Florida gives us the confidence the technology is working and we’re onto something special.

We will resume writing policies in Florida upon establishing reinsurance prices and with a clearer understanding of the upcoming hurricane season. We’re keeping our commitment to providing quality service and simplified insurance.

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

Amid growing concerns about the health of Florida’s property insurers, the state’s largest carrier posted a somewhat mixed bag of financial results for the first quarter of 2022. But the company said it has taken big steps to reduce exposure and expenses.

Universal Insurance Holdings, the parent company of Universal Property & Casualty Insurance Co., said in its latest financial information that its combined ratio had dropped sharply compared to the end of 2021, to 97.9%. But the ratio was up slightly compared to this time last year, the publicly traded company reported.

Net income for Q1 2022 was $17 million, down from $26 million in the first quarter last year, but much stronger than the $48 million loss reported at the end of last year. Total revenue increased from the first quarter of 2021, but was down a bit from the final quarter of 2021.

“We reported a 16.9% annualized ROE despite the challenging external environment, which is a testament to the strength and resilience of our business,” CEO Stephen Donaghy said in a statement posted Thursday.

Net investment income for the first quarter was $4 million, up slightly from the end of 2021 and significantly higher than in the first quarter last year.

Direct premiums written fell slightly from Q4 2021 but were up 8.5% from this time last year, the financial report shows. That significantly outpaced a 6.1% decline in policies in force “as meaningful rate increases benefited premium volumes,” the CEO said.

Donaghy said that in addition to raising rates, the company has shed policies in “less profitable geographies,” tightened underwriting criteria and renegotiated agencies’ commission rates. The number of policies in force has fallen significantly, from 976,250 in March 2021 to 916,745 at the end of March 2022.

Universal is still slightly ahead of the state-backed Citizens Property Insurance Corp. in the number of policies it holds – but probably not for long. At the end of March this year, Citizens reported some 817,926 policies in force, but officials have said that number is expected to top 1 million by year’s end.

“Given our strong capital position, the profitability of our business and the steps we continue to take to improve results, we believe we stand out favorably as reinsurers increasingly differentiate amongst cedants in the current market,” Donaghy said.

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

You may need extra coverage for certain items or events.

Key points

Your homeowners insurance may not cover certain natural disasters.

Expensive items in your home may also fall outside your policy’s scope of coverage.

As a homeowner, there are different expenses you’re apt to incur outside of your mortgage payment. These include property taxes, maintenance, and the cost of homeowners insurance.

But even if you’re paying a decent premium for a homeowners insurance policy, you may still be left footing the bill for property damage if the circumstances align that way. Here are six things your homeowners policy may not cover.

1. Flood damage

If a pipe bursts inside your home due to flawed installation, your homeowners insurance policy may cover the associated damage. But if your home floods due to a hurricane or storm, your homeowners insurance likely will not pick up the tab for the bill. Floods of that nature are generally only covered by a separate flood insurance policy. If you live in a flood zone, it’s important to secure that additional coverage.

2. Wear and tear

Over time, appliances and other home features can deteriorate to the point where they need to be replaced. That’s not something you should expect your homeowners insurance policy to cover. If, for example, your washing machine dies after 10 years, it’ll generally be on you to cover the cost of getting a new one.

3. Termite damage

Termites can cause a lot of damage to a home, and sometimes it’s hard to pinpoint that they’re a problem until it’s too late. Unfortunately, many homeowners insurance policies do not cover damage caused by termites, so it’s important to stay vigilant and look for signs that your home is being invaded, like rotting wood.

4. Earthquakes

Most homeowners insurance policies won’t cover damage caused by an earthquake. The good news is that if you live somewhere prone to earthquakes, like California, you can buy separate insurance so you’re covered for those events. But if you don’t have a specific earthquake policy, don’t expect your homeowners insurance to kick in.

Find the Right Coverage for Your Home

Fill in the filters below to customize your results

ZIP CODE

AGE 16-20 21-24 25-34 35-44 45-54 55-64 65 +

HOMEOWNERYesNo

MARRIEDYesNoUpdate

Click on 2 or more home insurers below to compare personalized quotes

Home Insurance from $35/mo – YA

Details

Get Quote

Home insurance protects your home & belongings

Details

Get Quote

Home Insurance Quotes in 94404

Details

Get Quote

Low Cost Home Insurance – Save up to 40%

Details

Get Quote

California Home Insurance – Find the Best Deals

Details

Get Quote

Home insurance, great rates in Foster City, California

Details

Get Quote

Compare 50+ insurers. Real quotes in 90 sec. Buy online at Nsure.com

Details

Get Quote

Advertiser disclosure

powered by:

5. Expensive artwork or jewelry

Most insurance policies have a limit as to how much they’ll pay to replace specific items that are damaged or destroyed during a covered event, like a fire. If you have expensive jewelry or artwork, you may need to get a rider on your insurance policy to ensure you’ll be reimbursed for their full value if they are damaged or stolen.

Your insurance policy may, for example, reimburse you up to $1,500 for a painting destroyed in a fire. But if that painting is worth $10,000, you’ll still be out a lot of money.

6. Spoiled food from a power outage

Power outages can happen during storms, or when power company equipment fails. Unfortunately, many homeowners insurance policies won’t reimburse you for spoiled food during a power outage. But even if your policy does, remember you’ll have to meet your policy’s deductible before getting a check. If that deductible is $500 and you’re claiming $400 in spoiled food, you won’t wind up with any money.

Know your coverage

It’s important to read the fine print when buying homeowners insurance so you know what level of coverage to expect. You may end up needing additional insurance outside of your standard homeowners policy, but that may be worth investing in, depending on your personal circumstances.

Choosing the right homeowners insurance to protect you

No matter where you live, insuring your home is critical to protecting your finances in the event of an unexpected incident. Whether it’s a natural disaster, an accident, a break-in or something that causes damage to your property, you want to know you have the right homeowners insurance coverage for your situation.

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

May 23 through May 27.

Those are the dates Florida Gov. Ron DeSantis has set aside for a special session of the Florida Legislature to address a number of changes that could ameliorate what many have called a property insurance crisis in the state.

In a proclamation issued Tuesday afternoon, the governor listed seven reasons for convening lawmakers, including insurance industry losses, excessive claims litigation, rising homeowner premiums, insurer insolvencies and the rapdily expanding girth of the state-run Citizens Property Insurance Corp.

“Whereas, the Florida insurance industry has seen two straight years of net underwriting losses exceeding $1 billion each year; and … whereas, it is necessary for the State of Florida to act to stabilize the insurance market for Florida policyholders before the 2022 Atlantic Hurricane Season, which begins on June 1st,” it is prudent to call a special session, the proclamation reads.

DeSantis

Insurance industry insiders praised the move, but a few wondered how far some House of Representative members may go on reform measures. A statement by House Speaker Chris Sprowls, who has downplayed the need for further reforms, did not sound overly enthusiastic.

“We look forward to working with our partners to evaluate whether there is more we can do to address the availability and affordability of property insurance,” Sprowls said Tuesday, according to news reports. “The Florida House will remain primarily focused on addressing the needs of the policyholders of Florida.”

Others noted that DeSantis, fresh off a total victory in last week’s special session on redistricting and retaliation against the Disney Corp., appears to have the power to steer lawmakers toward significant changes.

“I think it will really come down to what the governor wants to do,” said Melissa Burt DeVries, president of Security First Insurance, one of Florida’s largest property-casualty insurers. “If he wants to address some of the major cost drivers, such as litigation, I think the governor could get it done and it would be a huge help to the industry.”

Florida’s chief financial officer, whose office oversees insurance and agent regulation, applauded the proclamation.

“The timing of this special session is especially prudent as it would convene before the start of the 2022 hurricane season in June, which is already predicted to be an extremely active storm season,” Jimmy Patronis said in a statement. “The sooner we tackle needed property insurance reforms, the sooner Florida consumers can reap the benefits of these policy changes.”

Sprowls

The special session apparently will not include condominium reforms or condo insurance issues, despite an editorial in the Miami Herald this week. Insurance premiums on high-rise condominiums have spiked since the Champlain Towers South building collapsed near Miami Beach in June 2021 that killed 98 people. A number of insurers have declined to write condo insurance while others are demanding more extensive inspection records, the Herald noted.

Along with significant property insurance changes, Florida lawmakers also failed to adopt tougher condo inspection and cash-reserve laws during the regular session this year that ended in March.

The governor’s proclamation also raised some eyebrows for three items on the session’s agenda. In addition to property insurance and reinsurance, the session will also consider legislation related to the Florida Office of Insurance Regulation and “appropriations.”

Speculation among some industry analysts Tuesday was that DeSantis may want to see funding for more positions at the agency, perhaps to give it the ability to move more quickly on regulatory changes and rate reviews.

The agenda also will include changes to the Florida Building Code, the governor indicated. That also caught some off guard, since the state Building Commission already is scheduled to consider changes to the code, including revisions to the section that, in many cases, requires full roof replacement if just 25% of a roof section is damaged.

The announcement also updated some often-quoted figures that seem to sum up the state of the insurance market in Florida. The OIR last year said that data from the National Association of Insurance Commissioners shows that while Florida accounted for about 8% of all homeowner insurance claims in the United States in 2019, Florida homeowner insurance lawsuits made up 76% of all litigation against insurers, nationwide.

DeSantis’ proclamation said those numbers have now grown to 9% and 79%. That could indicate that 2019 and 2021 legislative reforms designed to reduce claims litigation have had little effect.

The session is scheduled to begin at 9 a.m. on May 23, a Monday, and extend no later than midnight on Friday.

Top photo: The Tallahassee skyline, courtesy VisitTallahassee.com.

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

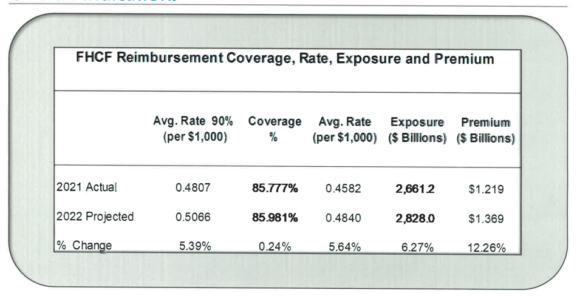

Premiums paid to the Florida Hurricane Catastrophe Fund are expected to increase by more than 12% later this year, giving new urgency to calls to cut the fund’s retention level in half, a move that some estimates show could save Florida insurers and policyholders as much as $1 billion a year.

And the methodology used to calculate the need for the higher cat fund premiums has come under the disapproving eye of some Florida insurance company executives. They suggest that too much emphasis has been placed on one hurricane-loss computer model that predicts larger storm losses than most other models do.

“The FHCF could have chosen to ignore that model,” or could have averaged the results of all seven approved models, reads an email from one company official. “Since that wasn’t done, the reinsurance costs paid to the FHCF by Florida’s consumers increased by $150 million.”

A recent ratemaking formula report from Paragon Strategic Solutions, an Aon company, shows that for contract year 2022, total premiums from Florida property and casualty insurers would rise from $1.21 billion to $1.37 billion. That’s particularly onerous for some insurers, given the fact that private-market reinsurance premiums also are expected to soar, starting June 1, along with the continued cost of claims litigation, hurricane losses, roof claims and higher assessments to pay insolvent insurers’ claims.

The results of the individual computer models aren’t publicly available. But the Paragon report said that one loss model was based on a strict interpretation of the Florida Building Code’s requirement that, if just 25% of a roof section is damaged in a storm event, then the entire roof should be replaced.

“This change affects overall premiums and rates,” the report noted.

That building code is now under review. The Florida Roofing and Sheetmetal Contractors Association has proposed relaxing the replacement requirement, which could help discourage “free roof” campaigns by some unscrupulous contractors, officials have said.

The Paragon report also ignored two more recent hurricane loss-cost models that have been approved by the Florida Commission on Hurricane Loss Projection Methodology, insurers pointed out. Paragon’s managing director and actuary, Andrew Rapoport, could not be reached for comment Monday.

The cat fund’s proposed 2022 rates will be presented to the fund’s governing body, the State Board of Administration, at its June 28 meeting. The fund’s chief operating officer, Gina Wilson, has declined to comment to the Insurance Journal about the fund.

The increase in premiums is sure to add fuel to the growing fervor for the Florida Legislature to lower the cat fund’s retention level. Gov. Ron DeSantis has said he plans to call lawmakers into special session some time in May to tackle a range of proposed solutions to Florida’s property insurance crisis.

One of those proposals has been discussed in the industry for years.

It’s known as the retention, or the threshold of industry losses from a catastrophic event that must be reached before insurers can tap into the cat fund. It’s a type of reinsurance that comes at a much lower cost than reinsurance in the private spot market, insurers have said.

By lowering that retention amount, from $8.5 billion to $4 billion, would still give the $11 billion cat fund enough reserves, but it would shave about 10% off the amount of reinsurance that must be purchased by insurance companies, supporters of the change have insisted. That could save Florida insurers an estimated $1 billion annually, according to insurer estimates and Sen. Jeff Brandes, who has advocated for the change.

Cat fund officials have argued against sudden changes to the fund’s retention level. Information from the fund, provided to Brandes, argues that “the FHCF is 45% more likely to exhaust its $11.3B projected 2021 year-end fund balance and begin subsequent season with a projected fund balance equal to just one year of premium.”

But industry advocates have said the 45% figure is overly dramatic. The fund’s report shows that the odds that cat fund’s balance would be exhausted would increase from a 3% chance to a 4.3% chance. That’s about a 45% increase, but the likelihood is still quite small, some industry analysts have said.

State law in 2004 required an elastic retention level of at least $4.5 billion. Due to an 89% increase in exposure since then, the retention requirement has grown to $8.5 billion for 2022, the Paragon report said. Critics have argued that the automatic increases are out of line with reality.

“Due to a misguided concern that the FHCF’s funding continue to increase indefinitely, its ‘retention’ (threshold at which it begins protecting consumers) has been allowed to ‘inflate to irrelevance,’ even as the premium it charges Florida consumers (via their property insurers) retains a 25% surcharge originally intended as an emergency measure to build cash after 2004- 05’s eight hurricanes,” the Federal Association For Insurance Reform argued in a 2021 white paper to regulators.

Brandes

FAIR noted that the retention had been as low as $2.9 billion before the calamitous 2004-2005 hurricane season. The “rapid cash buildup” surcharge was set in 2006, repealed the next year, then reinstated in 2009. Temporarily halting it now would save consumers and insurers significantly, FAIR has said.

But cat fund officials have warned that major hurricanes, such as those that are predicted in coming years with warming seas and rising tides, could bring the fund to its knees.

In February, Brandes sent questions to the fund’s Wilson, asking her and her staff to contemplate effects of various types of storms on the fund. Answers from the fund suggested that an event like the famous 1926 hurricane that struck Miami would result in a $16 billion loss under the current retention. For a storm similar to 1992’s powerful Hurricane Andrew, the fund’s layer loss would top $9 billion.

She said estimates on the effects of those storms, using a lowered retention level, were not available.

It’s uncertain if Brandes will sponsor a separate bill on the cat fund during the upcoming session, or if it will be made part of an omnibus rescue bill. In January, during the regular 2022 legislative session, the senator offered a retention amendment to a separate bill, but withdrew it after concerns from other lawmakers and fund officials that it was too much to chew with no advance notice.

Insurance rates are skyrocketing and majority of homeowners are feeling the impact

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

Contractor Fraud: A Threat to Market StabilityInsurance rates are skyrocketing and majority of homeowners are feeling the impact. Higher insurance rates can be life altering, requiring homeowners to make decisions between vital medications, food, gas and other essentials. Fraud, specifically schemes perpetuated by contractors and other third parties, is a threat to the stability of the insurance market, a market that is already on life support (as I explained to Legislators last year). Just last month, Chief Financial Officer Jimmy Patronis announced two arrests of contractors in Naples for allegedly operating a solicitation scheme for free roof replacements due to Hurricane Irma damage. They allegedly enticed homeowners with rebates to cover their insurance deductible if they submitted an insurance claim for a roof replacement.The company’s salespeople would require the homeowner to sign an Assignment of Benefits and an “advertising agreement,” which allowed the company to place an advertising sign in their yard, and the homeowners were required to provide positive reviews online and give neighborhood referrals.•If convicted on all charges, they each face a maximum sentence of up to 45 years in prison and a $45,000 fine. The company’s salespeople would require the homeowner to sign an Assignment of Benefits and an “advertising agreement,” which allowed the company to place an advertising sign in their yard, and the homeowners were required to provide positive reviews online and give neighborhood referrals. • The contractors face nine counts of filing False & Fraudulent Insurance Claims, a third-degree felony. • If convicted on all charges, they each face a maximum sentence of up to 45 years in prison and a $45,000 fine. These schemes are real and are happening more frequently. You have the power to help stop contractor fraud by being informed and reporting fraud. Know how the schemes work and how to avoid falling victim. MyDemolish Contractor Fraud: Steps to Avoid Falling Victiminitiative provides a thorough overview on how contractor fraud works, including both common and uncommon tactics used by contractors. The program also includes a collection of stories from consumers sharing their experience with contractor fraud and how they were impacted. The program also outlines the prohibitions placed on contractors as outlined in law.The more informed you are about contractor fraud, the less likely you are to become a victim.As Florida’s Insurance Consumer Advocate, I am deeply concerned about the insurance market and how increased rates impact you and your family. I will continue working with CFO Patronis and his team and the Florida Legislature to address the factors causing rate increases, like fraud. As I work to influence impactful legislative changes, I urge you to learn more about contractor fraud @ www.MyFloridaCFO.com/Division/ICA/Demolish.Additionally, there may be ways to reduce your premium:• Ask your agent to review your coverage to ensure you are only paying for what you need. • Ask your insurance agent if you are eligible for premium discounts, as offered by most companies. • Determine if you can adjust your deductible, which may decrease your premium. But remember, if you sustain damage and file a claim, you will be responsible for the deductible amount. Together, we can combat fraud. Be informed and report insurance fraud: Department of Financial Services’ Fraud Reporting Portal.Learn More

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

The Florida Office of Insurance Regulation has given FedNat Insurance a week to come up with a plan to improve its financial footing, after the company’s stability rating was downgraded to level that is not recognized by the secondary mortgage market.

In a consent order signed Friday by Insurance Commissioner David Altmaier and executives with FedNat and its sister companies, the companies must file a strategic plan to acquire additional capital, improve FedNat’s rating and obtain sufficient reinsurance by its July 1 renewal date.

The Demotech rating firm on April 14 downgraded FedNat’s stability rating from “A exceptional” to “S substantial,” citing heavy losses after storms hit Texas and Louisiana in 2021. The rating indicates that the carrier continues to have substantial resources and is not in imminent danger of collapse, Demotech’s president said.

But an “S” rating is not recognized by Fannie Mae and Freddie Mac, the government-sponsored purchasers of home mortgages.

“If FedNat’s policies are no longer acceptable to the secondary mortgage market, at renewal, policyholders may be required by the lender to obtain replacement insurance coverage,” the OIR consent order explained.

The order noted that FedNat is a domestic property and casualty insurer in Florida, along with its sister company, Monarch National. Another company held by FedNat Holding Co., Maison Insurance Co., is a foreign insurer, domiciled in Louisiana. OIR said that while FedNat had its rating trimmed, Monarch’s rating of “A” had remained the same and Maison is not rated by Demotech.

Together, the three had 152,000 policies in force in Florida at the end of March, and about 96,000 policies, mostly for homeowners, in Alabama, Louisiana, South Carolina, Texas and Mississippi.

Altmaier

The consent order did not explain why Monarch and Maison were included in the directive. Publicly traded FedNat Holding Co., which reported a $103 million loss for 2021, has already announced several measures to improve its bottom line, including pulling out of Louisiana and Texas and running off its Maison operations.

Shoring up its capital investments also is in the works.

“The companies and FedNat Holding Co. have represented that they are in active negotiations with multiple parties regarding potential agreements for additional capital and the implementation of a strategic reorganization plan designed to provide for long-term stability,” the consent order reads.

The companies have until Friday, April 29 at 5 p.m. Eastern time to submit the plan. It must include projections for the next 30 months, a cash-flow analysis and a catastrophe reinsurance program. FedNat has waived its right to have a hearing on the matter, OIR said.

The order was signed by Michael Braun, president of FedNat and Monarch, and by Maison’s treasurer, Erick Fernandez. They could not be reached for comment Monday morning. FedNat is headquartered in Sunrise, near Fort Lauderdale.

FedNat Holding’s stock price has fallen steadily in the last month, from $1.39 a share on March 24, to just 53 cents on Monday, April 25, according to Yahoo Finance and other market tracking sites.

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

I had planned to write and try and answer the question, how can Demotech give a brand-new company (Florida newcomer, Vyrd Insurance) an A rating before they even write a single policy. As I looked into the rating process (which I don’t fully understand yet, but I plan to), I decided that Demotech used the best and most relevant information available at the time. I’ve looked into their results and from what I can tell, their rating system seems to achieve their stated goals so they get a pass from me for now.

As I dug into it, I began to see a question behind the question (thanks, John G. Miller, author of QBQ) I decided that Demotech did yeoman’s work in their rating. My trouble is not with the rating and it’s not with Vyrd. I dug a little into them and from what I’ve read so far in their OIR (Office of Insurance Regulation) filings, there’s nothing that jumps out as a system issue, except for one tiny detail.

The problem comes from a unique wrinkle in how property (homeowners’) insurance in Florida operates. In Florida, we don’t have a homeowners’ JUA or FAIR plan anymore. We have Citizens Property Insurance Corporation, our residual market for homeowners’, commercial property, and wind coverage.

Before going any further, I should probably tell you that I used to work for Citizens and loved my job there. I worked with some great insurance professionals and learning professionals. I’m not taking issue with Citizens here. I’m taking issue with a problem that the state created and saddled Citizens (and the rest of us) with.

In looking at the news and at their filings, the problem comes because their business model to gain an influx of premium is to be a Citizens take-out company, which is not nearly as good as getting take-out from that little sandwich place down the road. Because Citizens is supposed to be the market of last resort in the state, standard market companies (like Vyrd) can apply to take policies out from Citizens.

The short version of the story is that Citizens does not only write policies on those risks that would qualify for a JUA or a FAIR plan but every building in the state could potentially be insured by Citizens. When I first went to work at Citizens, they were the largest property insurer in Florida, which was never the intent, but that’s another story for another day. Those who could otherwise qualify for coverage in the standard market are eligible for the takeout program. This allows carriers to select risks based on specific criteria that they create. That’s how companies end up with thousands of new policies on their books quickly without any expense for picking up new policies.

Here’s the problem with the business model. It doesn’t work nearly as well as most carriers think it will. They plan on picking up hundreds or thousands of policies, receiving an infusion of premium dollars immediately, and instantly gaining a renewal book of business worth plenty. Remember that Florida homeowners’ insurance premiums are among the highest in the nation. If everything went the way the carriers planned, they would have a solid book of business without having to pay any customer acquisition costs or claims.

It never works out exactly that way.

What usually happens is that the carrier submits the list of risks that they want to take and so do a dozen other carriers. There are always several carriers that end up wanting the same risks so that means that someone loses out and in fact, most carriers don’t get what they want. This is just the first cut on their list.

Then the policyholders are notified that they have been selected for takeout. They get a letter that tells them that on a specific date, their policy will no longer be with Citizens, but with a new company. Several policyholders will ignore the letter for now. Others will take the letter and call their agent, which the letter tells them to do. When they call, it’s not to say thanks for finding this new policy. It’s who is this insurance company? Who said that I wanted them to write my insurance? Will they be there in a year? Will they raise premiums or reduce coverage? What often happens next is that the policyholder sends back their response to Citizens. No thanks. I’d rather not change insurance companies.

The list is smaller now.

Eventually, those customers that ignored the letters receive a bill or renewal notice or something else that alerts them to the fact that they have a new insurance company. That’s when they call their agent to ask those questions. What insurance company is this? Why did my company change? No, I didn’t see the letters letting me know about this change. Is there anything that I can do now? No, I don’t think I want that insurance company. I can’t even pronounce it.

The list is smaller now.

On renewal, some policies will renew. Others won’t. Costs will be incurred. Claims will come in. The truth of the Florida insurance market will arrive somewhere between their top line and bottom line. The claims reserves will increase. Maybe there’s a storm. Maybe there isn’t. Maybe there are four storms. It’s never as easy as it looks on paper. Maybe they can apply for another Citizens takeout.

The flaws with this business model are really in the numbers. Companies may think that they’re going to get the number of policies that they need, but the truth of it is that it never works out the way they think it will on paper. It’s the same lesson that I learned in my early Army days.

No plan survives first contact with the opposing force.

Please call Lee from USAsurance Powered by WeInsure & Calle Financial. 954-270-7966 or 833-USAssure at the office. My email is lee@myUSAssurance.com . I am Your Insurance Consultant about Home Insurance, Auto, Flood, Private Flood, Car, Life Insurance, Mortgage protection, Financial Products, Business & Commercial Policies, & Group Products for business owners to give Employees benefits at no cost to the employer. My email is lee@myUSAssurance.com

Insurer insolvencies are hard enough on policyholders and company executives, but local agents across Florida also are feeling the pain from one recent liquidation and may soon feel it from others.

The Florida Department of Financial Services has notified agents that invoices for unearned commissions for Gulfstream Property and Casualty Insurance Co., which was liquidated last summer, will be sent out starting this week.

The total commissions that must be returned amount to about $4.1 million, and must come from 985 agencies, said Kyle Ulrich, president of the Florida Association of Insurance Agents.

That’s an average of $4,162 per agency. But some Florida agencies wrote hundreds of Gulfstream policies that were canceled before they expired, and may face significant bills.

“I think we’re probably getting a bill for about $20,000,” said David Radcliffe, a branch manager and producer at Underwood Anderson Insurance agency in Gulf Breeze, Florida. “We have the money, but all of a sudden we have to write a check for that.”

Many agents in Florida in 2022 will also be asked to return unearned commissions from Avatar Property and Casualty Insurance, which was deemed insolvent earlier this year. Lighthouse Property Insurance Co. was placed into receivership last week by Louisiana regulators, and agents in Florida may be asked later this year to return their commissions on those policies.

And more insolvencies are expected before the year is out as many insurers continue to face losses from hurricane claims, roof replacements and litigation costs.

Bradford

“It’s not a fun time to be in the insurance business as an agent right now,” said Amber Bradford, owner of the We Insure agency in Navarre, Florida.

Bradford said she had written about 50 homeowner policies with Gulfstream, but has not yet seen the bill from the Department of Financial Services.

“I imagine some agencies will be hurt a lot more than we are,” she said.

One panhandle insurance agency reportedly had written 1,600 policies with Gulfstream in recent years, agents said. Other high-volume producers around the state could face even greater expenses. Gulfstream had more than 35,000 policies in force when it was liquidated in July 2021, state officials have said.

DFS indicated that all invoices for unearned commissions should be sent to agents by the end of May. The department, which is acting as the receiver for Gulfstream, will work with agents who need assistance in making payments, the FAIA’s Dave Newell said Tuesday in a bulletin to agents.

“Do not hesitate to reach out to the receiver to work out a repayment plan,” the bulletin noted. “Please post any questions you may have about this process, so we can get clarification from the receiver.”

Gulfstream also operated in Texas, Alabama, Mississippi and South Carolina, so agents in those states also are affected. A notice from the South Carolina Property and Casualty Insurance Guaranty Association said that agents in that state will receive notices from Florida regulators about unearned commissions.

Contractor Fraud: A Threat to Market StabilityInsurance rates are skyrocketing and majority of homeowners are feeling the impact. Higher insurance rates can be life altering, requiring homeowners to make decisions between vital medications, food, gas and other essentials. Fraud, specifically schemes perpetuated by contractors and other third parties, is a threat to the stability of the insurance market, a market that is already on life support (as I explained to Legislators last year).

Contractor Fraud: A Threat to Market StabilityInsurance rates are skyrocketing and majority of homeowners are feeling the impact. Higher insurance rates can be life altering, requiring homeowners to make decisions between vital medications, food, gas and other essentials. Fraud, specifically schemes perpetuated by contractors and other third parties, is a threat to the stability of the insurance market, a market that is already on life support (as I explained to Legislators last year).